Close Brothers Group (LSE: CBG) saw its shares rally by approximately 4.3% on December 23, 2025, capping off a volatile but resilient year for the FTSE 250 merchant bank. As the market heads into the Christmas break, investors are reappraising the "old school" lender’s survival and recovery strategy after a year dominated by regulatory headwinds.

- Key Reasons & Drivers for the Dec 23rd Surge

The 4% jump wasn't a random holiday fluke; it was driven by a confluence of regulatory clarity and strategic execution:

Source: Kalkine Group

- FCA Deadline Passing: Investors reacted positively to the passing of the December 12th FCA consultation deadline. With the "worst-case" scenarios now baked into the current £300 million provision, the market is pricing in a "known unknown" rather than a catastrophic surprise.

- Completion of Asset Sales: Following the successful disposal of Close Brothers Asset Management (CBAM) and Winterflood Securities earlier in the year, the market is finally rewarding the bank’s simplified, high-capital structure.

- "Santa Rally" Yield Hunting: With the stock having been heavily discounted due to the motor finance saga, retail and institutional "value hunters" moved in, attracted by the bank's fortified 13.4% pro-forma CET1 ratio.

- Short Covering: High short interest throughout 2025 began to unwind as the probability of a "worst-case" industry-wide redress scheme appeared to stabilize following the Supreme Court’s nuanced views in late 2025.

- Latest Business Model: The "Back to Basics" Pivot

Close Brothers has spent 2025 shedding its non-core skin. The "New Close Brothers" is a leaner, more focused specialist lender:

- Exit from Non-Core: The group has completed the sale of Winterflood (Securities) and CBAM (Wealth Management), and is actively exiting its Vehicle Hire and Brewery Rentals businesses.

- Pure-Play Specialist Lending: The focus has returned to high-margin, secured lending for UK/Irish SMEs.

- Premium Finance Shifting: A strategic pivot away from personal lines (home/car insurance) toward Commercial Lines, where risk-adjusted returns are higher and operational complexity is lower.

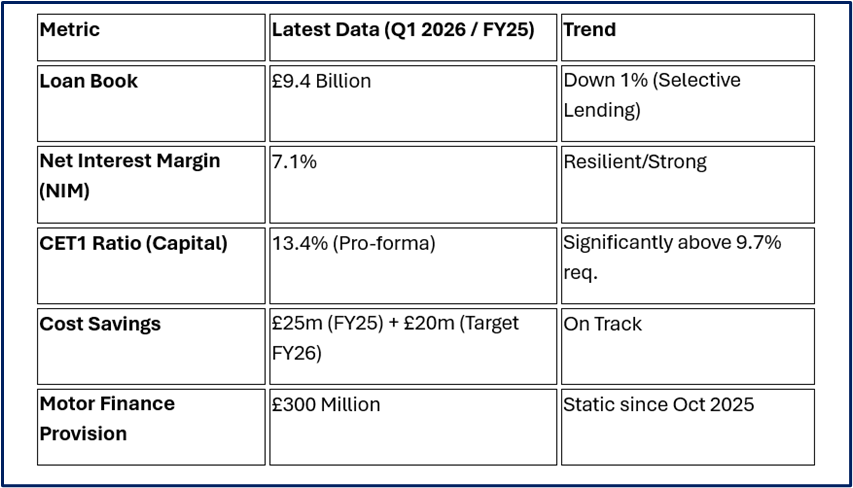

- Financial & Operational Updates (Q1 2026 Snapshot)

As of the latest updates leading into December 2025:

Source: Company Data

- SWOT Analysis: 2025 Year-End Edition

Source: Kalkine Group

Strengths

- Capital Fortress: Pro-forma CET1 of 13.4% provides a massive buffer against regulatory shocks.

- NIM Superiority: Maintaining a 7%+ margin is far above the "Big Four" retail banks.

- Deep SME Relationships: 99% of UK businesses are SMEs, a market Close Brothers understands better than most.

Weaknesses

- Dividend Suspension: Income investors remain sidelined until the FCA review concludes in early 2026.

- Concentration Risk: By selling Winterflood and CBAM, the bank is now entirely dependent on the lending cycle.

Opportunities

- Market Consolidation: As smaller competitors struggle with costs, Close Brothers can cherry-pick high-quality SME loans.

- Operational Efficiency: The target of £20m/year in savings through 2028 could significantly boost RoTE.

Threats

- FCA Final Rules (Feb/March 2026): The ultimate cost of the motor finance redress remains the "Sword of Damocles."

- Economic Stagnation: A downturn in the UK SME sector would lead to rising bad debts (currently stable at 1.0%).

5. Key Risks to Watch

- Redress Creep: While the £300m provision is the "best estimate," the final FCA methodology in early 2026 could still shift the goalposts.

- Loan Book Contraction: The bank has been shrinking its loan book to preserve capital; it must return to growth in 2026 to maintain earnings momentum.

- Regulatory Burden: The "Consumer Duty" era in the UK continues to put pressure on specialist lending fees and commissions.

Conclusion: A Christmas Relief Rally or a New Chapter?

The 4% rise on December 23rd reflects a market that is tired of being afraid. Close Brothers has successfully "de-risked" its balance sheet by selling assets and building a capital mountain. While the dividend remains on ice, the bank is now a "pure-play" specialist lender with a clear path back to double-digit RoTE by 2028.

Investors are betting that the darkest days of the motor finance scandal are in the rearview mirror, and that the bank's streamlined model is ready to sprint once the FCA gives the green light.

Source: Trading View, 23 December 2025

Please wait processing your request...

Please wait processing your request...