Image Source : Krish Capital Pty Ltd

Index Update: The FTSE 100 index, a key benchmark index for the London stock exchange, went down around 0.29% on 29 August 2025.

Macro Update: Britain’s outlook saw fresh pressures as a think-tank urged Finance Minister Rachel Reeves to tax banks on the £22 bn they earn annually from BoE reserves, dragging bank shares on fears of higher levies. Meanwhile, Britain, France and Germany moved to reimpose U.N. sanctions on Iran, raising geopolitical tension. London equities slipped for a third day as utilities and tech names weakened after Nvidia’s results, though miners offered support. Apple opposed UK plans to curb its app store dominance, warning of risks to privacy and innovation, while Diageo announced closure of a Canadian whisky bottling plant to streamline supply chains. Lotus also unveiled plans to cut up to 550 jobs as part of a restructuring to adapt to auto sector challenges.

Top Market Movers: Among top gainers on FTSE 100 index, RENTOKIL INITIAL PLC witnessed a rise of 2.87% followed by CONVATEC GROUP PLC which gained around 1.80%.

Commodity Update: The dollar weakened Friday, on track for a 2% August decline amid rising bets of a Federal Reserve rate cut and concerns over its independence, with President Trump attempting to oust Fed Governor Lisa Cook, who has filed a lawsuit. Gold slipped 0.06% to $3,472.20, silver fell 0.23% to $39.10, while copper gained 0.22% to $9,847.75. Brent crude dropped 0.71% to $67.50, with oil prices set for a weekly rise despite U.S. demand slowdown and Russian supply uncertainty.

Our Stance: The end of the U.S. de minimis tariff exemption for packages under $800 has raised costs for e-commerce firms, small businesses, and consumers, while boosting government revenues and tightening trade flows. At the same time, Federal Reserve Governor Christopher Waller signalled support for a 25-basis-point rate cut in September, with potential further easing over the next few months to cushion labor market weakness. Despite macro uncertainty, Wall Street indices hit record highs as Nvidia’s strong AI-driven results reinforced confidence in technology as a structural growth driver, though concerns over its China exposure and investor sensitivity to lofty valuations remain. Oil markets, meanwhile, stayed volatile—pulled between Russian supply risks and softer U.S. demand as the summer driving season winds down—underscoring the fragile balance between geopolitical pressures, monetary policy shifts, and sector-specific momentum.

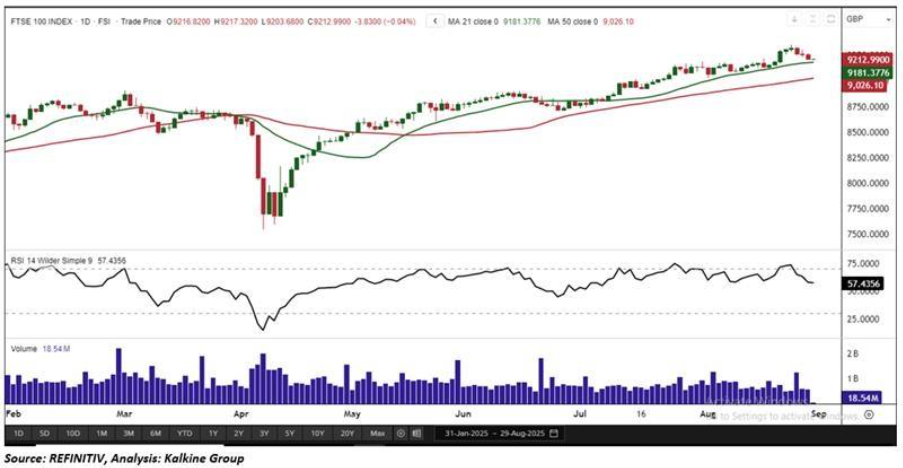

FTSE 100

The FTSE 100 edged lower by 0.04% on Friday to close at 9,212.99, forming a small bearish candlestick on the daily chart. Despite the mild pullback, the index remains firmly above a key horizontal support level, reflecting strong underlying momentum. Technical indicators continue to present a constructive outlook. The price action is comfortably above both the 21-period and 50-period Simple Moving Averages (SMAs), which are acting as dynamic support zones and highlighting sustained buying interest. The Relative Strength Index (RSI) at 57.43 further signals strengthening momentum, pointing toward a possible shift into deeper bullish territory. Looking ahead, a decisive breakout above the immediate resistance zone would reaffirm the prevailing uptrend and open the way for higher targets in the sessions ahead. On the downside, holding above current support and the key SMAs remains critical to preserving the bullish structure, as a breakdown could trigger a near-term corrective phase.

Please wait processing your request...

Please wait processing your request...