_01_28_2026_04_40_08_677083.jpg)

Trending Titans: FTSE 250 Mid-Cap Momentum

The FTSE 250 continues to serve as a fertile hunting ground for investors seeking growth outside the stagnant blue-chip giants, with EW Group (EWG) and Saga PLC (SAGA) emerging as the standout performers this Tuesday, January 27, 2026. While the broader market navigates a complex macroeconomic landscape of fluctuating interest rates and shifting consumer sentiment, these two companies have decoupled from the pack.

Their ascent is fueled by distinct structural shifts: a fintech-led migration at EW Group that is redefining commercial road transport payments, and a balance-sheet-first recovery at Saga that is finally unlocking the value of its asset-rich travel division.

EW Group (WAG Payment Solutions PLC - EWG)

Source: Kalkine Group

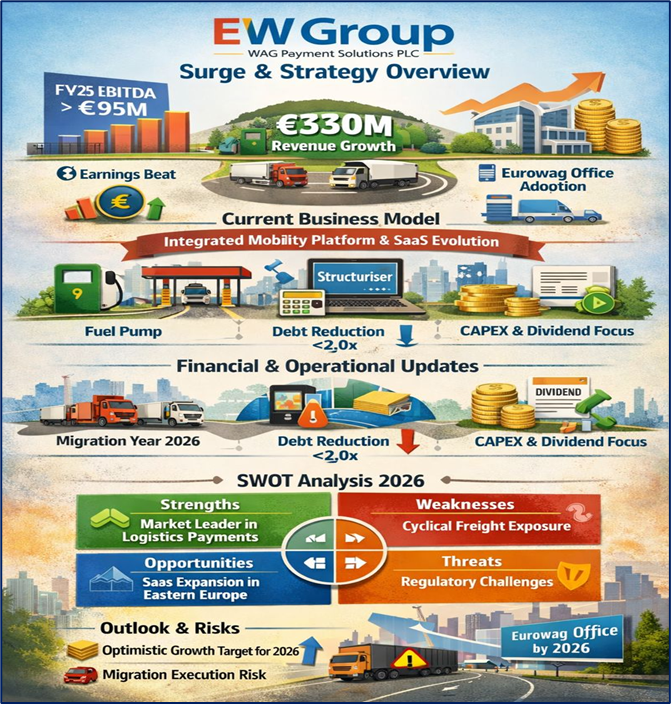

Latest Reasons for Surge & Drivers

- Earnings Beat: The primary catalyst for today's price action is the unaudited trading update indicating that adjusted cash EBITDA for FY25 is estimated to be above previous guidance of €95 million (Alliance News, Jan 27).

- Revenue Growth: The company delivered roughly 13% organic net revenue growth, reaching approximately €330 million, showcasing resilience in the European commercial road transport sector.

- Platform Adoption: Investors are reacting positively to the successful rollout of the "Eurowag Office" platform, with adoption on track to hit 30% of customers by the end of Q1 2026.

Current Business Model

- Integrated Mobility Platform: EWG operates as a one-stop-shop for the commercial road transport industry, providing payment solutions for fuel and tolls, tax refund services, and fleet management software.

- SaaS Evolution: The model is shifting toward a recurring revenue "Software-as-a-Service" (SaaS) structure, exemplified by the recent launch of "Structuriser," an AML/compliance tool for the professional services market (Digital Jersey, Nov 2025).

Latest Financial & Operational Updates

- Migration Year: Management has officially labeled 2026 as a "migration year," focusing on moving the majority of the customer base to the new digital platform to drive long-term margin expansion (Alliance News).

- Debt Reduction: Year-end net debt to adjusted EBITDA is expected to fall below 2.0x, significantly strengthening the balance sheet.

- Dividend Update: While the company has prioritized growth-oriented CAPEX (keeping R&D below the €50 million cap), it maintains a long-term focus on cash generation (Company Update).

Latest SWOT Analysis (2026)

- Strengths: Market-leading position in European logistics payments; high customer retention during platform migration.

- Weaknesses: Exposure to cyclical fluctuations in European freight volumes; high R&D intensity.

- Opportunities: Expansion of the "Structuriser" SaaS tool into new compliance sectors; deeper penetration in Eastern European markets.

- Threats: Rapidly evolving regulatory environment for cross-border payments; potential for increased competition from traditional banking giants.

Outlook & Risks

- Outlook: Guidance for 2026 remains optimistic, with low double-digit net revenue growth expected as the platform migration matures.

- Risks: Execution risk remains the primary concern as the majority of customers must be migrated to the "Eurowag Office" by year-end 2026.

Saga plc (SAGA)

Source: Kalkine Group

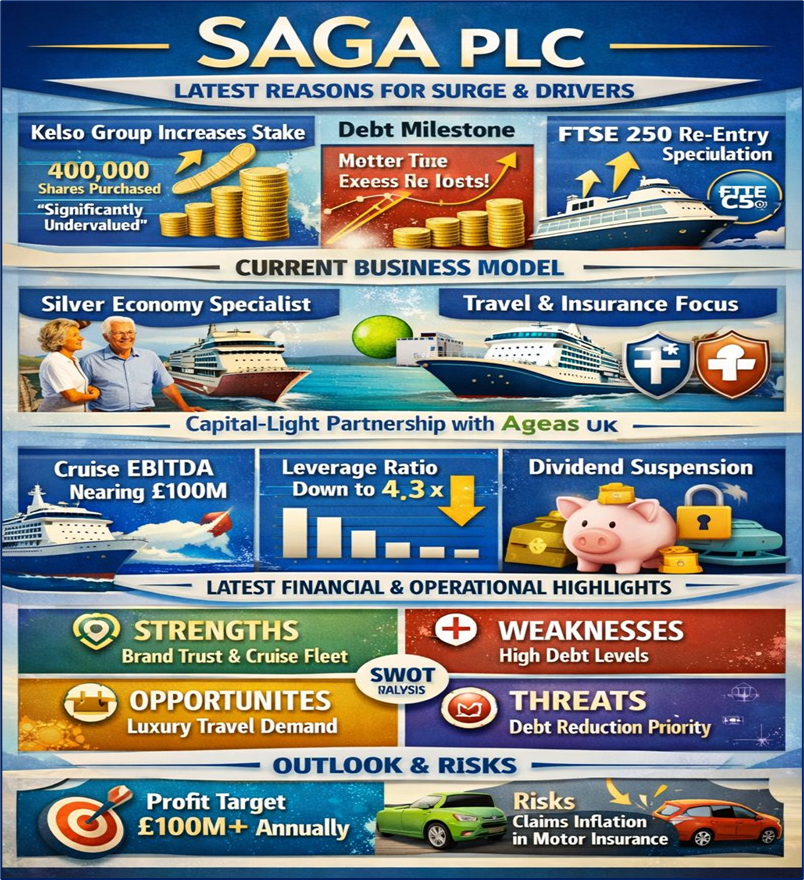

Latest Reasons for Surge & Drivers

- Strategic Stake Increase: Shares are buoyed by recent news that Kelso Group has significantly increased its holding, purchasing 400,000 shares and highlighting the company as "significantly undervalued" (LSE/Kelso, Jan 5).

- Debt Milestone: For the first time in five years, Saga's market capitalization has exceeded its net debt, a psychological and financial turning point for the stock.

- FTSE 250 Re-entry Hopes: As the share price improves, there is increasing speculation regarding a return to the FTSE 250 index, which would trigger mandatory buying from index-tracking funds.

Current Business Model

- Silver Economy Specialist: Saga targets the UK over-50s demographic through two core pillars: Travel (ocean and river cruises) and Insurance (home, motor, and health).

- Capital-Light Pivot: The business is transitioning to a capital-light model, notably through its 20-year partnership with Ageas UK for motor and home insurance (Saga Corporate, Dec 2025).

Latest Financial & Operational Updates

- Cruise Momentum: EBITDA in the ocean and river cruise divisions is now approaching £100 million, reflecting a fourfold increase in revenue for these segments since the IPO (Kelso Announcement).

- Leverage Reduction: The leverage ratio has plummeted from a peak of 12.3x in 2021 to 4.3x as of mid-2025, with internal forecasts targeting below 2.0x by 2030 (Saga PLC).

- Dividend Update: Dividends remain suspended as the company prioritizes debt reduction; however, the board has indicated they will look to reinstate payments as leverage targets are met (Saga Investor Relations).

Latest SWOT Analysis (2026)

- Strengths: Massive brand trust among the wealthy over-50s demographic; high asset backing via its fleet of boutique cruise ships.

- Weaknesses: Historically high debt levels; sensitivity to insurance premium pricing cycles.

- Opportunities: The partnership with Ageas allows for more efficient insurance scaling; high demand for luxury travel post-2025.

- Threats: Increasing competition in the over-50s insurance space; potential for global health or geopolitical events to disrupt travel.

Outlook & Risks

- Outlook: Management is targeting annual underlying profits of at least £100 million, supported by a more streamlined corporate structure.

- Risks: High claims inflation in the motor insurance sector remains a headwind that could dampen profit margins in the short term.

Compelling Conclusion

The surge in EW Group and Saga plc on January 27, 2026, represents two different but equally potent narratives within the FTSE 250. EWG is successfully navigating the "S-curve" of digital transformation, proving that its platform migration is not just a technical update but a financial accelerator. Meanwhile, Saga is demonstrating the power of a "clean" balance sheet, as the market finally begins to value its robust travel assets over its historical debt burdens. Both companies exemplify a shift in investor appetite toward mid-caps that can demonstrate clear operational progress and disciplined deleveraging in an uncertain global economy.

Please wait processing your request...

Please wait processing your request...