Antofagasta PLC (LSE: ANTO), the Chile-focused copper mining group listed on the London Stock Exchange, experienced a notable intraday surge of approximately 5% in its UK-listed shares (ANTO) today. This analytical report examines the likely reasons for the movement, delves into the company's latest operational and financial data, outlines its strategic direction, and assesses the associated risks.

Key Drivers for the Share Price Movement

The significant upward movement in Antofagasta’s share price can typically be attributed to a combination of internal corporate developments and broader macroeconomic factors influencing the copper market.

1. Macroeconomic Tailwinds: Copper Market Strength

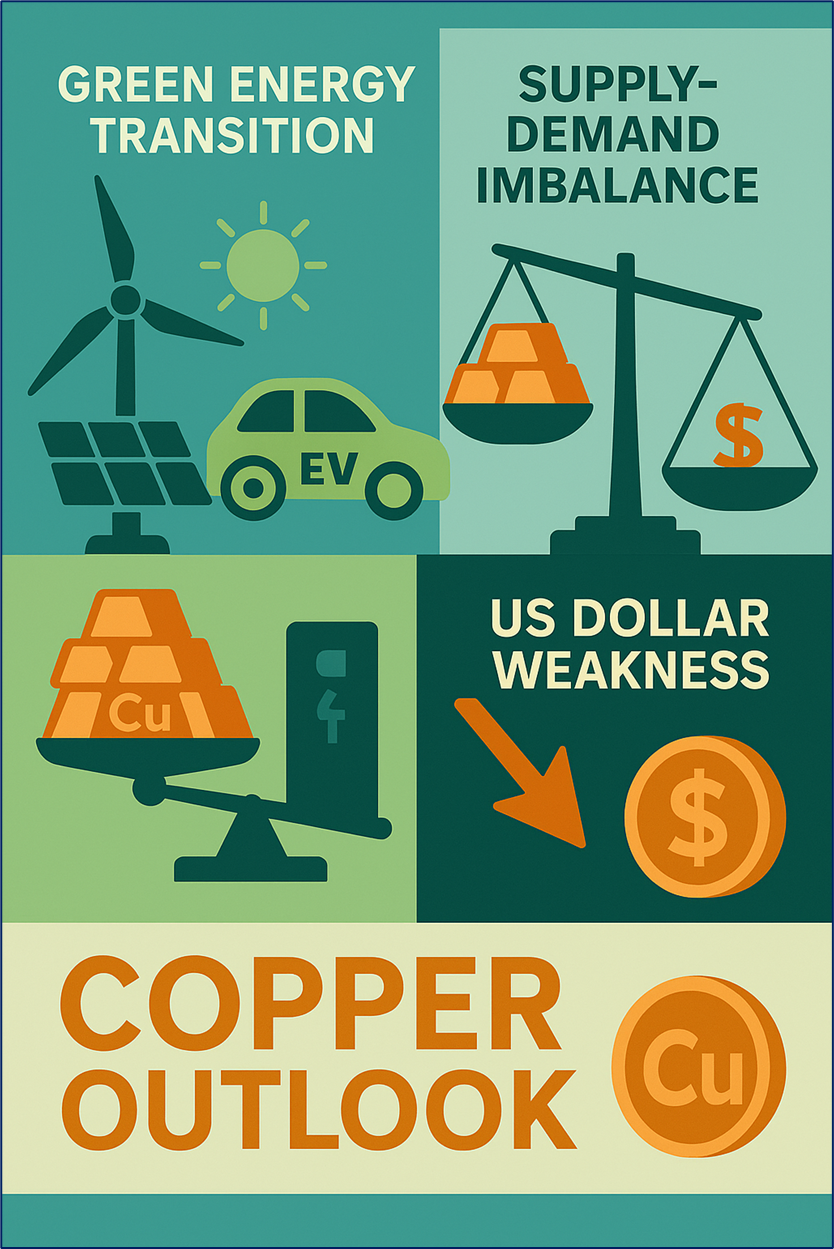

As a pure-play copper producer, Antofagasta’s stock performance is highly correlated with the price of copper. A primary driver for the surge is the potential for an uptick in global copper prices. Positive sentiment may stem from:

- Green Energy Transition: Continued strong global demand forecasts for copper, a critical material in electrification, electric vehicles (EVs), and renewable energy infrastructure.

- Supply-Demand Imbalance: Persistent expectations of a structural long-term supply deficit in the copper market, driven by limited new discoveries and complex permitting processes.

- US Dollar Weakness: A weaker US dollar generally makes dollar-denominated commodities, like copper, more affordable for international buyers, increasing demand and prices.

Source: Kalkine Group

2. Corporate Confidence and Strategic Execution

Recent market updates from Antofagasta, which reinforce the company's ability to execute its growth strategy, likely contributed to investor confidence:

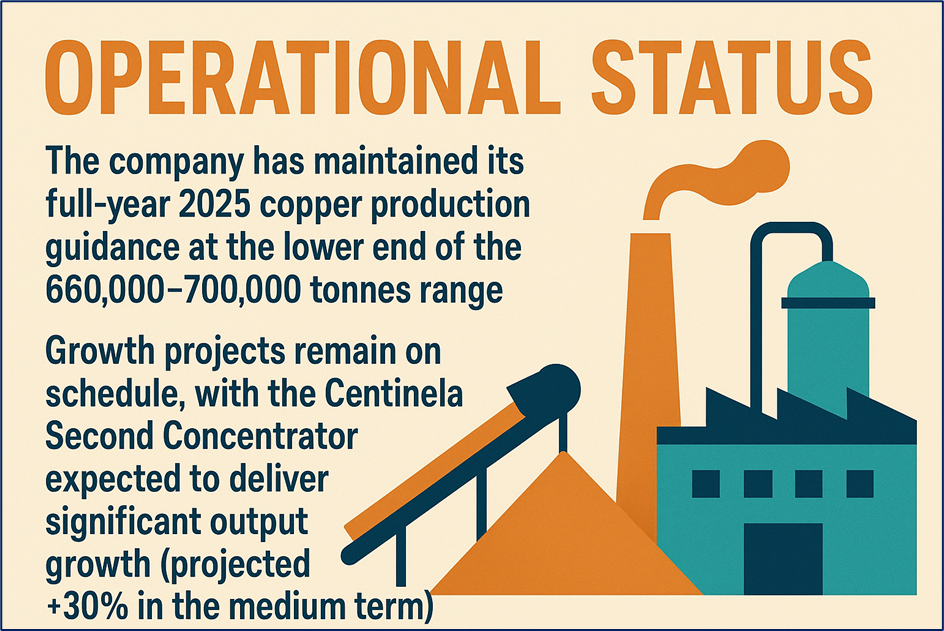

- Growth Project Momentum: Positive updates regarding the progress of major capital expenditure programs, such as the Centinela Second Concentrator and the Los Pelambres Desalination Plant Expansion, may suggest a clearer path to future production increases and reduced operational risk.

- Operational Efficiency: Continued success of the company's Competitiveness Programme, aiming for material cost savings, may have signalled improved margins to the market.

Source: Kalkine Group

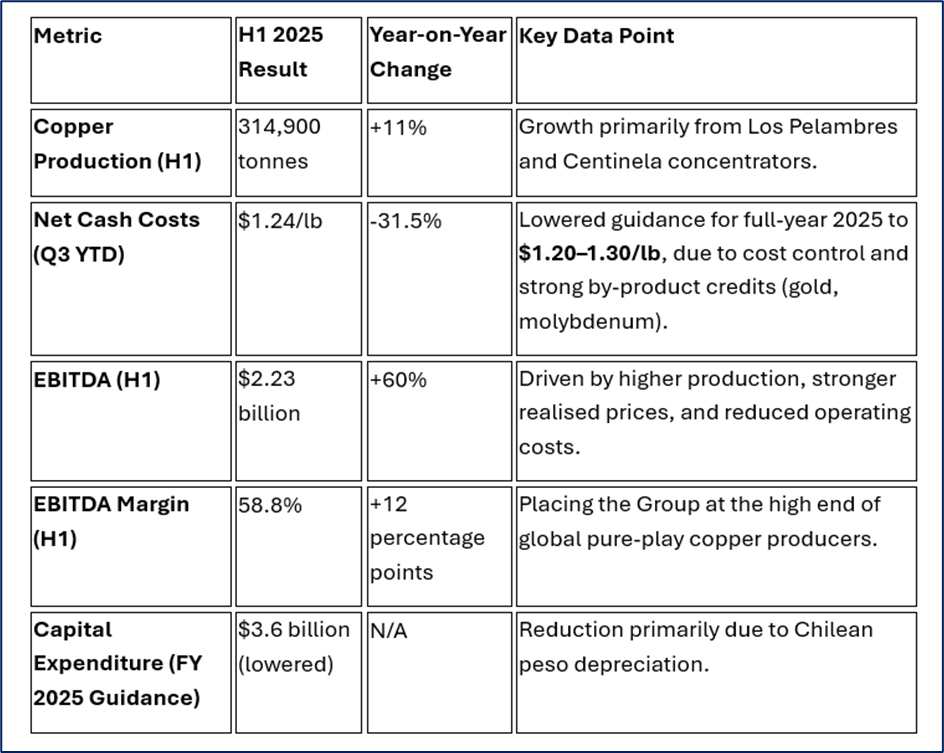

Latest Operational and Financial Data (Based on H1 and Q3 2025 Reports)

Recent disclosures highlight robust operational delivery and financial strength, positioning the company favourably amidst market volatility.

Data Source: Company Data, Kalkine Group

Source: Kalkine Group

Strategy and Outlook

Antofagasta's strategy remains explicitly focused on being a pure-play, high-margin copper producer with a commitment to sustainable growth and disciplined capital allocation.

- Core Strategy: To deliver profitable and responsible growth by maximising value from its existing world-class Chilean assets. This includes systematically expanding capacity, improving processing efficiency, and advancing exploration.

- Growth Program: The main thrust is the delivery of the Centinela Second Concentrator, which will significantly increase copper and by-product (gold) production, and the Los Pelambres Desalination Plant expansion, which mitigates water risk and secures long-term production.

- Financial Discipline: A stated commitment to a robust balance sheet (Net debt/EBITDA ratio of 0.54x in H1 2025) and a predictable dividend policy (35% payout of underlying net earnings).

- Sustainability: Key focus areas include securing water supply via desalination (63% seawater sourcing in H1 2025) and reducing greenhouse gas emissions (targeting 50% reduction in Scope 1 and 2 by 2035).

The outlook remains positive for copper fundamentals, with global market forecasts predicting a growing supply gap, reinforcing the long-term value of Antofagasta's expanding, high-margin portfolio.

Source: Kalkine Group

Key Investment Risks

Despite the strong recent performance, the investment case for Antofagasta carries several risks inherent to the sector and its geographic focus:

- Commodity Price Volatility: As a pure-play copper miner, the company remains highly susceptible to fluctuations in global copper prices, which can be driven by global economic growth, geopolitical events, and US dollar strength.

- Geopolitical and Regulatory Risk (Chile): Operations are concentrated in Chile, exposing the company to changes in local mining regulations, water usage laws, and political stability, including potential tax or royalty changes.

- Operational and Climate Risks: Challenges include declining ore grades at established mines, rising input inflation, and the ongoing regional risks associated with drought and extreme weather events.

- Project Execution Risk: The successful and timely completion of major capital-intensive growth projects (Centinela, Los Pelambres) is critical to the medium-term outlook. Delays or cost overruns could impact future free cash flow.

Conclusion

The 5% surge in Antofagasta’s UK share price today appears to reflect a constructive intersection of positive macroeconomic factors (strong copper demand outlook) and encouraging company-specific fundamentals. The latest financial results demonstrate superior margins and effective cost control, while the growth projects signal a clear pathway to higher future production volumes.

The company's strategic commitment to expanding capacity and managing critical risks, particularly water supply and operating costs, has likely bolstered investor sentiment. However, the inherent cyclicality of commodity prices and the concentrated geopolitical exposure in Chile mandate a balanced, analytical perspective on the company’s trajectory.

Source: Trading View, 3 December 2025, 12:30 PM GMT

Please wait processing your request...

Please wait processing your request...