Key Takeaways: The Retail Pulse Summary

- The Stock Spark: Ashtead Group PLC (LSE: AHT) saw a significant stock rise on Friday (December 12, 2025), closing up over 2.5% after being up around 3.7% earlier in the week, driven primarily by strong strategic announcements.

- The Big News: The company, which trades under the Sunbelt Rentals brand, announced a new $1.5 billion share buyback program to coincide with its planned primary listing move to the NYSE in March 2026. This signals management's confidence and commitment to shareholder returns.

- Cash is King: The latest financial update (H1 2026 results) highlighted record free cash flow (FCF) generation of $1.1 billion, a massive 164% year-over-year increase, despite moderate revenue growth.

- Mega-Projects vs. Main Street: Growth is being underpinned by a boom in large-scale 'mega-projects' in North America, successfully offsetting the current "moderation" in local, non-residential construction markets.

Source: Kalkine Group

The Drivers: Why the FTSE 100 Stock Climbed

Ashtead's strong movement on the FTSE 100 was a response to several interconnected factors, announced during and following its Half-Year results:

1. The Share Buyback Buzz: Confident Capital Return

The headline driver was the announcement of a new $1.5 billion share repurchase program. This massive commitment, coming on the heels of an existing buyback, serves as a powerful signal from management:

- Confidence in FCF: It demonstrates the Board's conviction in the company's ability to generate substantial and sustainable Free Cash Flow going forward.

- US Listing Catalyst: The new program is strategically timed to begin on March 2, 2026, coinciding with the shift of the company's primary listing from the London Stock Exchange (LSE) to the New York Stock Exchange (NYSE). This financial maneuver is often viewed positively by the market as it concentrates ownership and can enhance earnings per share.

2. Record Free Cash Flow Generation

The sheer volume of cash generated was a standout feature in the H1 2026 results. A 164% surge in Free Cash Flow (FCF) to $1.1 billion reassured investors about the financial health and flexibility of the business, particularly in a mixed operating environment. This cash generation is the engine funding the large buyback.

3. US Mega-Project Strength

The company successfully leveraged its presence in 'mega-projects'—large infrastructure, industrial, and manufacturing projects in North America. This strength provides a critical buffer against the softer performance in the more cyclical local non-residential construction market, which has been experiencing a slowdown.

Ashtead's Business Model: The Rental Powerhouse

Ashtead operates primarily through its Sunbelt Rentals brand, making it one of the largest equipment rental companies globally, with a dominant presence in North America and a strong position in the UK.

The "Buy-Rent-Sell" Engine

Ashtead’s model is simple but effective:

- Buy: Purchase a broad, technologically advanced fleet of equipment (from scaffolding and hand tools to heavy machinery) from leading manufacturers.

- Rent (Sunbelt Rentals): Lease the equipment on a short-term basis to a diverse base of customers across construction, industrial, government, and emergency services.

- Sell: Sell older, well-maintained equipment into the second-hand market, generating additional revenue and funding the next cycle of fleet investment.

Strategic Pillars (Sunbelt 4.0)

The current strategy, known as Sunbelt 4.0, focuses on:

- General Tool and Specialty: Offering a dual-pronged approach, balancing general construction tools with high-margin, technical specialty equipment (e.g., climate control, temporary power).

- Cluster Strategy: Building density in local markets to improve logistics, service response times, and equipment utilization rates.

- Digitalization: Investing heavily in technology for better fleet management, customer service, and dynamic pricing.

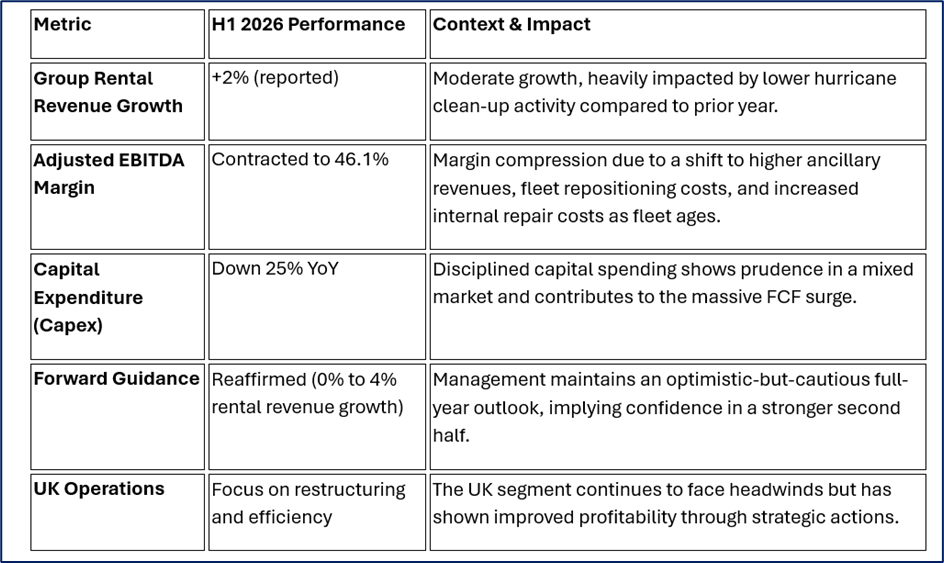

Latest Business Updates: Navigating the Headwinds

Source: Company Data, Kalkine Group

Key Risks and Headwinds: Looking Under the Hood

While the buyback and FCF are bullish signals, key risks remain for investors to consider:

- The Economic Cycle: Ashtead's business is deeply tied to the construction and industrial cycles. A prolonged economic downturn or a significant rise in borrowing costs could suppress demand for equipment rental.

- Interest Rates: The business is capital-intensive, requiring debt to fund its fleet purchases. High interest rates increase financing costs, directly impacting profit margins.

- Margin Pressure: Recent results show margin contraction due to higher repair costs (fleet aging) and a change in revenue mix. Sustained margin pressure could erode profitability.

- Competition: The equipment rental market is highly competitive, risking pressure on rental rates and utilization levels.

- US Listing Volatility: The move to the NYSE is a major undertaking. While aimed at greater US visibility, it introduces short-term execution risk and could lead to changes in its shareholder base.

Conclusion

Ashtead Group's significant stock surge was a robust market reaction, driven primarily by the announcement of a new $1.5 billion share buyback program and exceptional Free Cash Flow (FCF) generation. This financial strength provides a critical buffer, allowing the company to aggressively return capital while successfully leveraging its dominant position in lucrative North American mega-projects to offset softer demand in the local non-residential construction market. The upcoming shift of its primary listing to the NYSE, paired with the buyback, underscores management's confidence and strategic focus on enhancing shareholder value and market visibility in its core operating region.

Source: Trading View, 12 December 2025

Please wait processing your request...

Please wait processing your request...