The FTSE 100 has found a resilient star in Convatec Group (LSE: CTEC). On December 17, 2025, the stock climbed above 3%, outperforming the broader market and catching the eye of retail and institutional investors alike.

While the medical technology sector has faced its share of volatility this year, Convatec is proving that "boring is beautiful" when it comes to chronic care. Here is the deep dive into why the stock jumped, the inner workings of its business model, and the SWOT analysis every investor needs to see.

The December 17 Catalyst: Why the Jump?

The primary driver for yesterday's price action was a combination of institutional conviction and favorable macroeconomic tailwinds:

- Fidelity’s High-Conviction Bet: A major regulatory filing (TR-1) revealed that FIL Limited (Fidelity) increased its stake in Convatec, crossing the critical 5% threshold. In the world of the FTSE 100, when a titan like Fidelity increases its position, it sends a powerful signal to the market.

- Inflation "Cool-Off" Rally: The broader FTSE 100 rose 0.9% following softer-than-expected UK inflation data for November. This sparked hopes for more aggressive rate cuts by the Bank of England. As a company with some debt and significant international earnings, Convatec is a prime beneficiary of a weaker pound and lower interest rates.

- Short-Covering & Sector Rotation: Following the tragic passing of CEO Karim Bitar in October, the stock saw a period of uncertainty. Yesterday’s move suggests that investors are rotating back into "quality defensive" stocks that offer high visibility into 2026 earnings.

Source: Kalkine Group

The Business Model: The "Razor-and-Blade" of Healthcare

Convatec doesn't just sell products; it sells recurring necessity. Its business model is built on four pillars of chronic care, where patients require consumable supplies for the rest of their lives:

- Advanced Wound Care (30% of Rev): High-tech dressings for chronic wounds like diabetic ulcers.

- Ostomy Care (25% of Rev): Essential bags and seals for stoma patients.

- Continence Care (26% of Rev): Catheters and urological products, led by the powerhouse 180 Medical brand.

- Infusion Care (19% of Rev): The "tubing" for insulin pumps and non-diabetes therapies like Parkinson’s.

The Revenue Engine: Over 85% of revenue is recurring. Once a patient is prescribed a Convatec ostomy bag or infusion set, they rarely switch. This creates a "sticky" cash flow that is highly attractive during economic uncertainty.

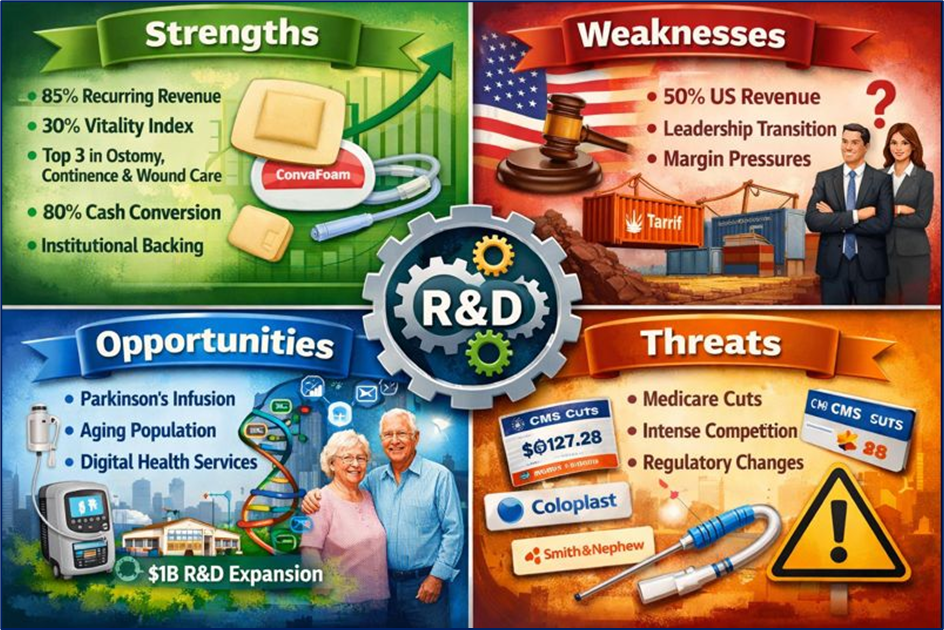

Deep-Dive SWOT Analysis

Source: Kalkine Group

Strengths

- High Recurring Revenue: ~85% of sales come from chronic care products that patients must use daily.

- The "Vitality Index": 30% of revenue now comes from products launched in the last 5 years (e.g., ConvaFoam, GentleCath Air), proving a successful R&D engine.

- Leading Market Positions: Global Top 3 player in Ostomy, Continence, and Wound Care categories.

- Strong Cash Conversion: On track for 80% equity cash conversion, allowing for consistent dividends and buybacks.

- Institutional Backing: Increasing stakes from giants like Fidelity signal long-term confidence.

Weaknesses

- US Market Concentration: Over 50% of revenue is tied to North America, making the company highly sensitive to US regulatory changes.

- Leadership Transition Risk: Following the death of Karim Bitar, the new team (Jonny Mason and Fiona Ryder) must prove they can maintain the "FISBE" strategy momentum.

- Margin Pressures: Exposure to global supply chain costs and a 30-basis-point hit from current tariff headwinds.

Opportunities

- Non-Diabetes Infusion: Rapid expansion into Parkinson’s disease treatments (partnering with AbbVie) provides a new growth frontier.

- Aging Demographics: A structurally growing global population over 65 ensures a permanent expansion of the patient base.

- Digital Health Integration: Leveraging their "Home Services Group" to provide direct-to-patient data and care management.

- R&D Expansion: Recent plans to invest over $1 billion in new R&D facilities in the US and UK.

Threats

- CMS Reimbursement Cuts: The US Medicare decision to cap "skin substitute" (InnovaMatrix) payments at $127.28/sq cm creates a 1-2% revenue headwind for 2026.

- Intense Competition: Rivals like Coloplast and Smith & Nephew are aggressively competing on price in the advanced wound care space.

- Regulatory Uncertainty: Changes in US "catheter codes" and competitive bidding could pressure margins in the Continence segment.

Latest Business Updates: Growth Amidst Headwinds

Despite a heavy regulatory cloud over its InnovaMatrix product, Convatec’s latest trading update (Nov 2025) was surprisingly robust:

- Guidance Upgraded: Organic revenue growth (ex-InnovaMatrix) was narrowed to a strong 6.0%–6.5%.

- The "Infusion" Explosion: The Infusion Care division is delivering double-digit growth, fueled by the rise of automated insulin delivery.

- Share Buyback: The company has already repurchased $202 million of its $300 million programme, providing a floor for the share price.

- Pipeline Momentum: New launches like ConvaNiox (nitric oxide dressing) and ConvaFiber are set to hit the market in 2026.

The Risks: What to Watch

While the stock is trending upward, it isn't without hurdles. The InnovaMatrix headwind is real; revenue for that specific line is expected to drop to $70 million in 2025 and lower in 2026 due to Medicare price caps. Furthermore, any strengthening of the British Pound could "wash away" some of the gains seen from their massive US-based earnings when translated back to GBP.

Conclusion

Convatec’s ~3% jump on December 17 is a classic case of a "quality recovery." By shaking off the temporary technical pressure of leadership changes and gaining fresh support from Fidelity, the stock is re-aligning with its fundamental strength.

With a business model predicated on essential, daily-use medical supplies and an R&D pipeline that is finally yielding high-margin results, Convatec remains a premier defensive growth play in the FTSE 100 for 2026.

Source: Trading View, 17 December 2025

Please wait processing your request...

Please wait processing your request...