The London Stock Exchange witnessed a significant spark on December 17, 2025, as Phoenix Group Holdings (LSE: PHNX) shares surged approximately 3.5%, reaching new 52-week highs near GBX 727. For retail investors tracking the FTSE 100, this wasn't just a minor fluctuation; it was a signal of a major "pivot" in the company's financial story.

The Catalyst: Why the 3.5% Jump Today?

The primary driver behind today's rally is a high-conviction upgrade from UBS. The investment bank shifted its rating from ‘Neutral’ to ‘Buy’, aggressively hiking its price target from GBX 670 to GBX 770.

Key Takeaways from the UBS Note:

- Excess Cash Generation: Phoenix is generating at least £300 million per year in excess cash above its operational needs.

- The "Debt-Free" Horizon: The company is currently using this cash to deleverage. UBS predicts this debt reduction will be complete by the first half of 2025 (within the next 6 months).

- Capital Returns: Once debt targets are met, UBS expects Phoenix to unleash £150 million annually in share buybacks, potentially pushing the "all-in" yield (dividends + buybacks) above 10%.

Source: Kalkine Group

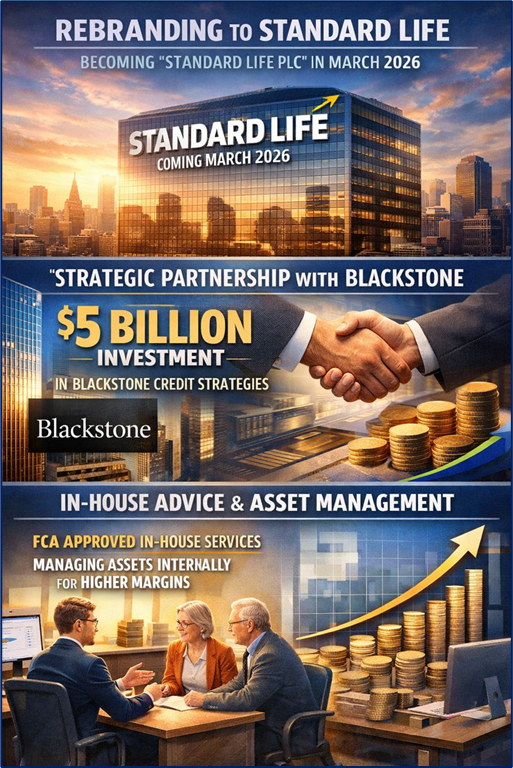

Business Update: From "Closed-Book" to Growth Engine

Historically, Phoenix was known as a "consolidator"—a company that bought old, closed pension books and milked them for cash. However, the 2025 strategy has seen a total evolution:

- Rebranding to Standard Life: Management confirmed that in March 2026, the group will officially change its name to Standard Life PLC, putting its most powerful consumer brand front and center.

- Strategic Partnership with Blackstone: On the same day as the share spike, reports highlighted a massive strategic collaboration where Phoenix will invest up to $5 billion across Blackstone’s credit strategies, enhancing its asset management yield.

- In-House Advice & Asset Management: The company recently received FCA approval for its in-house advice proposition. By managing more assets internally rather than outsourcing, they are capturing higher margins.

Source: Kalkine Group

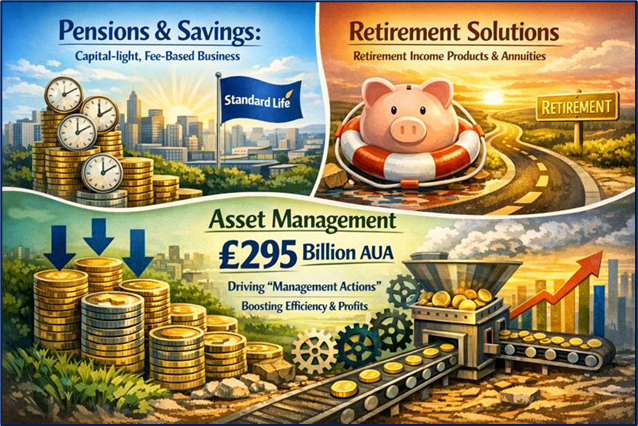

The 2025 Business Model: The "Cash-Flow Machine"

Phoenix operates a diversified model focused on three core pillars:

- Pensions & Savings: Capital-light, fee-based business (Standard Life brand).

- Retirement Solutions: Bulky "Retirement Income" products and annuities.

- Asset Management: Optimizing the £295 billion of assets under administration (AUA) to drive "management actions"—internal efficiency gains that drop straight to the bottom line.

Source: Kalkine Group

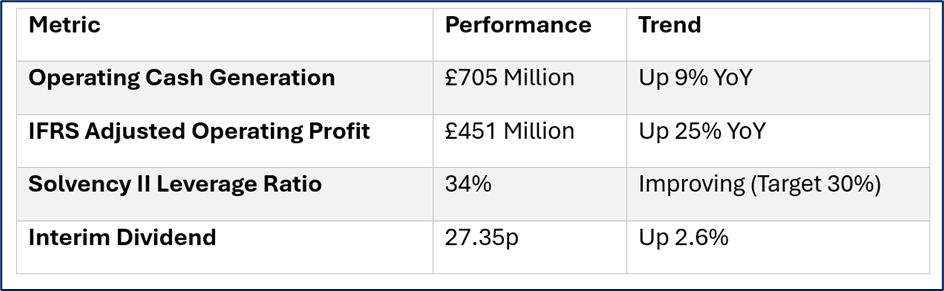

Financial Snapshot (H1 2025 Results)

Source: Company Data

The Risk Factors: What Could Dampen the Flame?

Despite the bullish sentiment, Phoenix isn't without its hurdles:

- Interest Rate Sensitivity: As a major provider of annuities, Phoenix is highly sensitive to the yield curve. Rapidly falling interest rates can create asset-liability mismatches, though their hedging programs are currently rated as "very resilient" by the PRA's LIST 2025 stress tests.

- Credit Downturns: While UBS noted the balance sheet is resilient, a global recession could lead to credit defaults in the corporate bond portfolios that back their insurance long-term liabilities.

- Operational Execution: The migration of millions of customer policies to new tech platforms (like TCS BaNCS and Wipro) carries inherent "key-man" and technical risks.

Conclusion: The "Yield Play" of the Year?

Phoenix Group has successfully transitioned from a legacy consolidator into a modern, cash-generative retirement powerhouse. With a 10% prospective all-in yield and a clear path to ending its deleveraging phase, the market is finally beginning to re-rate the stock toward the GBX 770 mark.

The combination of a stronger brand (Standard Life), massive cash reserves, and a "Buy" stamp from major analysts has made PHNX the standout performer of the FTSE 100 this December.

Source: Trading View, 17 December 2025

Please wait processing your request...

Please wait processing your request...