Senior PLC (LSE: SNR), the FTSE 250 engineering powerhouse, witnessed a significant 8% share price surge on January 22, 2026, after the company issued a bullish post-close trading update that caught the market's attention. The Rickmansworth-based manufacturer, a critical supplier to the global aerospace and energy sectors, revealed that its full-year 2025 adjusted profit before tax is now expected to be "comfortably above previous expectations."

This marks the second time in just three months that the group has lifted its guidance, signaling a powerful recovery in commercial aviation and a disciplined execution of its "pure-play" strategic pivot. Investors responded with high volume, pushing the stock toward its 52-week highs as the company nears the completion of its major structural reorganization.

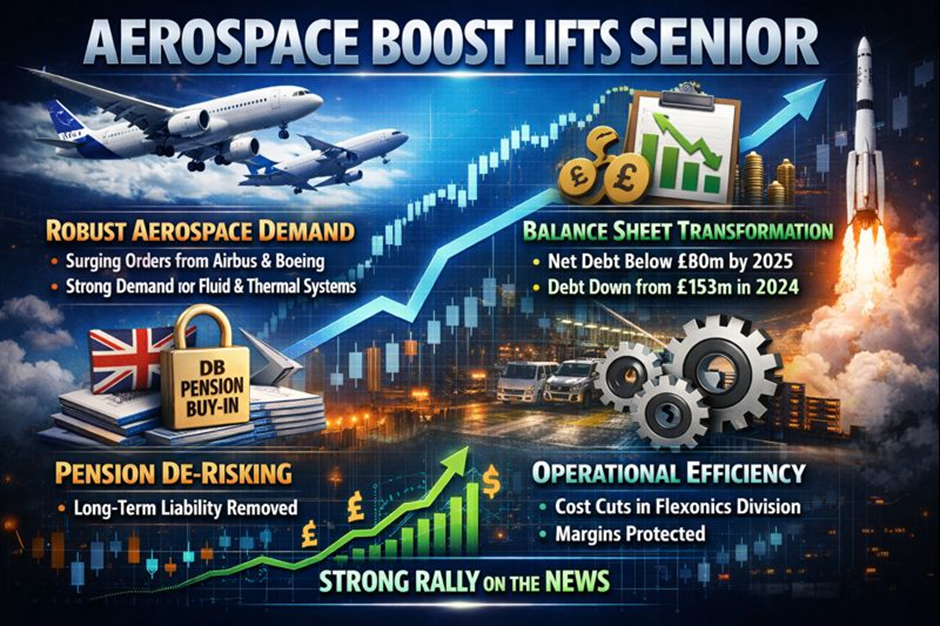

Latest Key Reasons for the Surge and Market Drivers

Source: Kalkine Group

The primary catalyst for today's rally is the unanticipated strength of the Aerospace division, which outperformed even the optimistic forecasts set in November 2025. Key drivers include:

- Robust Aerospace Demand: Increased production rates from major OEMs like Airbus and Boeing have filtered down to Senior’s high-technology fluid conveyance and thermal management systems.

- Balance Sheet Transformation: The company confirmed that net debt is expected to fall below £80 million by year-end 2025 (down from £153 million in 2024), significantly reducing interest costs and leverage.

- Pension De-risking: A successful buy-in of the UK defined benefit pension scheme has removed a long-term liability from the books, clearing the path for more aggressive capital allocation.

- Operational Efficiency: Despite a softening in the land vehicle market, Senior’s cost-cutting measures in the Flexonics division have protected margins.

Current Business Model and Strategic Pivot

Senior operates as an international engineering and manufacturing group with a presence in 12 countries. Historically a diversified industrial, the current model is shifting toward a "Pure-Play" Fluid Conveyance and Thermal Management (FCTM) specialist.

- Aerospace Division: Focuses on high-technology components for airframes and engines, including fluid systems, ducting, and thermal insulation.

- Flexonics Division: Provides specialized bellows, expansion joints, and heat exchangers for land vehicles, nuclear power, and green energy applications.

- Strategic Realignment: The business model now prioritizes high-margin, IP-rich components that support the transition to a low-carbon economy, such as hydrogen fuel cell systems and sustainable aviation technologies.

Latest Financial and Operational Updates (Source: Senior PLC Trading Update, Jan 2026)

- Profit Guidance: Full-year 2025 adjusted profit before tax is "comfortably above" the consensus of approximately £43 million (Company Update).

- Leverage: Net debt to EBITDA ratio is projected to fall below 1.0x, a dramatic improvement from 1.8x at the end of 2024 (Company Update).

- Divestments: The sale of the Aerostructures business is nearing completion, with initial cash proceeds already contributing to the debt reduction (Company Source).

- Operations: January 2026 trading has "started well," maintaining the momentum from the final quarter of 2025 (Company Update).

- Dividend Update: While final 2025 figures are due in March, the board previously hiked the interim dividend by 13% to 0.85p, signaling a commitment to progressive returns (Interim Results).

Latest SWOT Analysis (2026)

Strengths

- Market-leading positions in specialized fluid conveyance.

- Strong relationship with Tier-1 aerospace OEMs (Airbus, Rolls-Royce).

- Significantly de-risked balance sheet and low leverage (<1.0x).

- High "A-List" CDP rating for climate transparency.

Weaknesses

- Exposure to cyclical land vehicle markets in the Flexonics division.

- Dependency on Boeing and Airbus production schedules.

- History of low free cash flow, though this is currently reversing.

Opportunities

- Expanding "Green" aerospace technologies (hydrogen and electric flight).

- Further accretive M&A in the thermal management space using new debt capacity.

- Recovery in wide-body aircraft production driving higher-value component sales.

Threats

- Global supply chain bottlenecks impacting the delivery of raw materials.

- Potential for extended weakness in European and North American land vehicle demand.

- Inflationary pressures on labor and specialized materials.

Outlook and Risks

The outlook for Senior PLC heading into the remainder of 2026 remains optimistic yet cautious. The company’s focus on the "Aerospace Supercycle" provides a strong tailwind, while the successful divestment of the Aerostructures business simplifies the group structure.

Key Risks:

- Production Delays: Any further technical or regulatory hurdles for major aircraft programs could slow revenue growth.

- Macroeconomic Headwinds: A broader slowdown in global industrial production could hit the Flexonics division's recovery.

- Geopolitical Instability: Conflicts affecting global trade routes or defense spending priorities could shift the demand landscape.

Compelling Conclusion

Senior PLC has successfully navigated a complex multi-year turnaround, emerging in 2026 as a leaner, more focused, and financially robust entity. Today's 8% surge is more than just a reaction to a profit beat; it is a validation of a strategy that has seen the company shed non-core assets, slash debt, and align itself with the accelerating recovery of global aviation. With leverage at record lows and the Aerospace division firing on all cylinders, Senior appears well-positioned to capitalize on the next phase of the industrial cycle, making its upcoming full-year results on March 2, 2026, a critical date for the market.

Please wait processing your request...

Please wait processing your request...