International Consolidated Airlines Group (IAG) has been one of the clearest beneficiaries of the post-pandemic travel rebound. But with shares now trading near multi-year highs, investors are asking a critical question in February 2026:

Is the airline recovery already priced in—or does IAG still offer meaningful upside?

What’s Driving IAG Stock Higher After Its 4.3% Jump on 6 February 2026?

Latest Performance Snapshot (February 2026)

- Share price move: IAG surged +4.33% on Friday, 6 February 2026, closing near 438.50 GBX

- Market comparison: Strongly outperformed the FTSE 100, which gained only ~0.59%

- Momentum signal: Shares are trading close to their 52-week high, reinforcing bullish technical sentiment

- Volume confirmation: Healthy daily trading volumes of ~13.9 million shares suggest broad investor participation rather than speculative spikes

Interpretation: The rally reflects renewed confidence that airline earnings momentum can extend into 2026, supported by demand strength rather than short-term news flow alone.

What Are the Key Takeaways for IAG Investors Right Now?

- IAG continues to outperform the FTSE 100, supported by improving sector fundamentals

- Dividend payments have resumed, with yields still modest but trending higher year-on-year

- Analyst sentiment remains bullish, with most brokers maintaining Buy or Outperform ratings

- Post-COVID travel recovery, particularly in premium and long-haul routes, remains the core earnings driver

- Macro risks—including currency strength, fuel prices, and global growth uncertainty—remain key variables

How Are Global Travel Trends and the UK Economy Shaping IAG’s Share Price?

Global Airline Demand Dynamics

Worldwide air travel continues to normalize, with transatlantic and premium cabin demand emerging as standout profit contributors.

Key global tailwinds include:

- Sustained rebound in international leisure travel

- Gradual return of business and premium corporate travel

- Capacity discipline across airlines supporting ticket pricing

- Industry consolidation reducing destructive competition

For IAG, strong exposure to North America–Europe routes has translated into pricing power and margin resilience.

UK Economy and FTSE Linkages

As a major FTSE 100 constituent, IAG remains sensitive to broader UK macro trends, including:

- GBP/USD and GBP/EUR currency movements

- UK GDP growth expectations

- Fuel and operating cost inflation

- Consumer confidence and discretionary spending patterns

While the FTSE 100 has led broader UK equity performance, a risk-on environment could further benefit cyclical names like IAG.

What Does the Sector and Company Analysis Reveal About IAG?

Airline Sector Backdrop

- Airlines remain high fixed-cost businesses, sensitive to fuel prices and demand volatility

- Load factors have improved significantly versus pre-pandemic levels

- Premium travel continues to deliver outsized margin contribution

- Competitive pressure from European and US carriers persists, but pricing discipline has improved

IAG’s Strategic Advantages

IAG’s diversified structure strengthens its resilience:

- Portfolio brands including British Airways, Iberia, Vueling, and Aer Lingus

- Strong transatlantic market positioning

- Growing ancillary and loyalty-program revenues

- Ongoing fleet modernization, improving fuel efficiency and cost control

These factors help IAG smooth earnings across cycles compared with single-brand peers.

What Is the Latest Dividend Outlook for IAG Shareholders?

- Dividends have restarted following the pandemic suspension

- Current yields remain low-to-moderate, reflecting capital-intensive industry dynamics

- Payout ratios suggest gradual increases are possible, assuming earnings stability

- Dividends are supportive—but capital appreciation remains the primary return driver

What Are Analysts Forecasting for IAG in 2026?

- Consensus rating: Predominantly Buy / Outperform

- 12-month price targets: Indicate moderate upside from current levels

- Forecast dispersion: Wide, reflecting volatility in fuel costs, currency effects, and demand assumptions

Bottom line: Analysts broadly agree on direction, but not magnitude—typical for cyclical airline stocks.

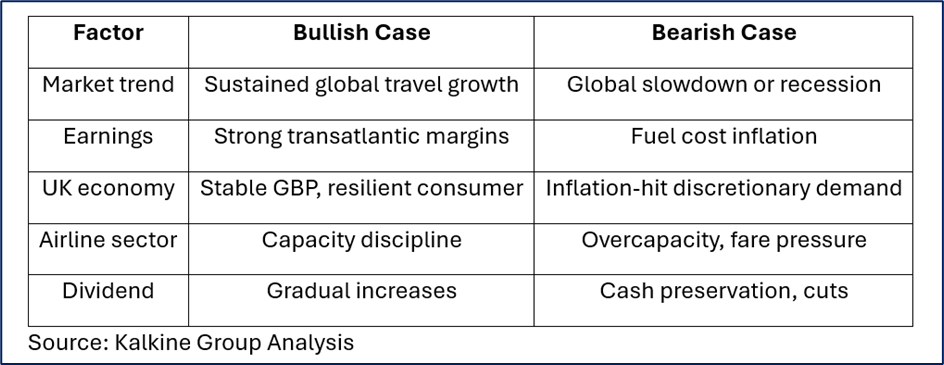

Bull vs Bear Scenario Matrix for IAG Stock

What Is the Short-, Medium-, and Long-Term Outlook for IAG?

Short Term (3–6 Months)

- Expect earnings-driven volatility

- Catalysts include quarterly results and Bank of England policy signals

Medium Term (6–12 Months)

- Further normalization of airline earnings

- Corporate travel recovery could support valuation

- Execution on cost control remains critical

Long Term (Beyond 12 Months)

- Structural growth in global air travel

- Loyalty program monetization and fleet efficiency gains

- Returns will depend on macro resilience and capital discipline

Is IAG Stock Bullish, Bearish, or Neutral Right Now?

Retail-Investor View:

- Bullish: Demand recovery, premium pricing power, improving balance-sheet strength

- Neutral: Currency volatility, inflation, geopolitical uncertainty

- Bearish: High sensitivity to fuel prices and global economic shocks

Overall stance: Neutral-to-bullish, with strong fundamentals but elevated cyclical risk.

Frequently Asked Questions (SEO-Optimized)

Should IAG stock be bought or held in 2026?

Analyst consensus leans Buy, but position sizing should reflect airline volatility.

Does IAG pay a dividend now?

Yes. Dividends have resumed, with gradual growth expected rather than high yields.

How does FTSE 100 performance impact IAG?

IAG is closely linked to UK macro data and GBP movements as a major FTSE 100 constituent.

Is airline demand sustainable post-COVID?

Demand remains robust, especially in premium routes, though margins fluctuate with costs.

Final Investment Verdict: Is IAG Worth Considering in 2026?

IAG stands out as a well-positioned global airline group benefiting from sustained travel recovery, strong transatlantic exposure, and improving shareholder returns. While valuation is no longer distressed, the company still offers selective upside for investors comfortable with cyclical risk.

Best suited for: Diversified portfolios seeking recovery-linked growth—not low-volatility income.

Please wait processing your request...

Please wait processing your request...