The London Stock Exchange might have been winding down for the holidays, but CAB Payments Holdings (LSE: CABP) shareholders received an early gift this December 24, 2025. The stock climbed ~3%, defying the usual low-volume holiday lull. After a "reset" year in 2024 and a transformative 2025, investors are finally asking: has the fintech underdog found its floor?

The Christmas Eve Spark: Why the 3% Pop?

The modest but significant rally on December 24 wasn't just holiday cheer; it was a culmination of several late-Q4 drivers:

Source: Kalkine Group

- ADGM Approval Momentum: Following the October announcement of "in principle" approval from the Abu Dhabi Global Market (ADGM), market confidence in CABP’s Middle East expansion has solidified.

- Operational Leaner-ness: Investors are pricing in the full impact of the 20% headcount reduction executed earlier in 2025, which saved an estimated £12 million in staff costs.

- The "Visa Effect": Continued integration with Visa Direct is opening up 8.5 billion end-points, shifting CABP from a niche wholesale player to a high-volume retail infrastructure provider.

- Oversold Recovery: Trading at a significant discount to its IPO price, the stock saw "window dressing" as institutional buyers re-entered positions before the 2026 fiscal year.

Latest Business Model: Beyond Just FX

CAB Payments has aggressively moved away from its risky dependence on a few "currency corridors" (like the Nigerian Naira). The 2025 business model is built on three pillars:

- B2B2X Infrastructure: Not just moving money, but providing the "pipes" for other banks and fintechs to reach hard-to-access markets.

- Banking-as-a-Service (BaaS): Leveraging its full UK banking license to offer trade finance and regulated deposit-taking, which provides more stable "annuity-like" income compared to volatile FX spreads.

- Low-Capital Scaling: The first successful trade asset sale in early 2025 proved the company can scale its trade finance business without bloating its balance sheet.

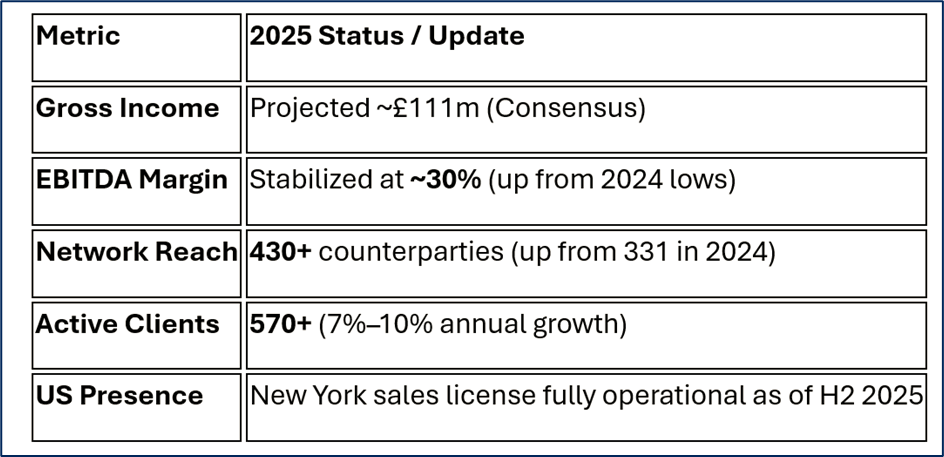

Financial & Operational Pulse Check

Source: Company Data

SWOT Analysis: The Hard Truths

Source: Kalkine Group

Strengths

- Regulated Moat: Holding a UK banking license is a massive barrier to entry for pure-tech competitors.

- Niche Dominance: Unrivaled access to "frontier" markets where Tier-1 banks are de-risking and exiting.

- B-Corp Status: A "partner of choice" for international aid organizations (NGOs) which require high ESG compliance.

Weaknesses

- Legacy Sentiment: Still haunted by the post-IPO "profit warning" of 2023; retail investor trust remains fragile.

- Fixed Cost Base: Despite layoffs, the business requires significant tech spend to maintain security and compliance.

Opportunities

- Digital Currencies: Expansion into Stablecoin and CBDC settlement to reduce transaction times in Africa and Asia.

- US Market: The NY office allows direct solicitation of US-based NGOs and Tier-2 banks.

Threats

- FX Compression: As emerging markets stabilize, the high "take rates" (margins) CABP enjoys may naturally shrink.

- Geopolitics: Sudden coups or economic collapses in core African markets can instantly freeze revenue in specific corridors.

Key Risks to Watch in 2026

- USD Strength: A persistently strong dollar can dampen demand for cross-border flows into emerging markets.

- Execution Risk: The transition to a "product-led" growth model requires the new leadership team to maintain 2024's momentum without further internal restructuring.

- Regulatory Scrutiny: As they expand into Abu Dhabi and the US, the compliance burden grows exponentially.

Conclusion

The 3% lift on December 24, 2025, suggests that the market is beginning to value CAB Payments for what it is now—a leaner, more diversified fintech bank—rather than what it was during its rocky IPO. With a stabilized 30% EBITDA margin and a massive new pipeline via Visa, the "reset" appears to be over. However, 2026 will be the true test: can they turn these operational milestones into double-digit revenue growth?

Please wait processing your request...

Please wait processing your request...