_01_06_2026_05_10_32_293382.jpg)

The FTSE 100 opened 2026 with a clear signal from the mining sector: Rio Tinto (LSE: RIO) is moving into high gear. While the broader market remained cautious, Rio Tinto shares climbed ~2% on 5 January 2026, hitting a fresh 52-week high.

This isn't just a "holiday bounce"; it's the result of a massive structural shift in how the world’s second-largest miner operates.

Key Drivers: What’s Pushing the Stock Today?

Source: Kalkine Group

The 2% jump today is fueled by a "perfect storm" of operational milestones and macroeconomic tailwinds:

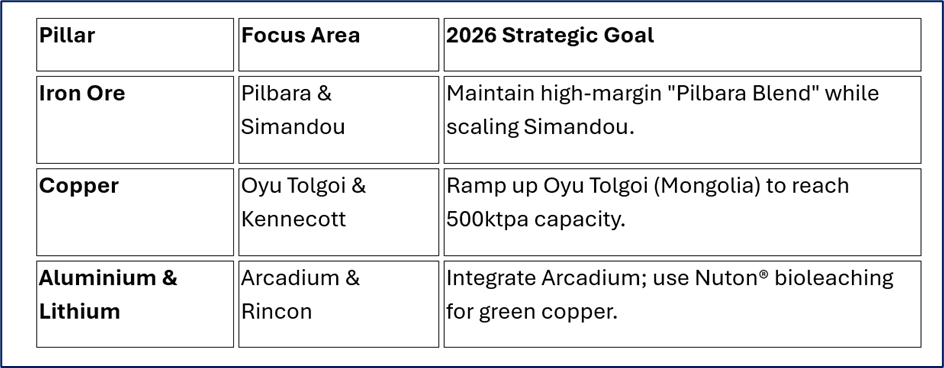

- Copper Guidance Upgrade: Markets are reacting to the late-2025 "Capital Markets Day" updates, where Rio upgraded its 2025 copper production to 860–875 kt while simultaneously slashing unit costs. Investors love a "higher volume, lower cost" narrative.

- The "Simandou" Factor: The massive Simandou iron ore project in Guinea—often called the "Pilbara of Africa"—successfully accelerated its first shipments to November 2025. Today’s sentiment reflects the de-risking of this multi-billion-dollar asset.

- Lithium Acquisition Synergy: Following the $6.7 billion acquisition of Arcadium Lithium (finalized in March 2025), Rio Tinto is now a Top 3 global lithium player. As EV demand forecasts for 2026 stabilize, Rio is no longer seen as "just an iron ore play."

- China’s "Advanced Manufacturing" Pivot: Goldman Sachs’ recent upgrade of China’s GDP growth to 4.8% for 2026—focused on high-tech manufacturing—has bolstered demand expectations for high-grade iron ore and aluminum.

The 2026 Business Model: "Stronger, Sharper, Simpler"

Rio Tinto has officially moved away from its legacy conglomerate structure to a tri-pillar model:

Source: Company Data

Financial & Operational Updates (Jan 2026)

- Production Growth: Rio expects a 7% increase in total production for 2025/2026, significantly higher than the industry average of 2-3%.

- Cost Discipline: The company achieved $650 million in annualized productivity gains by eliminating management layers and "non-core" programs in late 2025.

- Dividends: Rio remains a premier "dividend aristocrat" in the FTSE 100, maintaining a 40-60% payout policy with a current yield hovering around 3.6% to 5% depending on the listing.

- Capital Expenditure: Mid-term Capex is projected to drop below $10 billion after 2028 as major projects (Oyu Tolgoi, Simandou) move from construction to production.

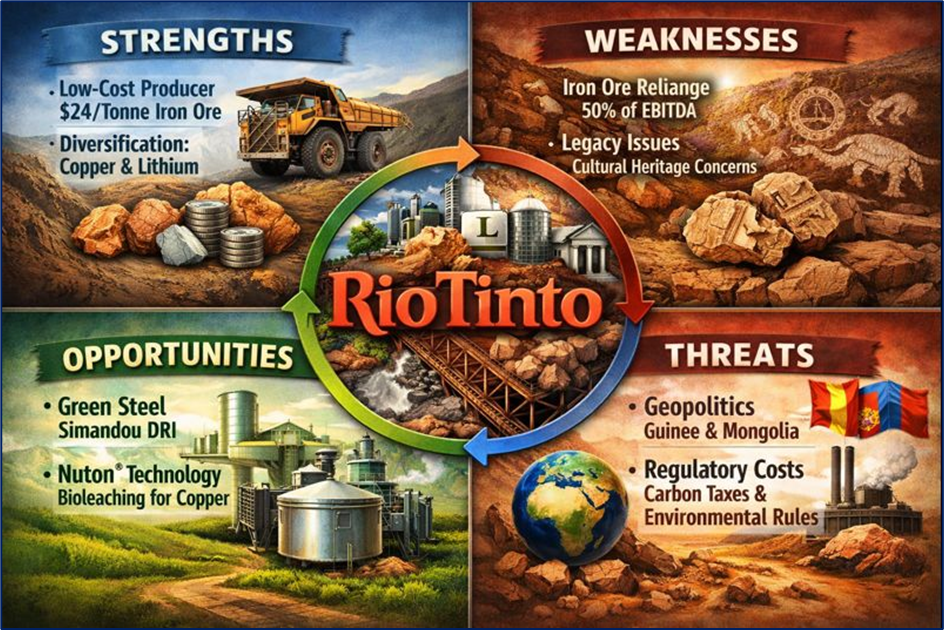

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Low-Cost Producer: Rio remains at the bottom of the cost curve for iron ore ($24/tonne range).

- Diversification: Rapidly growing exposure to "energy transition" metals (Copper/Lithium).

- Financial Fortress: Despite the Arcadium acquisition, the balance sheet remains robust with conservative net debt.

Weaknesses

- Iron Ore Reliance: Still generates over 50% of EBITDA from a single commodity.

- Legacy Issues: Ongoing pressure regarding cultural heritage management (post-Juukan Gorge reforms).

Opportunities

- Green Steel: High-grade ore from Simandou is ideal for low-carbon "Direct Reduced Iron" (DRI) steelmaking.

- Nuton® Technology: Proprietary bioleaching could unlock "un-mineable" copper deposits globally.

Threats

- Geopolitics: Heavy exposure to Guinea (Simandou) and Mongolia (Oyu Tolgoi).

- Regulatory Costs: Rising carbon taxes and stricter environmental regulations in Australia and Canada.

Critical Risks to Watch

- China’s Property Sector: While manufacturing is up, the Chinese property market remains a "dead weight" on bulk commodity prices.

- Weather Volatility: Recent years saw "four cyclones in one quarter" in the Pilbara; climate change remains a direct operational risk.

- Inflationary Opex: Labor and energy costs in Australia continue to squeeze margins, even as productivity rises.

Conclusion

Rio Tinto’s 2% climb on 5 January 2026 is a reflection of a company that has successfully pivoted from a "boring" iron ore miner to a high-growth "energy transition" powerhouse. By streamlining its management and hitting production milestones at Simandou and Oyu Tolgoi, the market is beginning to re-rate Rio as a diversified technology and materials leader rather than a cyclical commodity stock.

Please wait processing your request...

Please wait processing your request...