Image source: Shutterstock

Highlights

- ANTO’s H1 FY24 revenue rose 3.6% to USD 2,995.20 million, driven by higher commodity prices.

- The company’s Q3 FY24 saw a 15% increase in copper production and a 54% surge in gold output.

- FY24 guidance remains steady, with copper production projected between 670,000 and 710,000 tonnes.

Antofagasta PLC (LSE: ANTO) is a company listed on the FTSE 100 index. It specialises in copper mining. It operates four copper mines in Chile and also has a transportation division in Northern Chile to support its mining clients.

In H1 FY24, ANTO reported a revenue of USD 2,995.20mn, reflecting a year-on-year increase of 3.6% from USD 2,890.10mn in H1 FY23. This growth was primarily driven by higher average realized sales prices for the commodities sold, which helped offset a decline in overall production during the same period. Additionally, EBITDA rose to USD 1,394.40mn, up 4.8% from USD 1,331.00mn in H1 FY23, supported by increased revenue that counterbalanced higher production costs and lower depreciation expenses.

Recent Business Update

On October 16, 2024, ANTO announced its Q3 FY24 production update, highlighting a significant 15% increase in copper production. This growth was primarily driven by improved copper grades and recoveries at the Centinela mine, along with inventory destocking at Los Pelambres. Additionally, gold production saw a remarkable surge of 54% in Q3, due to higher grades at Centinela. However, year-to-date gold output remains 17% lower than the previous year, reflecting ongoing grade challenges compared to Q2 FY24.

In terms of financial management, ANTO demonstrated cost control by maintaining its cash cost guidance for 2024. In Q3, net cash costs decreased by 17%.

Furthermore, on September 12, 2024, the company declared an interim dividend of GBX 6.06 cents per share for the first half of FY24, which was paid out on September 20, 2024.

Company Outlook

The company’s guidance for FY24 remains consistent with previous forecasts. Group copper production is projected to range between 670,000 and 710,000 tonnes, with expectations for quarterly production to increase steadily throughout the year. The cash cost guidance is set at USD 2.40/lb before by-product credits and USD 1.70/lb after credits. Additionally, the capital expenditure target remains unchanged at USD 2.7 billion.

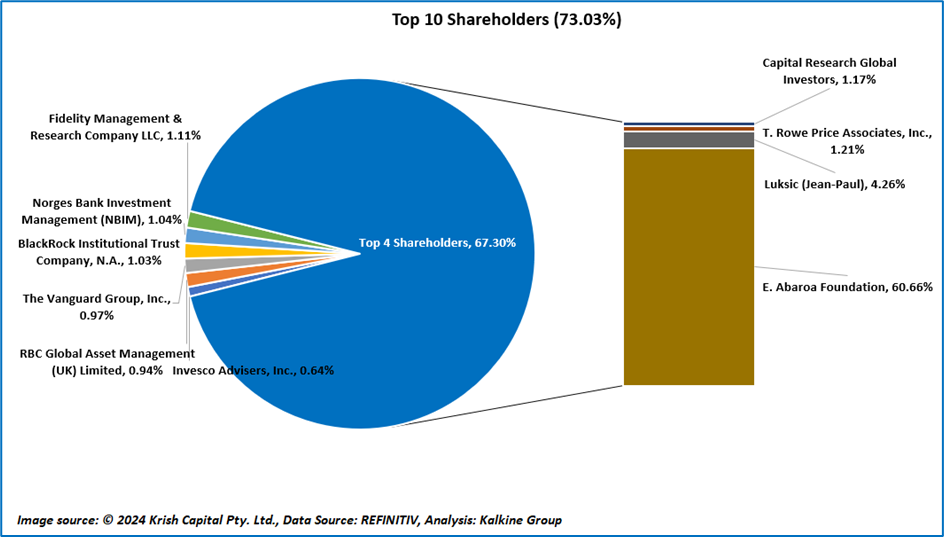

Top 10 Shareholders

The top 10 shareholders of ANTO hold approximately 73.03% of the total shares. E. Abaroa Foundation owns the largest share, with about 60.66% stake. Jean-Paul Luksic follows with around 4.26% shareholding. This information is illustrated in the chart below:

Price Information

The stock price of ANTO has increased by approximately 4.73% over the past three months. However, it has declined by about 15.42% in the last six months. Its 52-week low is GBX 1,280.00, while the high is GBX 2,425.00. Currently, the stock is trading above the average of these 52-week highs and lows. The stock’s closing price as of 22 Oct 2024 is GBX 1829.50.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference data for all price data, currency, technical indicators, support, and resistance levels is 22 October 2024. The reference data in this report has been partly sourced from EODHD/Others.

Please wait processing your request...

Please wait processing your request...