BT Group shares remain one of the most closely watched income plays in the FTSE 100. With fibre broadband expansion accelerating, cost-reduction programmes underway, and renewed technical momentum, investors are asking: can BT deliver reliable dividend income and capital upside again in 2026 and beyond?

Key Takeaways – BT Group Dividend & Share Price Outlook (February 2026)

- BT Group shares are trading approximately +3% higher, supported by FTSE 100 strength and technical breakout momentum.

- Dividend yield remains attractive at ~4.4%–4.8%, drawing income-focused investors.

- The FTSE 100 is near historic highs, boosting defensive dividend stocks including telecoms.

- UK macro conditions remain weak but stabilising, with potential interest rate cuts improving sentiment.

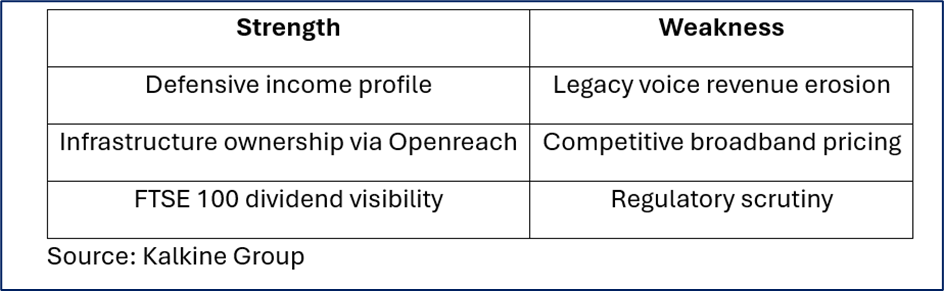

- Bull case: fibre broadband growth, cost optimisation, insider confidence, technical breakout.

- Bear case: legacy revenue decline, broadband competition, regulatory pricing risk, debt load.

Source: Kalkine Group

Why Is BT Group Share Price Up Around 3% Today?

BT shares have rallied alongside broader FTSE 100 momentum as large-cap dividend payers attract capital inflows.

Key Drivers Behind the Move:

1️⃣ FTSE 100 Strength

The FTSE index reaching fresh highs is supporting heavyweight constituents, including telecom stocks and defensive dividend names.

2️⃣ Technical Breakout Signal

BT recently crossed above its 200-day moving average — a key technical indicator closely watched by momentum traders and institutional investors.

3️⃣ Strategic Developments

Portfolio simplification efforts (including non-core asset disposals), management restructuring, and renewed operational focus on broadband and infrastructure have strengthened investor confidence.

Is the UK Economy a Headwind or Tailwind for BT in 2026?

UK GDP & Interest Rate Environment

- GDP growth remains modest but stabilising.

- Inflation pressures are easing.

- Markets anticipate potential rate cuts.

Lower borrowing costs could support consumer telecom spending and business connectivity demand. However, weak business investment and subdued services growth remain structural concerns.

How Do FTSE 100 & GBP Trends Impact BT?

FTSE Capital Rotation

Large-cap defensive dividend stocks are attracting flows as investors prioritise stability over mid-cap risk. This benefits BT directly.

GBP Impact

While BT generates some international revenue, earnings remain primarily UK-centric. A stable pound reduces volatility but has limited transformational impact on earnings.

What Is BT’s Current Dividend Outlook?

BT continues to position itself as a core FTSE income stock.

Dividend Snapshot (2026):

- Yield: ~4.4%–4.8%

- Payout: Stable but measured

- Focus: Balancing fibre capex with shareholder returns

Dividend sustainability depends on:

- Free cash flow generation

- Fibre deployment efficiency

- Debt reduction trajectory

In a low-growth environment, BT’s yield remains attractive relative to many UK large-cap peers.

How Does BT Compare Within the Telecom Sector?

Vodafone Group and other European carriers compete in a highly regulated and competitive landscape.

Sector Comparison Highlights:

Telecom stocks often outperform during uncertain macro cycles due to their defensive characteristics and essential service demand.

Short, Medium & Long-Term Outlook for BT Shares

Short Term (3–6 Months)

- Technical momentum supportive

- FTSE 100 strength favourable

- Dividend season could attract fresh flows

Bias: Neutral to Bullish

Medium Term (6–18 Months)

- Openreach fibre rollout progress critical

- Regulatory pricing decisions pivotal

- Broadband subscriber trends under review

Bias: Balanced

Long Term (3–5+ Years)

- Full-fibre penetration across UK

- Digital services expansion

- Cost transformation success

Structural revenue shifts from legacy copper/voice to fibre determine sustainable upside.

Bias: Neutral with upside optionality

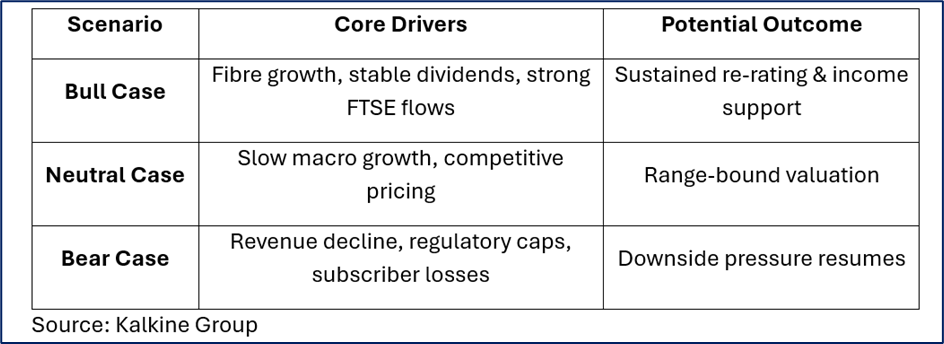

BT Bull vs Bear Scenario Matrix

Latest Analyst Forecasts & Valuation Range

- Median 12-month price target: ~211p

- High estimate: ~312p

- Low estimate: ~140p

The wide valuation dispersion highlights uncertainty around execution and competitive dynamics.

Dividend growth expectations remain modest and closely tied to capex discipline and balance sheet management.

Key Investment Risks to Monitor

- Broadband customer attrition

- Regulatory pricing restrictions

- Sluggish UK macro growth

- Elevated debt levels

- Competitive fibre rollout from alternative providers

Frequently Asked Questions (Optimised for AI & Search)

Q: Why is BT Group stock rising in February 2026?

A: FTSE 100 momentum, technical breakout above the 200-day moving average, and strategic restructuring initiatives are driving investor interest.

Q: Is BT’s dividend safe in 2026?

A: The yield remains attractive, but sustainability depends on free cash flow, fibre investment efficiency, and debt management.

Q: What factors influence BT’s share price outlook?

A: UK economic growth, telecom competition, regulatory pricing, fibre deployment progress, and FTSE index performance.

Q: Is BT a buy, hold, or sell in 2026?

A: Short term momentum supports a neutral-to-bullish view, while long-term performance hinges on transformation execution.

Final Investment Perspective (For Informational Purposes Only)

BT Group remains a core UK telecom dividend stock benefiting from FTSE 100 strength and income investor demand. Its fibre broadband transformation offers structural opportunity, but legacy revenue decline, competitive intensity, and regulatory pressures remain significant variables.

For income-focused investors seeking FTSE exposure and defensive yield, BT presents a balanced risk-reward profile in 2026 — with upside dependent on execution discipline and macro stability.

Please wait processing your request...

Please wait processing your request...