Key Takeaways – February 2026 Update

- Morgan Sindall shares jumped approximately 6% on 12 February 2026, outperforming the FTSE 250 Index and broader UK equities

- Record order book strength supports strong revenue visibility into 2026–2027

- UK infrastructure, housing regeneration, and defence spending continue driving sector momentum

- Progressive dividend outlook backed by robust free cash flow and disciplined capital allocation

- Short-term technical momentum is bullish; long-term upside depends on execution and UK infrastructure cycle durability

Source: Kalkine Group

Why Did Morgan Sindall Shares Surge 6% in February 2026?

Morgan Sindall stock rallied sharply on 12 February 2026, outperforming both the FTSE 250 Index and the FTSE 100 Index, signalling renewed investor appetite for high-quality UK infrastructure plays.

Key catalysts behind the rally:

- Sustained growth in secured order book across Construction & Infrastructure

- Improved visibility from UK government capital expenditure commitments

- Stable operating margins despite prior cost inflation pressures

- Strengthening GBP and moderating inflation

- Institutional rotation into cash-generative UK mid-cap dividend stocks

In a macro environment marked by stabilising bond yields and improving UK growth sentiment, Morgan Sindall is increasingly viewed as a defensive growth contractor with earnings resilience.

Is the UK Economic Backdrop Favourable for Construction Stocks in 2026?

Is UK Inflation and Interest Rate Normalisation Supporting the Sector?

The UK macro environment in early 2026 shows meaningful improvement:

- Inflation has cooled significantly from 2023–2024 peaks

- Interest rates are gradually normalising

- Public infrastructure funding remains intact

- Housing activity is stabilising

For contractors like Morgan Sindall, this combination reduces cost volatility while preserving project pipeline strength.

How Does Morgan Sindall’s Business Model Drive Competitive Advantage?

Morgan Sindall operates across five diversified divisions:

- Construction

- Infrastructure

- Fit Out

- Property Services

- Partnership Housing

Unlike high-risk developers, Morgan Sindall maintains a disciplined, framework-driven contracting strategy focused heavily on public and regulated sectors.

Core strengths include:

- Long-term public sector frameworks

- Repeat institutional clients

- Conservative contract bidding discipline

- Strong balance sheet and limited leverage

- Consistent free cash flow generation

This diversified structure reduces exposure to speculative commercial cycles and supports margin stability across economic downturns.

How Does Morgan Sindall Compare With UK Construction Peers?

Within the UK infrastructure and contracting space, key competitors include:

- Kier Group

- Balfour Beatty

- Costain Group

Relative positioning advantages:

- Stronger balance sheet discipline

- Lower leverage profile

- Reduced exposure to risky fixed-price mega contracts

- Historically more consistent profitability

Morgan Sindall’s conservative execution approach enhances resilience compared with more cyclical or leveraged peers.

Can Morgan Sindall Sustain Dividend Growth in 2026 and Beyond?

Morgan Sindall maintains a progressive dividend policy aligned with earnings growth and free cash flow generation.

Dividend sustainability drivers:

- Strong operating cash conversion

- Limited net debt

- Infrastructure-backed revenue visibility

- Prudent capital allocation

If order book momentum continues translating into earnings growth, dividend increases remain achievable over the medium term.

For income-focused investors seeking UK dividend growth exposure, Morgan Sindall offers a compelling infrastructure-backed yield opportunity.

What Is the Technical and Fundamental Outlook for Morgan Sindall Stock?

Short-Term Outlook (3–6 Months): Is Momentum Building?

Bullish signals include:

- 6% breakout move

- Renewed buying interest in FTSE 250 mid-caps

- Infrastructure contract visibility

- Positive earnings sentiment

Risks: macro volatility, policy surprises, or contract margin slippage.

Medium-Term Outlook (1–3 Years): Can Earnings Compound?

Constructively bullish if:

- UK public infrastructure spending remains funded

- Operating margins remain disciplined

- Housing partnerships recover alongside macro stabilisation

Long-Term Outlook (3–5+ Years): Is This a Structural Infrastructure Play?

Neutral-to-bullish depending on:

- Execution discipline

- Inflation control

- Labour cost management

- Infrastructure funding continuity

Construction is cyclical, but best-in-class operators tend to outperform through disciplined bidding and balance sheet strength.

What Are Analysts Forecasting for Morgan Sindall in 2026?

Broker consensus (February 2026):

- Predominantly Buy/Overweight ratings

- Target prices imply mid-teens percentage upside from pre-rally levels

- Forward P/E valuation remains reasonable versus historical averages

Major UK broker coverage includes:

- Investec (Buy)

- Peel Hunt (Add)

- Numis (Buy)

- Shore Capital (Positive stance)

Consensus suggests confidence in earnings delivery and cash return continuity.

What Are the Biggest Risks Facing Morgan Sindall in 2026?

Investors should monitor:

- UK economic slowdown risk

- Government infrastructure budget adjustments

- Fixed-price contract margin compression

- Labour shortages and wage inflation

- Supply chain disruptions

While fundamentals remain strong, construction remains operationally sensitive to cost discipline.

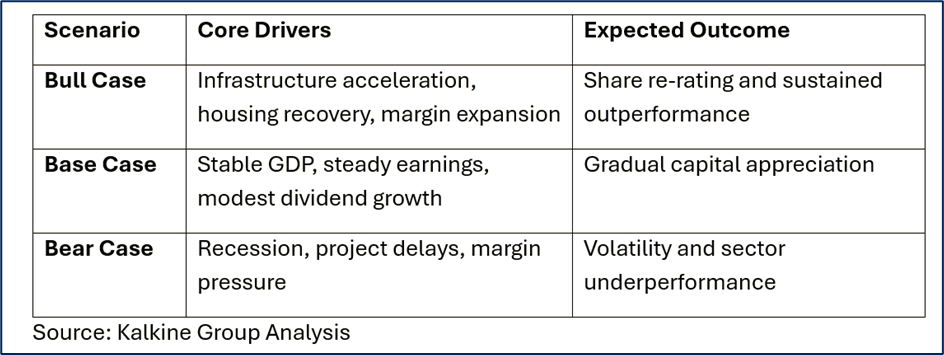

What Does the Bull vs Bear Case Scenario Analysis Suggest?

What Investment Strategies Make Sense for Morgan Sindall in 2026?

Short-Term Strategy

- Buy pullbacks within bullish momentum

- Track contract announcements

- Monitor UK macro indicators

Medium-Term Strategy

- Accumulate on market weakness

- Focus on dividend compounding

- Review order book quality regularly

Long-Term Strategy

- Hold for infrastructure cycle exposure

- Reinvest dividends

- Monitor balance sheet and capital discipline

Is Morgan Sindall a Top FTSE 250 Infrastructure Stock to Buy in 2026?

Morgan Sindall’s 6% surge in February 2026 reflects renewed confidence in UK infrastructure demand, earnings visibility, and disciplined contract management.

In a stabilising UK macro environment with ongoing public investment commitments, the company stands out as a high-quality, cash-generative, mid-cap infrastructure stock.

- Short term: Momentum favours bulls

- Medium term: Infrastructure pipeline supports earnings growth

- Long term: Execution discipline determines compounding potential

For investors seeking UK dividend growth, infrastructure exposure, and FTSE 250 upside, Morgan Sindall remains a structurally strong yet cyclically aware opportunity positioned for continued gains in 2026 and beyond.

Please wait processing your request...

Please wait processing your request...