_10_10_2025_12_04_10_693162.png)

Index Update: The FTSE 100 index, a key benchmark index for the London stock exchange, was trading up around 0.01% up on 10 October 2025.

Macro Update: Britain saw key economic and market developments on Friday. The CMA granted Google “strategic market status,” its first use of new powers to regulate big tech, citing the firm’s 90% share in UK search. The NIESR urged Finance Minister Rachel Reeves to consider raising income tax to meet a £30 billion revenue gap despite prior pledges not to. BP won an arbitration against Venture Global over an LNG contract breach, seeking over $1 billion in damages. Meanwhile, PMs Modi and Starmer highlighted their India-UK trade deal, expected to lift bilateral trade by £25.5 billion by 2040. The FTSE 100 fell 0.4%, weighed by HSBC’s 5.4% drop on plans to buy out Hang Seng Bank minorities, while Lloyds, Close Brothers, and Aston Martin also declined on financial and sector-specific pressures.

Top Market Movers: Among top gainers on FTSE 100 index, The Sage Group PLC (LSE: SGE) witnessed a rise of 3.15% followed by Compass Group PLC (LSE: CPG) which gained around 2.06%.

Commodity Update: The yen hovered near 153.12 per U.S. dollar, set for its steepest weekly drop in a year as fading prospects of another Bank of Japan rate hike weighed on sentiment. Gold rose 0.71% to $4,000.95, silver gained 0.84% to $47.56, and copper slipped 0.54% to $10,822.45. Brent crude was flat at $65.22, steady after the Israel-Hamas ceasefire eased risk premium, offset by fresh U.S. sanctions on Iran and concerns over weak winter fuel demand.

Our Stance: U.S. economic signals showed mixed trends on Friday as jobless claims rose to 235,000, hinting at early contractor layoffs linked to the government shutdown, while flight delays worsened amid staff shortages at major airports, prompting Transportation Secretary Sean Duffy to warn of dismissals for absentee controllers. Despite these headwinds, U.S. stock futures edged higher, supported by optimism over AI-driven growth and expectations that the rally may broaden into sectors like energy and construction. In Europe, the STOXX 600 remained steady, with automakers and real estate stocks rebounding, while investors awaited political developments in France. Meanwhile, oil prices fell around 1% as easing tensions in the Middle East following an Israel-Hamas truce reduced the market’s risk premium.

FTSE 100

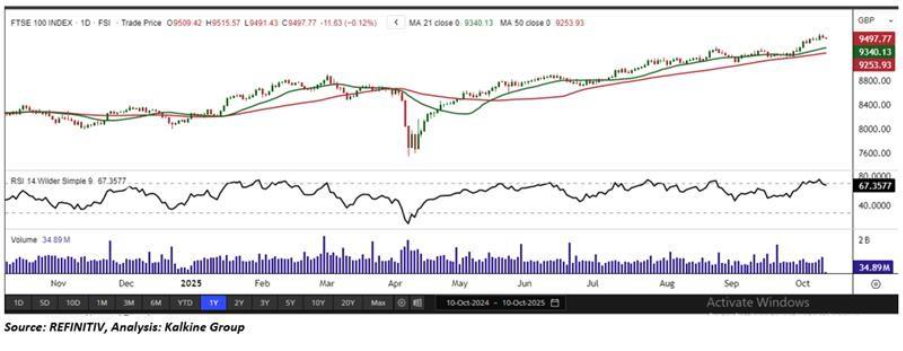

The FTSE 100 fell 0.12% on Friday to close at 9,497.77, forming a bearish candlestick pattern on the daily chart. Despite the minor pullback, the index remains firmly above a key horizontal support level, underscoring strong underlying momentum. Technical indicators remain constructive, with price action holding comfortably above both the 21- and 50-period Simple Moving Averages (SMAs), which serve as dynamic support zones and highlight sustained buying interest. The Relative Strength Index (RSI), at 67.35, signals strengthening momentum and points to a potential shift toward deeper bullish sentiment. A decisive breakout above the immediate resistance zone would confirm the prevailing uptrend and open the way for further upside targets. On the downside, maintaining support at current levels is crucial to preserving the bullish structure, while a breakdown below the moving averages could trigger a near-term corrective phase.

Please wait processing your request...

Please wait processing your request...