Capricorn Energy (LSE: CNE) shares surged roughly 4% on December 30, 2025, closing the year on a high note despite a turbulent broader market. This late-year rally has caught the eye of retail investors and analysts alike, as the company pivots from its legacy "Cairn Energy" identity into a lean, Egypt-focused production engine.

Key Drivers: Why the 4% Spike Today?

The jump to approximately GBX 190 isn't just a random fluctuation. Several factors converged this week to boost sentiment:

Source: Kalkine Group

- Waldorf Payment Resolution: Market confidence was bolstered by the latest updates regarding the Waldorf earn-out. After months of uncertainty, the company’s December 12th update and subsequent end-of-year settlement talks suggest that while the full amount is unlikely, a significant portion of the capital is being recovered, strengthening the balance sheet for 2026.

- Egypt Concession Synergy: Investor enthusiasm is building around the ratification of the merged concession agreements in Egypt. By consolidating eight existing agreements into a single integrated framework with partner Cheiron, Capricorn is significantly lowering its unit operating costs and unlocking new drilling targets.

- Oil Price Resilience: As Brent Crude remains stable, Capricorn’s low-cost production profile ($5–$7/boe) makes it an attractive "cash-cow" play for those looking for energy exposure without the massive overhead of "Supermajors."

- Short-Covering & Window Dressing: As the final full trading day of 2025, institutional rebalancing and the closing of short positions likely provided the technical tailwind needed to push the stock past key resistance levels.

Latest Business Model: The "Lean & Mean" Pivot

Capricorn has undergone a radical transformation. No longer an explorer chasing "frontier" wells in the Atlantic, its 2025 business model is built on high-margin, short-cycle production.

- Core Focus: Onshore Egypt (Western Desert).

- Revenue Streams: Direct oil and gas sales via the Egyptian General Petroleum Corporation (EGPC).

- Capital Allocation: A strict "Pay-for-Performance" model. The company only commits significant D&P (Development & Production) Capex when cash receipts from the Egyptian government are regular, protecting shareholder equity.

- Secondary Value: Harvesting contingent payments from past disposals (Senegal and UK North Sea assets) to fund special dividends or buybacks.

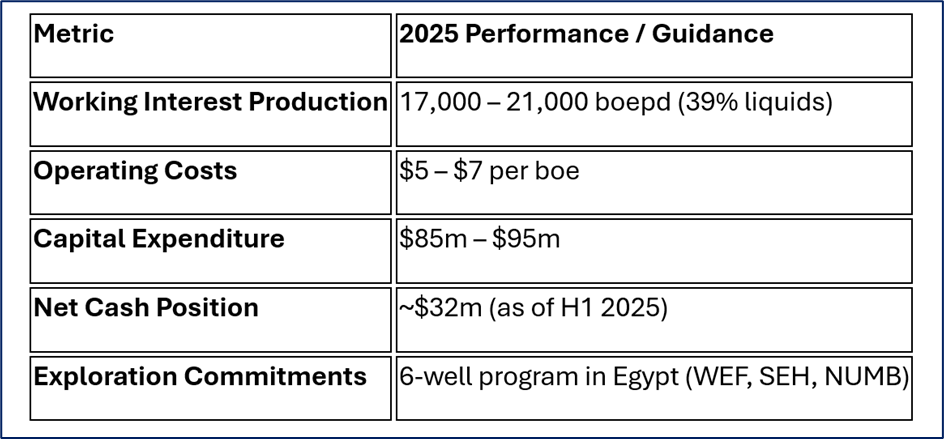

2025 Financial & Operational Snapshot

Source: Company Data

The company successfully received a $50m Senegal contingent payment from Woodside in early 2025, which acted as a massive liquidity cushion during the year's volatility.

SWOT Analysis

Source: Kalkine Group

Strengths

- Low-Cost Operator: One of the cheapest production profiles in the FTSE All-Share energy sector.

- Agile Balance Sheet: Low debt and a history of returning "excess" cash to shareholders.

- Strategic Partnerships: Strong operational alignment with Cheiron in Egypt.

Weaknesses

- Geographic Concentration: Over-reliance on Egypt’s fiscal environment.

- Receivables Risk: Historically, Egypt has struggled with timely payments to international oil companies (IOCs).

- Small-Cap Volatility: With a market cap hovering around £125m–$130m, the stock is prone to sharp swings on low volume.

Opportunities

- M&A Activity: Management is actively screening for "advantaged" assets in the UK North Sea and MENA region.

- Exploration Upside: Success in the South East Horus or West El Fayoum wells could add significant reserve life.

- Energy Transition: Their 15% carbon reduction target for 2025 puts them ahead of many small-cap peers in ESG rankings.

Threats

- Political Instability: Regional tensions in the Middle East can impact investor sentiment regardless of operational success.

- Currency Fluctuations: Exposure to the Egyptian Pound and USD/GBP shifts.

- Commodity Price Slumps: A sudden drop in Brent Crude below $60/bbl would squeeze the margins of their development wells.

The "Reality Check" Risks

Investing in Capricorn isn't without its "red flags." The Egyptian receivables position remains the elephant in the room. While the balance has flattened, any delay in payments from EGPC directly impacts Capricorn's ability to fund its 2026 drilling program. Furthermore, the Waldorf Waldorf earn-out remains a point of contention; investors should be wary of any further write-downs if the remaining $22.5m isn't recovered.

Conclusion

Capricorn Energy’s 4% pop on December 30th reflects a market that is finally beginning to price in the stability of its new Egyptian engine. The company enters 2026 as a leaner, more disciplined version of its former self. If the integrated concession agreements deliver the promised synergies and the drill bit finds success in the Western Desert, today's rally might just be the baseline for a much larger recovery.

Please wait processing your request...

Please wait processing your request...