Snapshot: Why The 26% Surge?

Atlantic Lithium (LSE: ALL) has posted a massive ~26% intra-day gain on the FTSE AIM market today. After months of regulatory stagnation, the floodgates have opened. The primary catalyst is the submission of the revised Mining Lease to the Ghanaian Parliament, signaling the final step before full ratification.

Combined with a rebounding global lithium spot price and a strengthened partnership with the newly formed Elevra Lithium (formerly Piedmont/Sayona), investors are rushing back in to catch the re-rating as ALL transitions from "developer" to "near-term producer."

Key Reasons For Today's Rally

Source: Kalkine Group

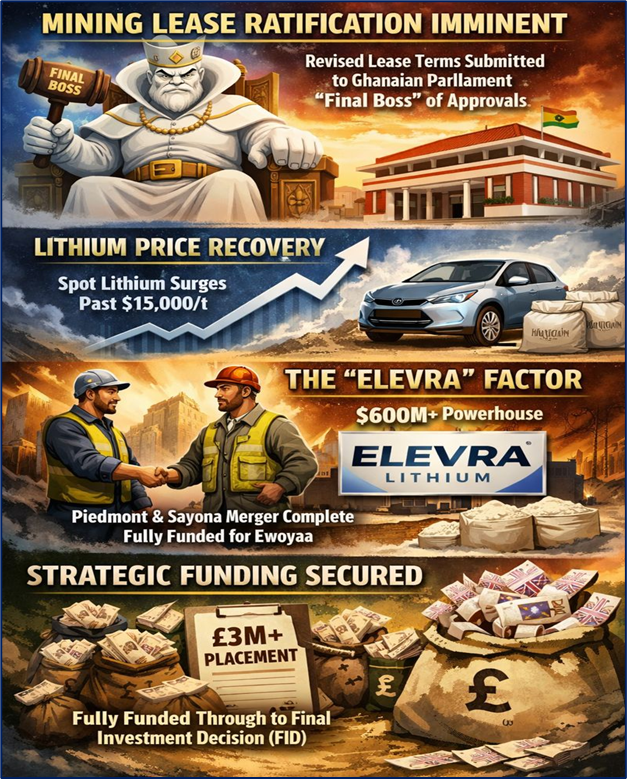

- Mining Lease Ratification Imminent: The Company has officially submitted the revised Mining Lease terms to the Ghanaian Parliament’s Select Committee. This is the "final boss" of regulatory approvals. The market is pricing in a high probability of success.

- Lithium Price Recovery: Spot lithium carbonate prices have rallied in Q4 2025, breaking the psychological $15,000/t barrier, driven by renewed EV demand in China and supply discipline from majors.

- The "Elevra" Factor: The uncertainty around funding partner Piedmont Lithium is gone. Piedmont’s merger with Sayona Mining to form Elevra Lithium (completed late 2025) has created a $600M+ heavy-hitter that is fully committed to funding Ewoyaa’s construction.

- Strategic Funding Secured: The recent closure of the £3M+ placement (via Long State) ensures the company is fully funded through to the Final Investment Decision (FID).

Deep Dive: Strategic Drivers

1. The "Golden Ticket" (Lease Ratification)

The delay in 2024/2025 was due to Ghana’s desire to maximize state revenue. The revised terms submitted today likely include the previously agreed increased royalty (10%) and state equity stake (13%), but the submission itself confirms that both the Company and the Ministry of Lands have aligned. Parliament’s ratification is the trigger for the MIIF (Minerals Income Investment Fund) to release its substantial $32.9M project investment.

2. Business Model Evolution (The Elevra Pivot)

ALL is no longer just a junior explorer; it is the operator of a joint venture with a major producer.

- Old Model: Rely on Piedmont Lithium for funding.

- New Model: Partner with Elevra Lithium (ASX: ELV / Nasdaq: ELVR). Elevra holds the earn-in rights to 50% of the project. This partnership reduces execution risk significantly, as Elevra brings operational expertise from its North American Lithium (NAL) operations in Canada.

3. Operational Readiness

While the lawyers argued, the engineers worked.

- Permits in Hand: EPA Permit (Sept 2024) and Mine Operating Permit (Oct 2024) are already secured.

- Shovel Ready: The Ewoyaa Lithium Project is effectively "shovel ready." Once Parliament stamps the lease, early works can begin almost immediately.

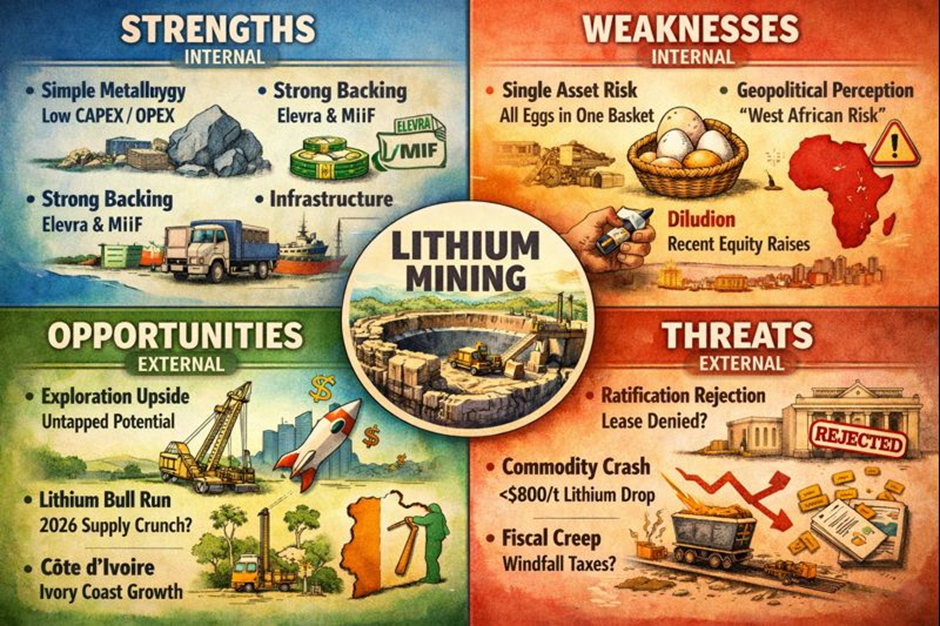

Swot Analysis

Source: Kalkine Group

Latest Financial & Operational Updates

- Cash Position: Healthy following the December 2025 dual-tranche placement (~£4M total raised recently via Long State Investments). Burn rate remains low as major CAPEX is deferred until FID.

- Project Economics (DFS Refresher):

- Post-Tax NPV8: ~$1.3 Billion USD (huge upside vs current market cap).

- IRR: ~94% (Exceptional).

- Payback: < 20 months.

- Production: ~365,000 tonnes of spodumene concentrate per annum.

- MIIF Investment: The $32.9M investment from Ghana’s sovereign wealth fund is currently pending ratification. Once signed, this non-dilutive cash injection will likely trigger another re-rate.

Risks: What Could Go Wrong?

- "Sell the News": Retail investors often buy the rumor and sell the news. Once the actual ratification stamp occurs, we might see a short-term dip as profit-takers exit.

- Parliamentary Gridlock: If the Ghanaian Parliament delays the vote past Q1 2026 due to unrelated political stalling (e.g., election cycles or budget disputes), momentum will die.

- Elevra’s Priorities: Merged entity Elevra has assets in Canada and the US. Investors must ensure Ewoyaa remains a "Priority 1" capital allocation for them.

Conclusion: The Final Hurdle

Atlantic Lithium has effectively de-risked the technical and financial aspects of the Ewoyaa project. The 26% surge today is the market acknowledging that the political risk—the final hang-up—is evaporating.

With a low-capex start-up, a massive partner in Elevra, and a recovered lithium price environment, ALL is arguably the most undervalued near-term producer on the AIM. The ratification of the Mining Lease is the key that unlocks the MIIF cash, the Elevra construction funding, and the path to first spodumene in 2027.

Verdict: The waiting game is almost over. If ratification lands in Jan/Feb 2026 as expected, this 26% move is just the warm-up.

Source: Trading View, 22 December 2025, 11:10 AM GMT

Please wait processing your request...

Please wait processing your request...