The final trading session of 2025 saw Eco (Atlantic) Oil & Gas (LSE: ECO) deliver a masterclass in year-end rallies. While the broader FTSE struggled, ECO shares vaulted 14.51% to close at GBX 29.20, marking a new 52-week high.

This isn't just a "Santa Rally"—it’s the culmination of a strategic pivot that has transformed the company from a speculative explorer into a de-risked partner of choice.

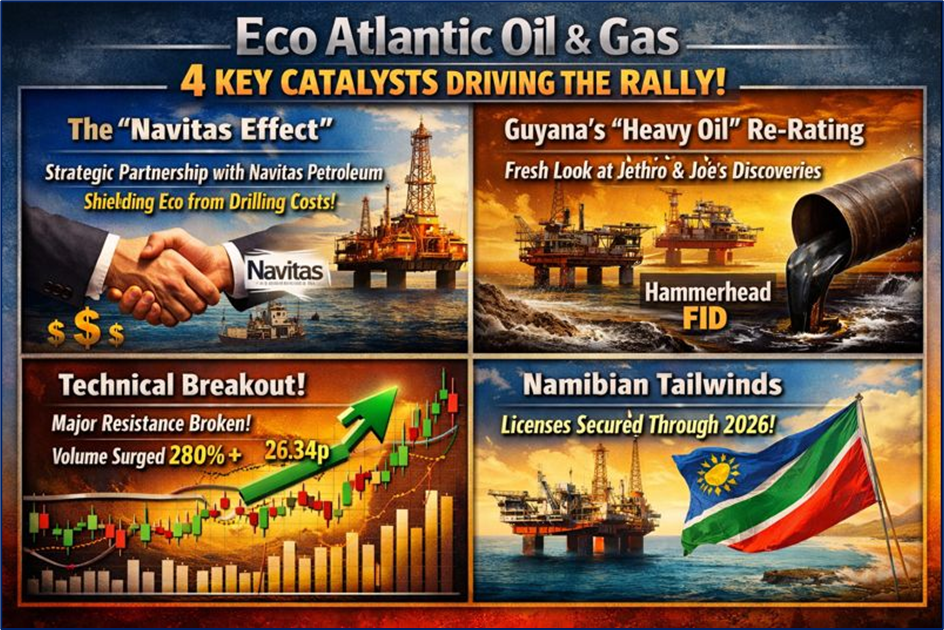

Key Drivers: Why the December 31st Explosion?

The 14.5% surge was fueled by a "perfect storm" of technical breakouts and recent fundamental de-risking:

Source: Kalkine Group

- The "Navitas Effect": The market is finally pricing in the December 4th Strategic Partnership with Navitas Petroleum. Navitas’s entry into the Orinduik Block (Guyana) and Block 1 CBK (South Africa) provides a multi-million dollar "carry," essentially shielding Eco from high-stakes drilling costs.

- Guyana’s "Heavy Oil" Re-Rating: Following ExxonMobil’s FID on the Hammerhead project, Eco has pivoted its strategy for the Jethro-1 and Joe-1 discoveries. The market is betting on a "fresh look" at these heavy oil assets as viable commercial hubs rather than stranded assets.

- Technical Breakout: On December 31, the stock broke through a major resistance level at 26.34p. This triggered algorithmic buying and momentum trades, with volume spiking over 280% above the session average.

- Namibian Tailwinds: With license extensions secured for PELs 97, 99, and 100 through September 2026, Eco has cleared the regulatory "cliff" that often plagues junior explorers.

Latest Business Model: The "Partner & Carry" Blueprint

Eco Atlantic has shifted away from the "high-equity, high-risk" model. Its 2026 business model is built on Strategic Optionality:

- Farm-Out Specialist: Eco acquires high-potential acreage early, then "farms out" majority stakes (to giants like Navitas or Azinam) in exchange for cash and a "carry" on drilling costs.

- Low Overhead, High Exposure: By maintaining 15–20% interests while being "carried," Eco retains massive upside to a discovery without the "cash call" risks that bankrupt smaller peers.

- Three-Basin Diversification: They are one of the few juniors with meaningful footprints in the world's three hottest basins: The Orange Basin (Namibia/SA), The Guyana-Suriname Basin, and The Walvis Basin (Namibia).

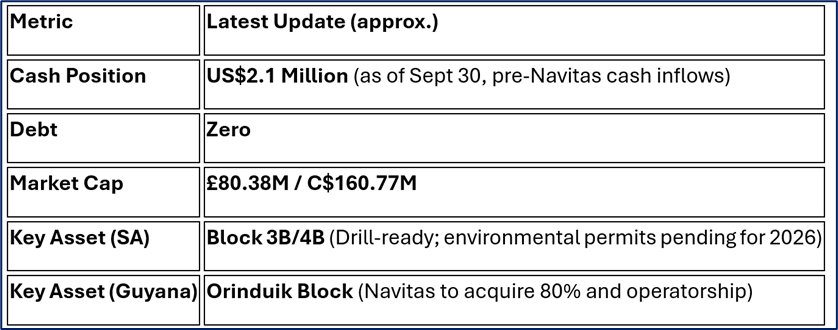

Financial & Operational Snapshot (Q2 2026/Dec 2025)

Source: Company Data

Operational Milestone: The South African Block 1 has been renamed Block 1 CBK in honor of the late co-founder Colin Kinley, signaling a transition into the next phase of development.

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- World-Class Partners: Teaming up with Navitas and TotalEnergies (via Block 3B/4B).

- Debt-Free Balance Sheet: Highly unusual for a junior explorer in a high-interest environment.

- Diversified Portfolio: Not reliant on a single well or single country.

Weaknesses

- Negative Earnings: Still in the "exploration loss" phase with a P/E of -28.33.

- Small Cash Buffer: Relies heavily on farm-in payments and "carries" to stay liquid.

Opportunities

- Orange Basin Boom: Any discovery by neighbors in the South African/Namibian Orange Basin immediately re-rates Eco’s adjacent blocks.

- Suriname Proximity: Recent discoveries in Suriname increase the "near-field" appeal of the Orinduik block.

Threats

- Permitting Delays: South African environmental authorizations (Block 3B/4B) have been pushed into 2026.

- Oil Price Volatility: A sub-$70 oil environment could cool farm-out interest from majors.

The "High-Risk" Warning

Despite the 14.5% gain, investors should note the very high volatility. The stock has a beta of 1.95, meaning it moves nearly twice as much as the broader market. Technical indicators suggest the next resistance level is 38.26p, but any delay in 2026 drilling permits could lead to a rapid retracement to support at 23.24p.

Conclusion

Eco (Atlantic) Oil & Gas ended 2025 as one of the FTSE AIM’s standout performers. By successfully navigating the transition from "explorer" to "strategic partner," the company has built a bridge to 2026 that is paved with carried costs and high-impact catalysts. While the path ahead is fraught with the usual "drill-bit" risks, the Dec 31st surge signals a market that is finally waking up to the value of its Atlantic Margin mosaic.

Please wait processing your request...

Please wait processing your request...