On January 5, 2026, the London Stock Exchange witnessed a historic milestone as the FTSE 100 closed above 10,000 points for the first time. Leading this charge was the Chilean mining giant Antofagasta PLC (LSE: ANTO), which saw its share price jump 5.96% to end the day at 3,459.00p.

While the broader market was optimistic, Antofagasta's outperformance was driven by a "perfect storm" of geopolitical tension, record-breaking commodity prices, and strategic supply-side maneuvers.

Key Drivers: Why the 6% Spike?

Source: Kalkine Group

The rally on January 5th wasn't just a "rising tide" effect; it was fueled by specific fundamental shifts:

- Record Copper Prices: Copper surged past $12,000 per tonne for the first time on record. Disruptions in global mine supply, combined with new U.S. tariffs, created a supply squeeze that benefited pure-play producers like Antofagasta.

- Geopolitical Safe Haven: Following U.S. actions regarding the leadership in Venezuela, global uncertainty spiked. Investors rotated heavily into "hard assets" and miners, viewing them as a hedge against currency volatility and geopolitical risk.

- The "Zero-Fee" Breakthrough: Antofagasta recently finalized a landmark deal with Chinese smelters for 2026 Treatment and Refining Charges (TC/RCs) at $0 per metric ton. This is the lowest level in history, essentially allowing the miner to keep a larger share of the copper's value as smelters compete for scarce concentrate.

- Supply Constraint Sentiment: News of a strike at Capstone Copper’s Mantoverde Mine in Chile on January 2nd added to fears of a regional supply crunch, putting upward pressure on the stock prices of stable operators in the region.

Latest Business Model & Strategy

Antofagasta has evolved from a traditional miner into a technology-driven copper powerhouse. Its 2026 business model focuses on two pillars: Resilience and Expansion.

- The "Pure-Play" Focus

Unlike diversified giants like Rio Tinto or BHP, Antofagasta remains a pure-play copper producer. This makes it the primary vehicle for investors looking to bet on The Electrification Mega-trend (EVs, AI data centers, and renewable grids).

- Operational Efficiency

The company operates four major mines in Chile: Los Pelambres, Centinela, Antucoya, and Zaldívar. The strategy now involves:

- Desalination Dominance: To combat Chile's water scarcity, the company is rapidly expanding its desalination plants to ensure 100% of mining water comes from the sea or recycled sources.

- By-Product Maximization: Antofagasta is leveraging high Gold and Molybdenum prices as "credits" to lower its net cash costs for copper production.

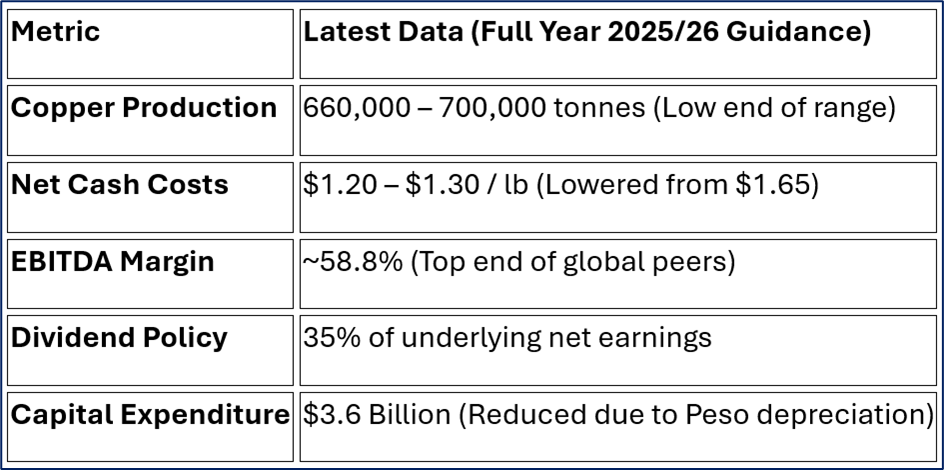

Financial & Operational Updates (Jan 2026)

Source: Company Data

The company reported that while production volume is at the lower end of expectations due to grade declines, profitability has reached a 5-year high due to massive cost-cutting and high realized prices for gold and copper.

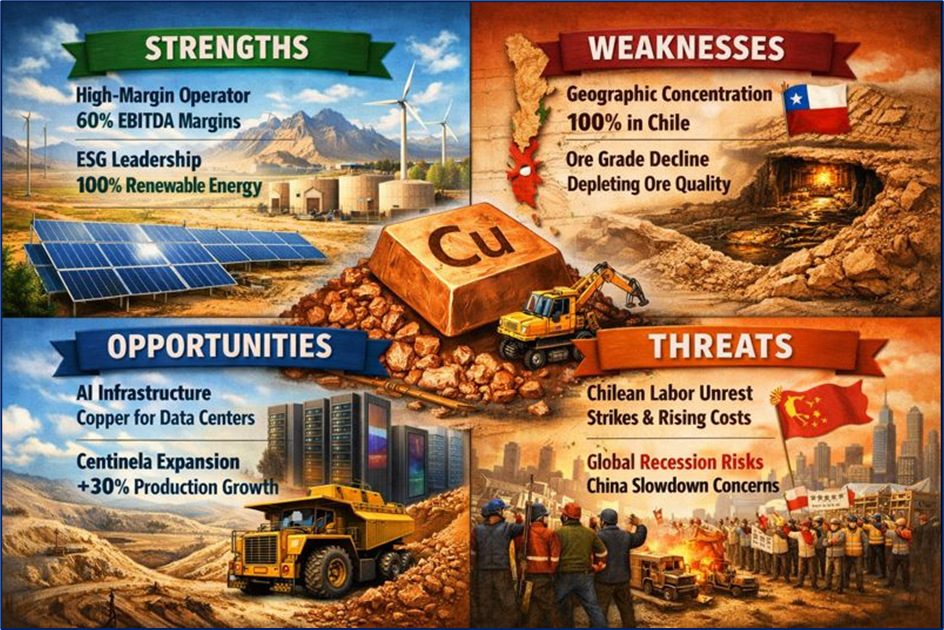

SWOT Analysis: 2026 Outlook

Source: Kalkine Group

Strengths

- High-Margin Operator: EBITDA margins near 60% are among the highest in the world.

- ESG Leadership: 100% of mining operations are powered by renewable energy.

- Zero TC/RC Terms: Unprecedented bargaining power with Chinese smelters.

Weaknesses

- Geographic Concentration: 100% of production is in Chile, exposing it to local political and regulatory shifts.

- Ore Grade Decline: Like many mature mines, the "easy" copper has been taken, requiring more energy to extract the same amount of metal.

Opportunities

- AI Infrastructure: The global explosion in AI data centers requires massive amounts of copper for power distribution.

- Centinela Expansion: The Second Concentrator project is set to lift copper production by over 30% in the coming years.

Threats

- Chilean Labor Unrest: Recent strikes at neighboring mines (Mantoverde) signal potential for rising labor costs.

- Global Recession Risks: While copper is "green," it is also "industrial." A sharp slowdown in China’s construction sector could cap price gains.

Critical Risks to Watch

- Water Scarcity: Despite desalination, prolonged droughts in Chile remain a systemic risk to processing volumes.

- Resource Nationalism: Any future changes to the Chilean Mining Royalty tax could eat into the high margins seen in early 2026.

- Tariff Wars: Increased U.S. tariffs on Chinese goods may complicate the global flow of refined copper, creating price volatility.

Conclusion

Antofagasta’s 6% surge on January 5th is a reflection of its status as a premium copper vehicle in a world starved for supply. By successfully negotiating $0 smelting fees and benefiting from record-high commodity prices, the company has positioned itself as a primary beneficiary of the 2026 "Green Commodity Boom." However, investors must weigh these record highs against the operational realities of mining in a high-inflation, strike-prone environment.

Please wait processing your request...

Please wait processing your request...