Image source: © 2025 Krish Capital Pty.Ltd

Highlights

- ANTO’s FY24 revenue rose by 4.6% YoY while EBITDA surged by 11.0% YoY.

- The management declared the final dividend of US 23.5 cents per share which was paid on 12 May 2025.

- ANTO reaffirmed FY24 copper output guidance and capex at USD 3.9 Billion, with stable cost projection.

Antofagasta PLC (LSE: ANTO), a FTSE 100 company, operates four copper mines and a transport division serving mining clients in Northern Chile.

In the financial year 2024 (FY24), the company’s revenue increased by 4.6% YoY to USD 6,613.4 million, driven by a 7% rise in average realized copper prices, which was partly offset by lower copper sales volumes due to shipment delays. EBITDA surged by 11.0% YoY to USD 3,426.8 million, supported by higher copper prices and continued cost discipline under the competitiveness programme. Profit before tax rose by 5.4% YoY to USD 2,071.1 million, up from USD 1,965.5 million in FY23.

During the first quarter of the financial year 2025 (Q1FY25), the company’s copper output rose by 20% YoY to 154,700 tonnes due to improved ore grades at Centinela and consistently high throughput at both Centinela and Los Pelambres concentrators. Gold production grew by 29% YoY to 42,900 ounces, while molybdenum output rose 15% to 3,100 tonnes, driven by higher-grade recoveries at Centinela concentrates. Net cash costs fell by 20% YoY to USD 1.54/lb compared to Q1FY24, supported by higher by-product credits and efficiency in base production costs.

Business Updates

Antofagasta reported steady progress on construction at Centinela’s second concentrator and Los Pelambres’ growth projects, with ongoing concrete pouring, equipment installation, and pipeline trenching to support its medium-term processing capacity expansion objectives. The management declared the final dividend of US 23.5 cents per share which was paid on 12 May 2025.

Company Outlook

ANTO reaffirmed its full-year copper production guidance of 660,000 to 700,000 tonnes, with no changes to volume expectations. Group cash costs are projected between USD 2.25–2.45/lb (pre-credits) and USD 1.45–1.65/lb (post-credits), while total capex remains at USD 3.9 billion as guided.

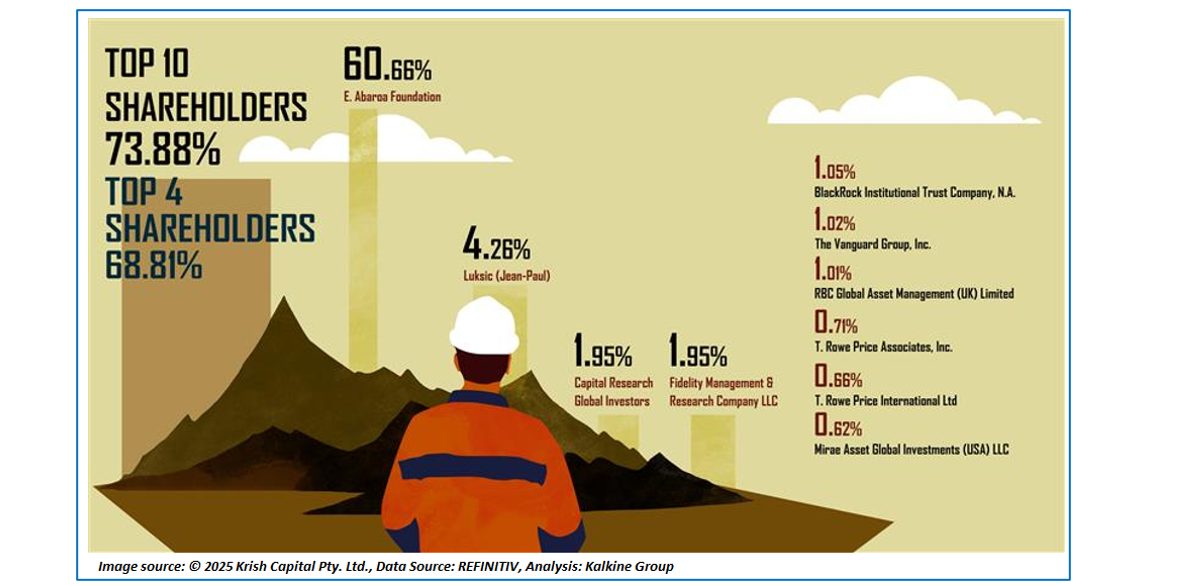

Top 10 Shareholders

The top 10 shareholders of ANTO collectively hold approximately 73.88% of the company’s total shares, with the largest stakes held by E. Abaroa Foundation at around 60.66% and Jean-Paul Luksic at roughly 4.26%.

Stock Information

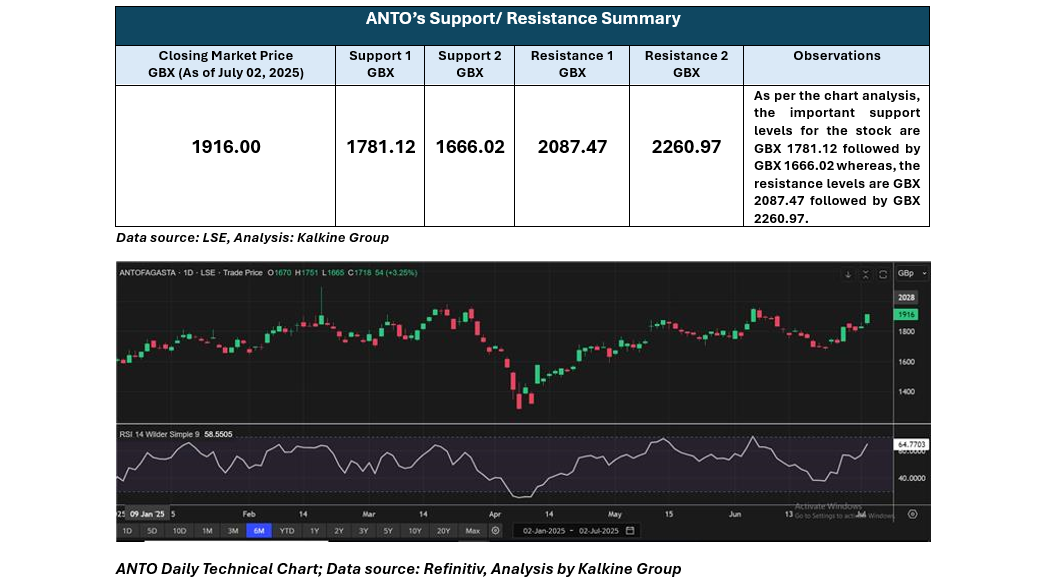

The stock price of ANTO has gone up by ~6.14% and ~20.50% over the past month and past six months, respectively.The stock has a 52-week low and 52-week high of GBX 2,239 and GBX 1,278 respectively, with a closing price of GBX 1916 as of 02 July 2025.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference data for all price data, currency, technical indicators, support, and resistance levels is 02 July July 2025. The reference data in this report has been partly sourced from EODHD/Others.

Technical Indicators Defined

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock

Please wait processing your request...

Please wait processing your request...