The FTSE 100 is witnessing a fascinating divergence in fortune and strategy this Friday, January 23, as two distinct heavyweights - Ashtead Group and JD Sports Fashion - command investor attention with robust upward momentum. While the broader market grapples with macroeconomic calibration, these two giants are trending not on speculative hype, but on concrete strategic pivots that have reassured a jittery institutional base.

For Ashtead, the narrative is one of capital discipline and a decisive trans-Atlantic shift, fueling optimism with a massive buyback program ahead of its historic US listing. Conversely, JD Sports is enjoying a "relief rally," having defied the gloom hanging over the UK high street by proving that its North American expansion is finally acting as the promised hedge against domestic stagnation.

Today’s movements underscore a critical theme for 2026: resilience is no longer just about operational efficiency; it is about geographical diversification and shareholder return velocity.

Ashtead Group: The Trans-Atlantic Capital Engine

Source: Kalkine Group

Latest Drivers of Surge

The primary catalyst propelling Ashtead’s stock today is the aggressive confirmation of shareholder returns coupled with structural corporate changes. The company has successfully executed a steadying of its share price following the announcement of a fresh $1.5 billion share buyback program. This capital deployment is strategically timed to bridge the gap before its imminent primary listing move to the New York Stock Exchange (NYSE), scheduled for March 2, 2026. Investors are reacting positively to the board's confidence in its cash flow generation, viewing the buyback as a definitive signal that the company considers its stock undervalued relative to its US peers.

Operational & Financial Updates (Source: Ashtead Group Jan 2026 Update)

- Financial Performance: Recent operational updates confirm that revenue and profits remain broadly in line with expectations, despite a challenging inflationary environment. The company continues to guide for rental revenue growth of 0-4% for the full year.

- Capital Allocation: The headline driver is the commencement of the new $1.5 billion buyback programme. This follows the completion of previous tranches, signaling a relentless focus on EPS accretion.

- Dividend: An interim dividend of 37.5 US cents per share (up 4% year-on-year) has been confirmed, with payment scheduled for February 2026, reinforcing its status as a progressive income payer.

- Listing Shift: The operational focus is heavily tilted towards the administrative and legal completion of the move to the US, where the bulk of its "Sunbelt Rentals" revenue is generated.

Current Business Model

Ashtead operates a capital-intensive rental model, primarily trading under the Sunbelt Rentals brand. The core premise is high-utilization fleet management—renting out industrial, construction, and general equipment to a diverse customer base ranging from massive infrastructure contractors to local DIY markets. The model thrives on "mega-projects" in the US (semiconductor plants, green energy infrastructure) which provide long-term visibility on rental demand, insulating the business from short-term cyclical dips in residential construction.

SWOT Analysis

- Strengths: Dominant market share in the US (second largest); robust cash flow generation; excellent fleet management technology; heavy exposure to government-backed infrastructure spending.

- Weaknesses: High capital expenditure requirements; significant debt load (though manageable); sensitivity to interest rate fluctuations which impact borrowing costs for fleet expansion.

- Opportunities: The NYSE relisting could unlock a higher valuation multiple comparable to US peers like United Rentals; continued expansion into "specialty" rentals (power, HVAC, flooring) which offer higher margins.

- Threats: A severe recession in the US construction sector; supply chain disruptions delaying fleet renewal; potential regulatory changes in US tax or labour laws.

Outlook

The outlook for Ashtead is cautiously optimistic but structurally bullish. The pivot to the US main market is expected to widen the investor pool, potentially reducing the "UK discount" historically applied to its valuation. While the economic backdrop remains "tough," the company's reliance on long-term structural projects provides a safety net that few FTSE peers possess.

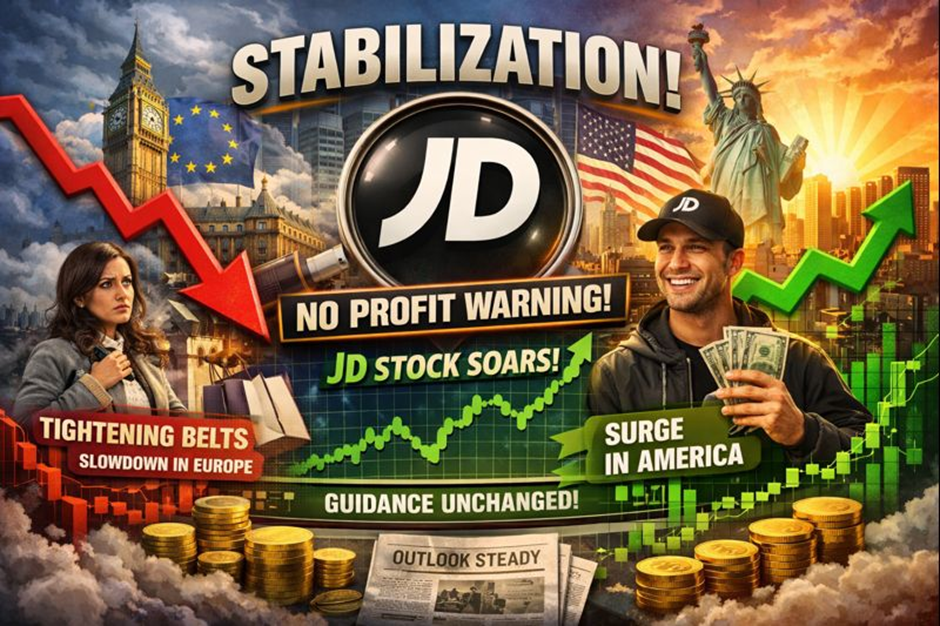

JD Sports Fashion: The North American Hedge Pays Off

Source: Kalkine Group

Latest Drivers of Surge

JD Sports is trending today largely due to a "stabilization" narrative. After a period of volatility and concerns over the "peak leisure" trend, the latest trading update provided much-needed reassurance. The key driver is the divergence in regional performance: while the UK and Europe remain soft due to consumer belt-tightening and weather impacts, the North American division has delivered a surprise upside. Investors are bidding up the stock on the news that full-year profit guidance remains unchanged, effectively removing the "profit warning risk" that had been priced into the shares.

Operational & Financial Updates (Source: JD Sports Fashion Jan 2026 Trading Update)

- Guidance Affirmation: The company confirmed it expects Profit Before Tax and Adjusting Items (PBTAI) for FY26 to be approximately £849 million, aligning with current market consensus.

- Sales Performance: Like-for-like (LFL) sales for the fourth quarter (to date) dipped 1.8% globally. However, the standout metric was North America, which flipped to positive LFL growth of +1.5%, significantly outperforming the negative trends seen in the UK (-5.3%) and Europe (-3.4%).

- Cash Flow: The group remains on track to generate free cash flow of roughly £400 million for the financial year, supporting ongoing investment in distribution automation.

- Margins: Gross margins are expected to be roughly 50 basis points lower, a calculated trade-off to maintain volume through promotional activity during the holiday season.

Current Business Model

JD Sports operates as a premium multichannel retailer of sports fashion and outdoor clothing. Its "King of Trainers" brand positioning relies on exclusive access to "tier-one" product lines from major global brands like Nike, Adidas, and New Balance. The model is increasingly pivoting away from pure high-street retail toward a digitally integrated "lifestyle" ecosystem. Crucially, the business model is now geographically hedged, with the US acquisition strategy (Finish Line, Hibbett) providing a counterweight to the mature UK market.

SWOT Analysis

- Strengths: Unrivaled relationships with key suppliers (Nike/Adidas) securing exclusive stock; strong cash generation; successfully integrating US acquisitions; agile "multi-fascia" retail strategy.

- Weaknesses: Heavy reliance on a single supplier (Nike) for a large portion of revenue; declining footfall in UK legacy stores; lower margins in the online channel due to returns and shipping costs.

- Opportunities: Expansion of the "JD" banner across the US to replace weaker regional brands; growth in under-penetrated markets like the Middle East; leveraging loyalty programs to drive repeat value.

- Threats: "Innovation lull" from major brands (e.g., Nike lacking new hit products); aggressive discounting by competitors impacting margins; rapid shifts in youth fashion trends away from athleisure.

Outlook

JD Sports faces a "muted" growth environment for FY27, but the stock's resilience today suggests the market believes the worst is over. The strategic focus will be on operational efficiency—automating supply chains in Europe and rolling out the stronger "JD" brand format in the US. If North America continues its trajectory, it will likely become the primary engine of valuation growth, rendering the UK market less critical to the overall group performance.

Conclusion

The concurrent rise of Ashtead and JD Sports on January 23 offers a microcosm of the intelligent investor's playbook in 2026. Ashtead demonstrates the power of capital structure engineering and the pursuit of higher valuations across the Atlantic, effectively telling London that its true worth lies in New York. JD Sports, meanwhile, illustrates the vital importance of geographic diversification, using American growth to bandage British wounds. Both companies have weathered their respective storms—one through financial muscle, the other through retail agility—and have emerged with their investment cases not just intact, but battle-hardened. For the market watcher, these moves signal that while the macroeconomic tide may be choppy, companies with clear, executed strategies can still command a premium.

Please wait processing your request...

Please wait processing your request...