What Readers Need to Know

- Pension consolidation means combining several pension pots into a single scheme.

- It can simplify management and reduce charges but can also lose valuable features.

- Defined benefit transfers normally require regulated advice and are usually cautious.

- SIPPs, modern personal pensions and master trusts are common destinations.

- The Pension Tracing Service helps locate forgotten pots.

Introduction

Many UK savers accumulate several pension pots over their working life — a workplace pension at each employer, perhaps an old personal pension, sometimes a SIPP. Consolidation is the conversation that often follows: would it be simpler, cheaper or better to bring them together?

This article explains, in plain British English, what pension consolidation is, when it makes sense and when it does not. It covers the 2026/27 tax year and is general information for UK readers — not personal advice. A regulated financial adviser can help match a consolidation decision to circumstances.

Pension Consolidation in One Sentence

Pension consolidation means transferring the value of one or more existing UK pension pots into a single scheme, usually to simplify administration, reduce charges or improve Investment choice.

Why Savers Consolidate

- Simpler administration — one set of statements, one provider, one portal.

- Lower charges — modern low-cost SIPPs can be cheaper than older personal pensions.

- Wider investment choice — particularly compared with legacy schemes.

- Easier Retirement Planning — bringing pots together helps model income strategies.

- Up-to-date features — modern drawdown and beneficiary nomination tools.

Why Savers Might Not Consolidate

- Loss of guaranteed Annuity rates (GARs) — sometimes valuable on older personal pensions.

- Loss of with-profits bonuses or terminal bonuses in legacy plans.

- Loss of defined benefit guarantees — guaranteed income for life cannot easily be replaced.

- Loss of life cover or Waiver of premium features attached to older policies.

- Loss of tax protections (fixed or individual protection) where transfers would invalidate them.

- Loss of employer contributions on an active workplace pension.

- Exit fees on older policies wiping out consolidation savings.

What Counts as Old Pension Pots

Old pension pots typically include personal pensions opened decades ago, workplace pensions from previous employers, group personal pensions arranged through old employer schemes and any frozen DB benefits from earlier careers. Each pot may have different rules, charging structures, default investments and exit terms. A consolidation review starts by gathering all current paperwork, statements and projections.

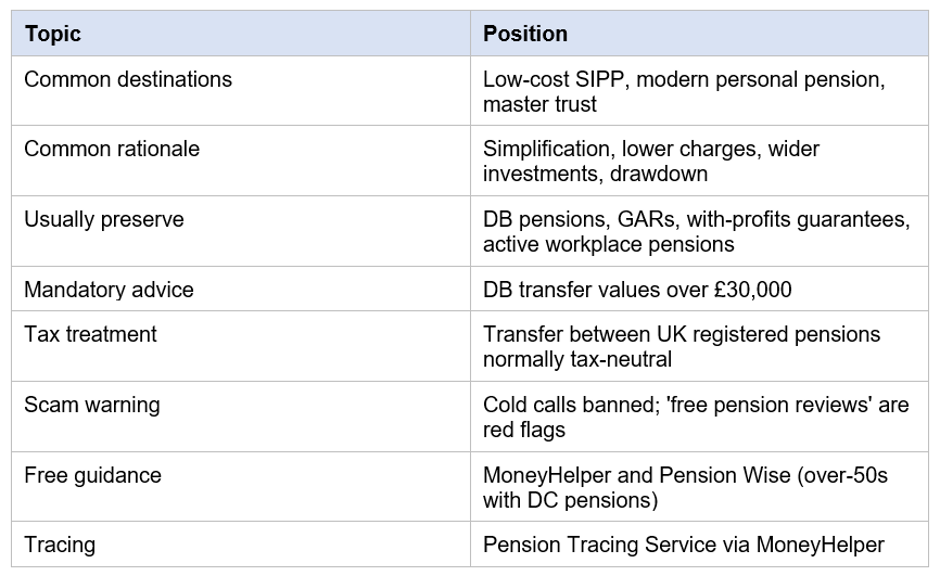

Common Destinations

Each destination has its own strengths. Many savers consolidate into a SIPP for breadth of investment choice; others use a master trust or modern personal pension for simplicity.

- Low-cost SIPPs — wide investment choice and modern drawdown support.

- Modern personal pensions — simpler default fund Options with online administration.

- Master trusts — large multi-employer occupational DC schemes governed by independent trustees.

- A new SIPP or personal pension opened specifically for consolidation.

Defined Benefit Transfers

Transferring a defined benefit pension to a DC scheme exchanges guaranteed income for life for a one-off cash equivalent transfer value. The transfer value can be large but the loss is permanent. UK rules require regulated advice for DB transfer values above £30,000. The FCA's default position is that DB transfers are not in the member's best interests unless the case for transfer is clear. Many DB transfer cases have been the subject of FCA enforcement and FOS complaints.

Consolidation Trade-Offs in Detail

Consolidation is rarely a clear win. The decision usually depends on weighing simplification and lower charges against the features and protections given up. Several practical trade-offs come up repeatedly.

- Charges — consolidating into a cheaper modern provider can reduce ongoing costs, but exit fees on the original scheme can offset savings.

- Investment choice — wider menus support tailored portfolios but require more decisions.

- Service quality — modern platforms offer online dashboards, app access and faster paper-free administration.

- Drawdown access — older policies sometimes do not support modern flexi-access drawdown.

- Estate planning — bringing pots into one provider simplifies beneficiary nominations.

- Lost features — GARs, with-profits bonuses, life cover and tax protections can be lost.

- Time out of the market — funds during transfer are typically held as cash.

Partial Consolidation

Consolidation does not have to be all-or-nothing. Many UK savers consolidate two or three older DC pots into a single SIPP while keeping the active workplace pension running and leaving any DB pensions in place. This 'partial' approach balances simplification with preservation of valuable features. Reviews every few years can reassess whether further consolidation is appropriate.

Lost Pensions

Many UK workers have pensions they have lost track of — perhaps from a brief Job decades ago. The Pension Tracing Service, provided through MoneyHelper, can help locate them. A planned consolidation often begins with a tracing exercise, gathering information about each pot before deciding what to do.

Process for a Sensible Consolidation

- List all pensions with values, scheme names, charges, features and guarantees.

- Request statutory transfer values and scheme features in writing.

- Compare receiving schemes on charges, investment choice and drawdown options.

- Engage a regulated financial adviser for transfer recommendations.

- Consider Pension Wise (MoneyHelper) for free guidance if aged 50 or over with DC pensions.

- Check the FCA Register before signing anything with any adviser or firm.

- Watch for scams — cold calls promising 'free pension reviews' or 'guaranteed returns' are red flags.

Tax Treatment of Consolidation

Transfers between UK registered pension schemes are normally tax-neutral. The receiving scheme takes on the pot at its existing value, subject to verifying any protections in place. There is no tax relief on the transfer itself; relief was given on the original contributions. The annual allowance is not used by transfers.

Costs of Consolidation

Direct costs may include exit fees from the original scheme (FCA rules limit or ban these in many cases), transfer paperwork costs, adviser fees for transfer reports and any in-specie transfer fees on the receiving SIPP. Indirect costs include time out of the market during transfer and any difference in fund pricing between providers.

Scam Warning

Pension scams have repeatedly targeted UK savers around consolidation. Common patterns include cold calls offering 'free pension reviews', high-pressure transfers to unusual investments and 'introducer' firms steering savers to specific products. Pension cold calls are banned in the UK. The FCA's ScamSmart resource and the FCA Register are essential checks before acting on any consolidation offer.

Comparing Receiving Schemes

The best receiving scheme is usually the one that fits the saver's long-term plan, not just the cheapest headline rate.

- Total expected cost — platform, dealing and fund OCFs across the saver's pot size and trading style.

- Investment menu — does it include the funds, shares and ETFs the saver intends to hold?

- Drawdown features — flexi-access, UFPLS and partial crystallisations support flexible income.

- Beneficiary and death benefit options — important for estate planning.

- Customer Service quality — online tools, phone support and responsiveness.

- Operator authorisation — confirmed on the FCA Register.

- FSCS cover — eligible investments protected up to £85,000 per firm where a claim is upheld.

Timing the Transfer

Transfers between modern UK DC providers typically complete in two to six weeks. Older schemes can take longer. During the transfer, funds are normally held as cash, meaning the saver is out of the market and misses any gains (or avoids any losses) over that period. Some receiving providers offer 'in-specie' transfers where Assets move without selling — useful for larger pots but not universally available.

Where to Get Help

MoneyHelper (Money and Pensions Service) provides free guidance on UK pensions and consolidation. Pension Wise, through MoneyHelper, offers free appointments for over-50s with DC pensions. For personalised recommendations and DB transfer advice, a regulated financial adviser is required. The Pension Tracing Service helps locate lost pots.

Many UK savers also benefit from speaking with an Accountant when consolidating around significant life events such as approaching retirement, Business sale or relocation overseas. Coordinating pension consolidation with tax planning, ISA usage and estate planning can produce better overall outcomes than addressing each in isolation. Free MoneyHelper guidance and the FCA Register are useful starting points before paid advice.

Pension Consolidation at a Glance

Common UK consolidation considerations for 2026/27.

Key Takeaways

- Consolidation can simplify administration and reduce charges — but can also lose features.

- Active workplace pensions usually remain valuable because of employer contributions.

- Defined benefit transfers are normally cautious and need regulated advice.

- SIPPs are common destinations but not the only option.

- Free guidance via MoneyHelper covers many basic questions.

- Cold-call pension offers are red flags and should be checked with FCA ScamSmart.

- Specialist advice is recommended for most consolidation decisions.

Please wait processing your request...

Please wait processing your request...