The London Stock Exchange opened its 2026 doors with a decisive statement from one of its most resilient performers. On January 2, 2026, Babcock International Group (LSE: BAB) saw its shares climb by approximately 2.4%, continuing a multi-year momentum that has transformed the company from a turnaround story into a premier FTSE 100 industrial powerhouse.

While the broader market remains sensitive to global economic shifts, Babcock is carving out a niche as a "safe haven" growth play. This article breaks down the mechanics behind the New Year surge and analyzing the fundamentals driving this defense titan.

The Jan 2 Catalyst: Why the Price Jumped

Source: Kalkine Group

The ~2.4% uptick on the first full trading day of 2026 wasn't a fluke; it was the result of a "perfect storm" of operational delivery and macro-tailwinds.

- Contract Momentum & Backlog Visibility: Entering 2026, Babcock boasts a massive contract backlog (exceeding £10 billion). This provides the "earnings visibility" that retail and institutional investors crave during periods of market volatility.

- The "AUKUS" and Nuclear Tailwind: As the UK ramps up its nuclear submarine and civil energy commitments, Babcock’s Nuclear sector—its highest-margin division—is seeing unprecedented demand.

- Share Buyback Execution: The ongoing execution of the £200 million share buyback programme announced in late 2025 continues to provide a structural floor for the share price, reducing share count and boosting Earnings Per Share (EPS).

Latest Business Model: From Service Provider to Tech Integrator

Babcock has moved away from being a simple "outsourcing" firm. Its 2026 business model is centered on high-value engineering and technology integration across four core sectors:

- Marine: Leading the Type 31 Frigate programme and providing critical support for the Royal Navy's fleet.

- Nuclear: Managing complex infrastructure at Devonport and Rosyth, and playing a pivotal role in the UK’s nuclear deterrent (submarines) and civil nuclear expansion.

- Aviation: Transitioning into high-growth international military training (e.g., the Mentor 2 contract in France).

- Land: Refocusing on military vehicle support (e.g., the £1bn DSG contract) while divesting lower-margin civil businesses like rail.

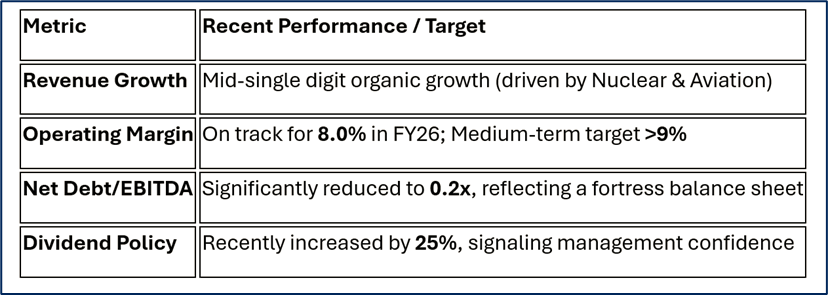

Financial & Operational Performance: By the Numbers

The most recent financial updates highlight a company that is finally hitting its "margin sweet spot."

Source: Company Data

Operational Milestone: The successful "float-off" of the first Type 31 frigate and the reopening of the 15 Dock facility at Devonport have demonstrated that Babcock can execute complex, large-scale engineering projects on time—a key differentiator from its peers.

SWOT Analysis (2026 Landscape)

Source: Kalkine Group

Strengths

- Critical Infrastructure Ownership: Ownership of the UK’s only licensed refitting docks for nuclear submarines creates a powerful moat.

- High Switching Costs: Defense contracts are typically 5–20 years in length, ensuring long-term revenue streams.

- De-risked Pension Scheme: Years of deficit repair have finally neutralized a former "black hole" on the balance sheet.

Weaknesses

- Concentration Risk: A significant portion of revenue is tied to the UK Ministry of Defence (MOD).

- Labor Scarcity: High demand for nuclear engineers and specialized technicians creates wage pressure and recruitment hurdles.

Opportunities

- Global Expansion: Growing footprints in Poland, Australia, and France reduce reliance on the UK budget.

- AUKUS Pillar 1: Long-term opportunities to support Australia’s new nuclear submarine capability.

- AI & Digital Twins: Using AI for "predictive maintenance" on naval fleets to increase margins.

Threats

- Government Fiscal Pressures: While defense spending is rising, overall UK "fiscal "tightness" could lead to delayed contract awards.

- Supply Chain Inflation: Volatility in specialized material costs (steel, electronic components) can eat into fixed-price contract margins.

The Risk Factors to Watch

No investment is without friction. Investors should monitor:

- Execution Risk: Large-scale naval builds (Type 31) have thin margins for error; any significant delay could trigger "onerous contract" provisions.

- Geopolitical Shifts: While current tensions drive defense spending, any de-escalation or shift in NATO priorities could cool the sector's "heat."

- Refinancing: While debt is low, the interest rate environment in 2026 will dictate the cost of future bond issuances.

Conclusion

Babcock International’s 2026 start reflects a company that has successfully shed its "troubled" past. By focusing on high-margin nuclear work and international defense exports, it has aligned itself with the most urgent priorities of Western governments. The 2.4% gain on January 2 is a signal that the market views Babcock not just as a defense contractor, but as a critical national asset with a strengthening financial engine.

Please wait processing your request...

Please wait processing your request...