FTSE-100 Listed DCC PLC didn’t just move on general market noise today. The stock jumped primarily because the company successfully executed a massive £600 million cash return to shareholders while simultaneously confirming its transformation into a specialized energy giant.

Source: Kalkine Group

- The £600m Tender Offer Success: On Dec 19, DCC announced the results of its massive share buyback (tender offer). They bought back ~11.6 million shares at a strike price of £51.70. This removes roughly 12% of the company's total shares from the market.

- Scarcity Value: By reducing the share count so drastically, remaining shares now represent a larger slice of the company’s future earnings (EPS accretion).

- Strategic Validation: The buyback isn't just financial engineering; it is funded by the divestment of their Healthcare division, signaling that their strategic pivot is working and cash is actually landing in investors' pockets.

- Analyst Support: The market views this as "promise kept." Management promised to simplify the confusing conglomerate structure and return cash—today, they delivered.

2. Business Update: The "Great Split"

For years, DCC was a "boring" conglomerate doing three unrelated things: Energy, Healthcare, and Tech. That model is officially dead.

- Exit from Healthcare: The sale of DCC Healthcare is the fuel behind this cash bonanza.

- Review of Technology: The Tech division is currently under strategic review (likely to be sold next), which would leave DCC as a pure-play energy company.

- Earnings Resilience: Recent interim results showed that despite a revenue dip (due to lower commodity prices), operating profits grew, proving they can squeeze more margin out of every litre of fuel sold.

3. The New Business Model: "Cleaner Energy in Your Power"

DCC is transitioning from a "delivery truck conglomerate" to an Energy Transition Enabler.

- Old Model: Buy fuel, put it in a truck, deliver it, collect a small margin. Repeat for laptops and vitamins.

- New Model (Energy Pure-Play):

- Core Distribution: Still delivering LPG and fuels to off-grid customers (high barrier to entry, loyal customer base).

- Energy Management: Selling "Energy as a Service"—installing heat pumps, solar panels, and managing energy efficiency for commercial clients.

- Biofuels: Aggressively swapping standard diesel/gas for HVO (Hydrotreated Vegetable Oil) and biomethane to keep customers compliant with green laws.

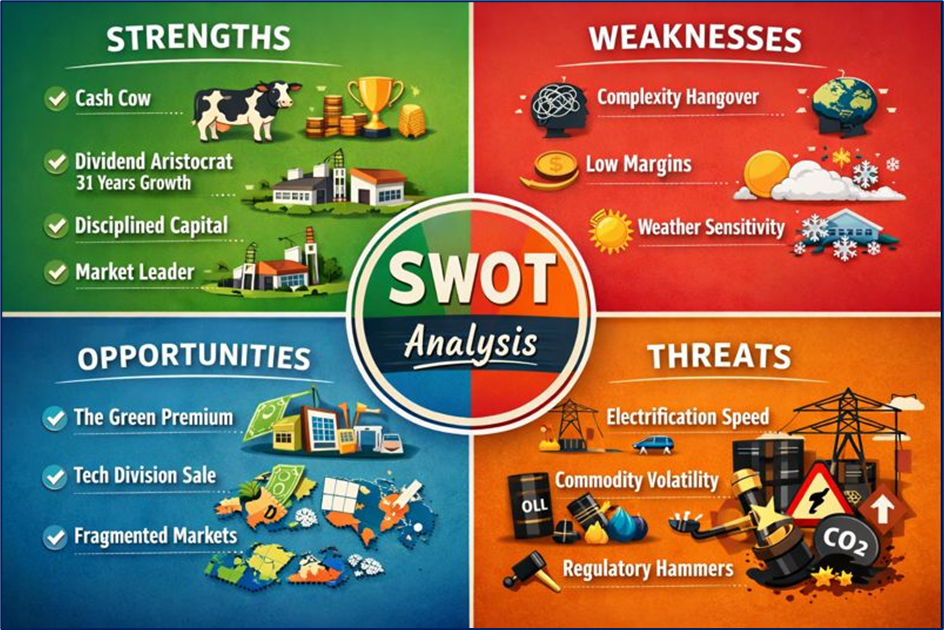

4. SWOT Analysis

Source: Kalkine Group

Strengths (Internal)

- Cash Cow: The energy distribution business generates massive, reliable free cash flow.

- Dividend Aristocrat: 31 years of unbroken dividend growth—a rarity in the FTSE 100.

- Disciplined Capital: Proven track record of buying small local energy distributors at good prices and integrating them perfectly (roll-up strategy).

- Market Position: Dominant player in off-grid energy (rural heating, industrial) where competitors are scarce.

Weaknesses (Internal)

- Complexity Hangover: The market still remembers them as a confusing conglomerate; it takes time to re-rate as a focused energy stock.

- Low Margins: Distribution is inherently a low-margin, high-volume game. They rely on efficiency, not pricing power.

- Weather Sensitivity: A warm winter means less heating fuel sold. Period.

Opportunities (External)

- The Green Premium: As they convert customers to renewables (solar/heat pumps), they can capture higher margins than just delivering commoditized fuel.

- Tech Division Sale: If they successfully sell the Technology arm, expect another massive cash injection/buyback.

- Fragmented Markets: The US and European energy distribution markets are still highly fragmented—plenty of targets to acquire.

Threats (External)

- Electrification Speed: If rural customers switch to electric grids faster than DCC can sell them heat pumps/solar, they lose the customer entirely.

- Commodity Volatility: Sudden spikes in oil/gas prices can hurt working capital, even if they pass costs to consumers.

- Regulatory Hammers: Aggressive carbon taxes or bans on liquid fuels in Europe could threaten their core legacy business before the new "green" business is fully scaled.

5. Key Risks to Watch

- Execution Risk: Can they actually become a "Green Energy Manager"? Selling solar panels is very different from filling oil tanks.

- Valuation Trap: If the "Energy" business doesn't grow fast enough to replace the lost earnings from Healthcare/Tech, the stock could stagnate despite buybacks.

- Interest Rates: As a capital-intensive business that often uses debt for acquisitions, "higher for longer" rates could slow their roll-up strategy.

6. Conclusion

DCC’s rise on Dec 19 is a classic case of shareholder value realization. The company is shrinking its share count while sharpening its focus. By dumping the "conglomerate discount" and doubling down on energy, they are betting big that the market will value a focused energy distributor higher than a confused holding company.

For retail investors, the story has shifted from "reliable boring dividend stock" to "active transformation play." The £600m tender offer was the proof of concept; the next leg up depends on whether they can successfully sell the Tech division and convince the market they are a growth play in the energy transition.

Source: Trading View, 19 December 2025, 9:45 AM GMT

Please wait processing your request...

Please wait processing your request...