FTSE 250 Strategic Momentum - Currys and Premier Foods

The UK mid-cap landscape is witnessing a significant divergence as Currys PLC and Premier Foods emerge as standout performers, buoyed by robust holiday trading and a clear demonstration of pricing resilience.

As of January 21, 2026, both entities have recalibrated market expectations through aggressive operational efficiencies and a strategic pivot toward high-margin recurring revenue streams. While Currys leverages a dominant 75% market share in the nascent AI-enabled laptop segment, Premier Foods continues to harness the defensive strength of its iconic "Everyday" brands. This convergence of tech-driven growth and consumer staple reliability has positioned both firms at the forefront of the FTSE 250’s latest bullish cycle.

Currys PLC: The Tech-Retail Transformation

Source: Kalkine Group

The latest surge in Currys’ valuation is rooted in a fundamental shift toward services and subscription-based ecosystems. The company’s January 2026 update highlighted a significant profit forecast upgrade, driven by a 4% growth in like-for-like (LFL) revenue and a massive 144% increase in group adjusted profit before tax (Currys Interim Report).

- Key Drivers and Surge Reasons:

- The primary catalyst is the "Peak Trading" success, where sales of AI-capable laptops and premium mobile devices offset declines in traditional categories like televisions.

- A critical driver is the expansion of the iD Mobile subscriber base, which grew to 2.4 million, tracking well ahead of internal targets (Currys PLC RNS).

- Operational leverage in the Nordics has finally stabilized, turning a historical drag into a contributor to the bottom line through a 24% increase in adjusted EBIT.

- Current Business Model & Financials (company sourced)

- Currys operates an omnichannel model with an increasing focus on the "Circular Economy" through its massive Newark repair facility, which handles 1.6 million tech repairs annually.

- Latest financials show a net cash position of £133 million, a significant recovery that has enabled a 0.75p interim dividend and a £50 million share buyback program (Currys Investor Update).

- Services now account for 15% of revenue, offering higher margins than hardware sales alone.

- Technical Analysis (as of Jan 21, 2026):

- The stock is exhibiting strong bullish momentum, having broken through the 124.60p resistance level.

- Immediate support is established at 118.50p. Technical oscillators suggest a "Buy" signal on the daily timeframe as the price stays consistently above the 50-day moving average.

- Latest SWOT Analysis:

- Strengths: Market-leading 75% share in AI laptops; robust omnichannel integration; strongest balance sheet in a decade.

- Weaknesses: High operational costs due to a large physical store footprint; reliance on the UK market (85% of revenue).

- Opportunities: Expansion of the B2B division which grew 16% this period; growth in refurbished tech sales.

- Risks: Increases in colleague costs due to UK government budget measures; potential supply chain volatility in semi-conductors.

Premier Foods: Branded Resilience and Global Reach

Source: Kalkine Group

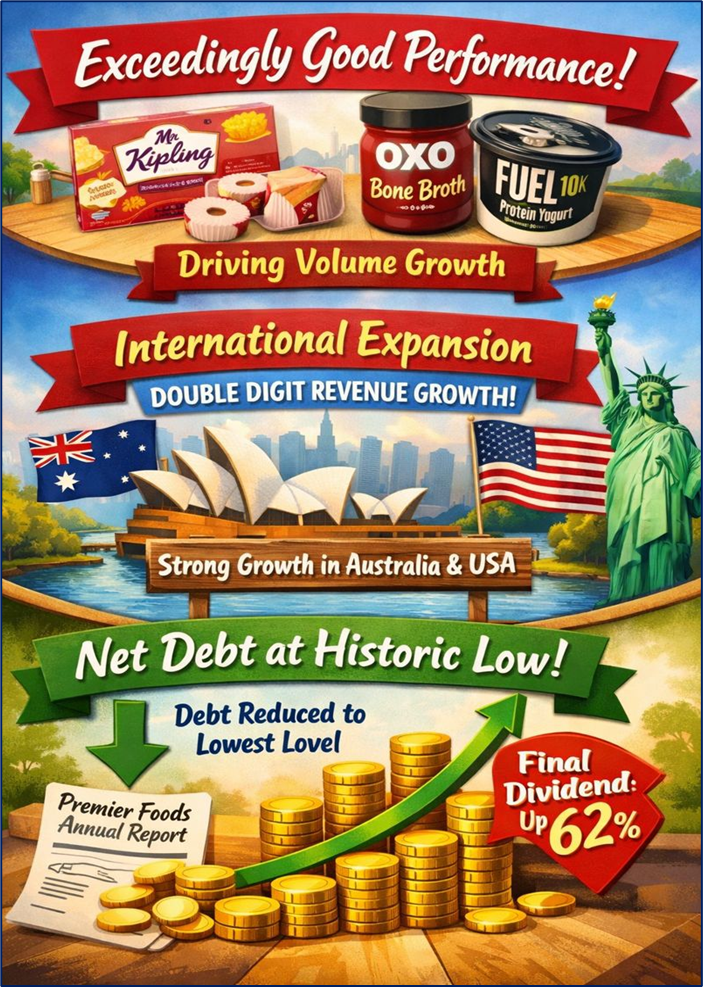

Premier Foods has redefined its market position as a "Branded Growth" powerhouse. On January 21, 2026, the company lifted its full-year profit outlook to the upper end of market expectations (£193m–£198.2m) following a 5.2% jump in branded revenue (Premier Foods Trading Update).

- Key Drivers and Surge Reasons:

- The "Exceedingly Good" performance of Mr Kipling and the successful launch of new categories like OXO Bone Broth and FUEL10K yogurt have driven volume growth.

- International expansion is a major tailwind, with double-digit revenue growth in Australia and the US.

- Net debt has reached its lowest historical level, allowing for a 62% increase in the final dividend in the previous cycle (Premier Foods Annual Report).

- Current Business Model & Financials (company sourced)

- The model relies on "The Branded Growth Model," prioritizing high-margin, household-name products over non-branded labels, which saw a 1.5% decline in the latest quarter.

- Vertical integration remains a core competency, with the company owning its mills and a fleet of 4,000 vehicles to mitigate commodity price volatility (Porter’s Five Forces Analysis).

- Total revenue for Q3 2025/26 reached £375.1 million, reflecting a 4.1% increase year-on-year.

- Technical Analysis (as of Jan 21, 2026):

- The stock surged 6.6% following the January 21 update.

- Immediate resistance is identified at 185.00p, with a pivot point at 178.00p. Long-term trends remain bullish, though short-term RSI suggests the stock is approaching overbought territory.

- Latest SWOT Analysis:

- Strengths: Dominant market share in core categories (28% in maize meal, high penetration in cakes); massive scale advantages in procurement.

- Weaknesses: Vulnerability to fluctuations in wheat and dairy prices; limited pricing power in the value-conscious discount segment.

- Opportunities: Continued leveraging of the Merchant Gourmet acquisition; expansion into "on-the-go" snacking formats.

- Risks: Regulatory headwinds regarding sugar taxes; rising energy and logistics costs impacting margins.

Compelling Conclusion

The current trajectory of Currys and Premier Foods underscores a pivotal moment for the FTSE 250, where operational discipline meets strategic innovation. Currys has successfully navigated the transition from a traditional electronics retailer to a tech-services leader, while Premier Foods has utilized its branded equity to outpace inflationary pressures. As we move further into 2026, the focus for both remains on sustaining these upgraded profit margins and navigating the delicate balance of consumer demand and rising operational costs. Their ability to deliver consistent cash flow and shareholder returns in a complex macro environment remains the primary narrative for institutional and retail observers alike.

Please wait processing your request...

Please wait processing your request...