The London Stock Exchange opened its first full week of 2026 with a notable spark in the industrial sector. Diploma PLC (LSE: DPLM), the specialist distribution giant, saw its shares climb approximately 2% on January 5, 2026, outperforming the broader FTSE 100 index.

While often flying under the radar compared to flashy tech stocks, Diploma is proving once again why it is a darling for institutional "quality" investors.

Key Drivers: The "Jan 5" Momentum

Source: Kalkine Group

The 2% lift isn't a fluke; it's the result of several converging factors:

- Dividend "Capture" & AGM Anticipation: With the Annual General Meeting (AGM) scheduled for January 14, 2026, and the ex-dividend date (44.1p per share) set for January 15, investors are positioning themselves to capture the final FY25 payout.

- Safe-Haven Inflow: Amidst early-year market volatility, capital is rotating into "compounding" stocks with high visibility. Diploma’s 105% free cash flow conversion makes it a fortress in uncertain climates.

- M&A Rumblings: Following its aggressive acquisition streak in late 2025 (six deals in Q4 alone), the market is pricing in the high probability of a new "bolt-on" announcement early in Q1 2026.

The Modern Business Model: More Than a Middleman

Diploma has evolved far beyond simple distribution. It operates a decentralized, value-add model that focuses on three high-margin sectors:

- Controls: Specialized wiring, connectors, and fasteners for Aerospace, Defense, and Data Centers. This sector saw a staggering 20% organic growth in the most recent fiscal year.

- Seals: Critical aftermarket components for heavy machinery. This provides a "sticky" revenue stream as these parts are essential for maintenance, not just new builds.

- Life Sciences: Consumables and instrumentation for MedTech and diagnostics.

The "Secret Sauce": Diploma doesn't just ship boxes; it provides technical expertise. By becoming an integral part of the customer's supply chain (e.g., designing custom seal kits or providing F1-grade wiring), they command operating margins of ~22.5%, significantly higher than standard wholesalers.

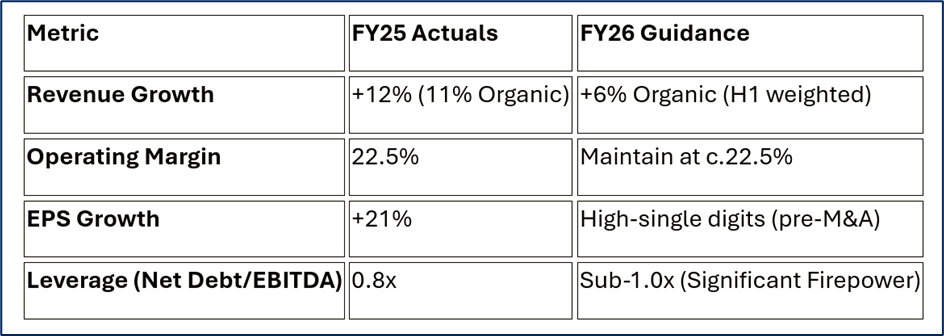

Financial & Operational Health Check (2025-26)

The latest updates from the company’s preliminary results (Nov 2025) paint a picture of aggressive efficiency:

Source: Kalkine Group

Operational Highlight: The acquisition of Peerless Aerospace has significantly expanded their US footprint, allowing them to cross-sell specialized fasteners into the booming North American defense and space markets.

SWOT Analysis: The Analytical Edge

Source: Kalkine Group

Strengths

- High Switching Costs: Their products are "mission-critical" but low-cost relative to the total system. Customers rarely switch suppliers for a few pence if it risks a multi-million pound machine failing.

- Capital Light: Reinvests only ~2% of revenue into capex, leaving 98% for dividends and acquisitions.

- Decentralized Culture: Local managers are empowered to make quick decisions, keeping the company agile.

Weaknesses

- Inventory Intensity: To guarantee "next-day" service, they must hold high stock levels, which can tie up cash during sudden economic slowdowns.

- Integration Risk: The model relies on constant acquisitions. Any failure in cultural or operational integration can dilute the "Diploma Brand."

Opportunities

- Energy Transition: Demand for specialized "Controls" is surging as the world shifts to Electric Vehicles (EVs) and smart grids.

- Digitalization: Their ongoing investment in B2B e-commerce portals is expected to drive 30% higher customer spend through automated cross-selling.

Threats

- Currency Headwinds: With over 50% of revenue from North America, a weakening Dollar against the Pound can erode reported earnings.

- Regulatory Shifts: Changing healthcare or aerospace compliance standards can delay new product entries by 6–12 months.

The Bottom Line: Risk & Outlook

While the stock is up, it is not without risk. The Price-to-Earnings (P/E) ratio sits around 38x, which is a premium valuation. This leaves little room for error; if organic growth dips below 5%, a "valuation reset" could occur.

However, with a 0.8x leverage ratio, Diploma has the "financial firepower" to buy its way out of trouble. Their ability to acquire small, private businesses at 8x EBITDA and immediately benefit from FTSE 100-level synergies remains their greatest competitive advantage.

Please wait processing your request...

Please wait processing your request...