The final trading session of 2025 was a subdued affair for the FTSE 100, yet BP PLC (LSE: BP.) managed to punch through the holiday quiet, closing up ~1% on December 31. While the broader market hovered near record highs, BP’s outperformance caught the eye of retail and institutional investors alike.

This rally wasn't just a "Santa Claus" bump; it was the culmination of a massive strategic pivot and a multi-billion dollar divestment deal that redefined the company's balance sheet in the final days of the year.

Key Reasons & Drivers for the Dec 31 Surge

Source: Kalkine Group

Several specific catalysts converged to push BP’s share price higher on the final day of 2025:

- The Castrol Liquidity Injection: Just days prior, BP confirmed the sale of a 65% majority stake in Castrol to Stonepeak for $10 billion. Investors spent the final session of the year pricing in the massive cash inflow, which significantly bolsters BP’s "buyback ammunition" for 2026.

- Production Milestone: On December 11, BP announced it had brought its seventh major project of the year into production. This reinforced the market’s confidence in BP’s ability to hit its goal of increasing fossil fuel output to 2.5 million barrels per day by 2030.

- The "Gap Closing" Trade: Throughout 2025, BP trailed its rival Shell. Year-end portfolio rebalancing saw "value hunters" moving into BP, betting that the company’s recent strategic reset—shifting focus back to high-margin oil and gas—would narrow the valuation gap with its peers.

Latest Business Model: "Integrated, Not Just Green"

BP’s 2025 business model is a "pragmatic evolution" from its 2020 "Beyond Petroleum" stance. CEO Murray Auchincloss has steered the ship toward a three-pillar strategy:

- High-Value Upstream: Growing oil and gas production (specifically in the Gulf of Mexico and Brazil) to fund the transition.

- Disciplined Transition: Selective investments in biogas, biofuels, and EV charging, but only where returns are immediate and high.

- Capital-Light Renewables: Moving away from expensive offshore wind ownership (evidenced by the sale of US wind assets in late 2025) toward "partnership models" that reduce BP's capital exposure.

Latest Financial & Operational Updates

- Cash Flow & Shareholder Returns: BP returned over $10 billion to shareholders in 2025 through a combination of dividends and aggressive share buybacks.

- Operational Excellence: The refining segment reported a 93% utilization rate in late 2025, a testament to high plant reliability and technological upgrades.

- Cost Cutting: The company is on track to hit $2 billion in annual structural cost savings by the end of 2026, streamlining its global workforce by approximately 6,000 roles.

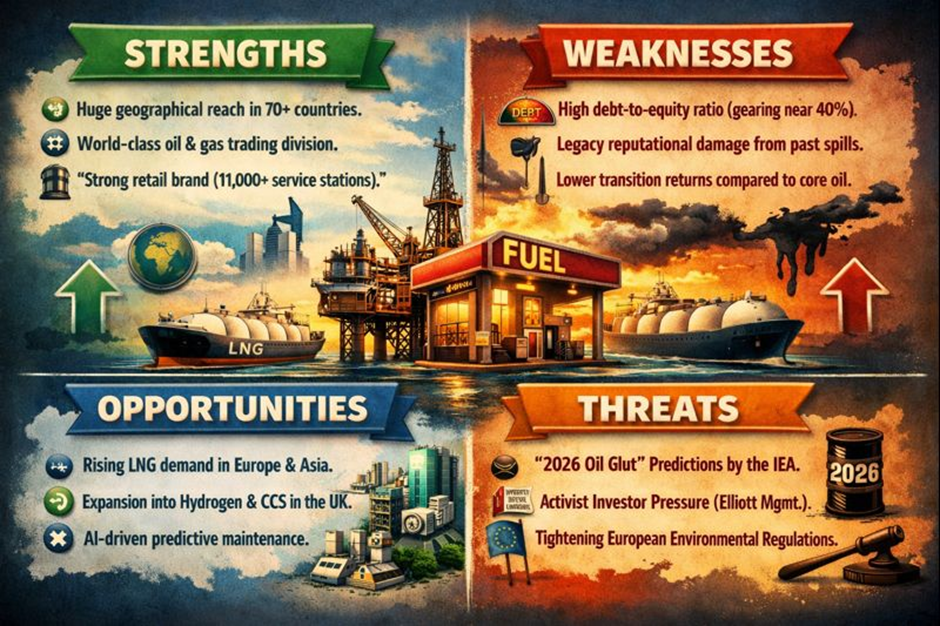

BP SWOT Analysis (2026 Outlook)

Source: Kalkine Group

Key Risks to Watch in 2026

Despite the year-end rally, BP faces a gauntlet of risks:

- Commodity Volatility: A potential supply surplus in 2026 could see Brent crude dip toward $60–$65/bbl, testing BP’s break-even levels.

- Asset Dilution: While the Castrol sale provided cash, analysts warn that selling high-margin "cash cow" assets could dilute the quality of remaining cash flows long-term.

- Political Risk: The Great British Energy Act 2025 and potential windfall tax extensions in the UK remain a constant headwind for North Sea operations.

Conclusion

BP ended 2025 on a high note, not because it solved all its problems, but because it chose a side. By pivoting back toward its "advantaged" oil and gas roots and offloading non-core assets like Castrol and US wind, the company has simplified its narrative for 2026. Investors are rewarding the clarity, even if the road ahead remains paved with geopolitical and environmental uncertainty.

Please wait processing your request...

Please wait processing your request...