The global financial landscape of 2026 has reached a definitive tipping point, where the "Great Mineral Squeeze" has transitioned from a theoretical macro-forecast into an aggressive, wealth-shifting reality. As AI data centres, global grid overhauls, and the localized battery arms race collide with a decade of chronic mining underinvestment, the FTSE’s critical mineral titans have emerged as the ultimate "Fortress Assets" for the modern portfolio. We are no longer merely discussing cyclical commodities; we are witnessing a structural re-rating of companies that own the periodic table, where tier-one assets in copper, lithium, and rare earths are being valued by smart money as the "New Oil."

For the disciplined investor, the current valuation gap between London’s mining elite and their projected 2027 cash flows represents a generational compounding opportunity—a rare window where massive dividend yields meet the explosive upside of a multi-year supply deficit.

Source: Kalkine Group

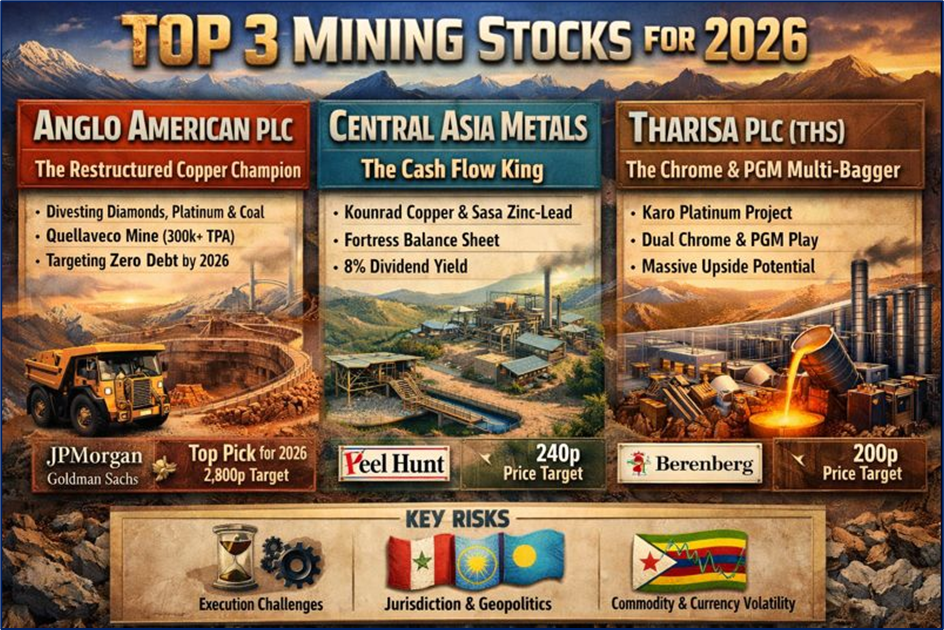

- Anglo American PLC (AAL) - The Restructured Copper Champion

Key Reasons and Drivers

Anglo American is currently undergoing one of the most significant portfolio "reshapes" in mining history. By 2026, the company will have divested its diamond (De Beers), platinum, and coal businesses to become a "pure-ish" copper and premium iron ore play. The primary driver is the Quellaveco mine in Peru, which is reaching steady-state production of 300,000+ tonnes per annum, making Anglo a top-5 global copper producer just as the 2026 supply deficit hits.

Latest Business Model and Financial Updates

The "New Anglo" business model focuses on high-margin, low-cost assets. Operational updates for early 2026 indicate a 10% reduction in overheads following the divestment of non-core units. Net debt is being aggressively targeted for reduction toward a "zero-debt" floor using proceeds from the De Beers separation.

Technical Analysis and Valuation

- Technical: AAL is exhibiting a "Rounding Bottom" formation on the weekly chart, a classic reversal pattern. It recently broke through the 2,600p resistance level.

- Valuation: Following the portfolio slim-down, analysts at Goldman Sachs value the copper business alone at 2,800p, suggesting the market is still getting the iron ore and polyhalite (fertilizer) assets for a significant discount.

Analysts and Smart Money Sentiment

- JPMorgan: Highlighted Anglo as their "Top Pick" for 2026, citing the simplification of the earnings story as a catalyst for institutional re-entry.

- Hedge Funds: Quantitative funds have increased weighting as the stock’s correlation with copper prices has tightened to 0.85.

Risks

- Execution: Complexity in the demerger of the PGM and Diamond units.

- Jurisdiction: Social unrest in Peru remains a recurring operational risk for Quellaveco.

- Central Asia Metals (CAML) - The Cash Flow King

Key Reasons and Drivers

Central Asia Metals is a favorite among "smart money" for its industry-leading margins. Operating the Kounrad copper project in Kazakhstan and the Sasa zinc-lead mine in North Macedonia, CAML is a low-cost producer. The 2026 driver is the "Sasa Life of Mine" extension and the transition to paste-fill mining, which is expected to boost recoveries and lower environmental impact.

Latest Business Model and Financial Updates

CAML operates a "low-capex, high-payout" model. The latest financial update shows a net cash position of approximately $80 million, a rare feat for a mid-tier miner. For 2026, they have guided for stable copper production despite the natural decline of dump-leaching, offset by higher zinc grades.

Technical Analysis and Valuation

- Technical: The stock has been consolidating in a tight range between 180p and 210p. A break above 215p on high volume would signal a move toward the 2022 highs of 250p+.

- Valuation: Trading at a P/E of 7.1x with a trailing dividend yield of nearly 8%, it is one of the cheapest critical mineral plays on the LSE.

Analysts and Smart Money Sentiment

- Peel Hunt: Maintains a "Buy" with a 240p target, noting CAML’s "fortress balance sheet."

- Broker Consensus: 100% of covering analysts have a "Buy" or "Hold" rating; zero "Sells."

- Smart Money: High retail and institutional loyalty due to the company's 10-year track record of consistent dividend payments.

Risks

- Single Asset Risk: Heavily dependent on the Kounrad site.

- Geopolitics: Proximity of Kazakhstan to Russia/China creates a perceived risk premium.

- Tharisa PLC (THS) - The Chrome & PGM Multi-Bagger

Key Reasons and Drivers

Tharisa is a dual-listed (London/Johannesburg) miner that provides a unique play on two critical minerals: Platinum Group Metals (PGMs) and Chrome. The "Wealth Compounding" story for 2026 revolves around the Karo Platinum Project in Zimbabwe. Once fully commissioned in 2026, Karo is expected to double the company’s PGM production, transforming it into a mid-tier major.

Latest Business Model and Financial Updates

Tharisa uses a proprietary "co-extraction" model where chrome and PGMs are mined from the same reef, effectively making one a "free" byproduct of the other. This allows them to remain profitable even when PGM prices are low. 2026 financial guidance predicts a 40% jump in EBITDA as the Karo project ramps up.

Technical Analysis and Valuation

- Technical: THS has recently touched a 52-week high of 129p. The stock is currently trading above its 50-day and 200-day moving averages, indicating a confirmed bullish trend.

- Valuation: With a P/E ratio of roughly 4.9x, Tharisa is priced for failure despite its massive growth pipeline. Berenberg recently set a price target of 200p, implying nearly 60% upside.

Analysts and Smart Money Sentiment

- Berenberg Bank: Reissued "Buy" rating, highlighting the "valuation disconnect" between current earnings and 2026 growth.

- SP Angel: Noted that "the growth potential does not look to be priced into the shares."

- Smart Money: Increasing interest from "Value" funds looking for a hedge against the high valuations in the tech sector.

Risks

- Commodity Pricing: Sensitivity to the volatile PGM market (platinum/palladium).

- Zimbabwe Risk: Currency and regulatory instability in Zimbabwe could affect the Karo project's timeline.

Conclusion

While the "Big Three" (Glencore, Rio, Antofagasta) provide the foundation for a 2026 portfolio, these "Next Three" (Anglo, CAML, Tharisa) offer the specific catalysts needed for multi-bagger returns. Anglo provides the "Event Driven" value unlock; CAML provides the "Income Compounder" floor; and Tharisa provides the "Growth Surge" from new asset commissioning.

Please wait processing your request...

Please wait processing your request...