While most traders were wrapping gifts, Ashmore Group PLC (LSE: ASHM) investors received an early present. On December 24, 2025, the FTSE 250 specialist asset manager saw its stock climb approximately 2%, closing at GBX 174.20.

This move comes amidst a complex year for the emerging markets (EM) specialist, but recent data suggests a tide might be turning. Here is the analytical breakdown of why Ashmore is gaining momentum and what the latest fundamentals reveal.

Key Reasons & Drivers for the Dec 24 Surge

The ~2% uptick on Christmas Eve wasn't just holiday cheer; it was backed by specific market shifts:

Source: Kalkine Group

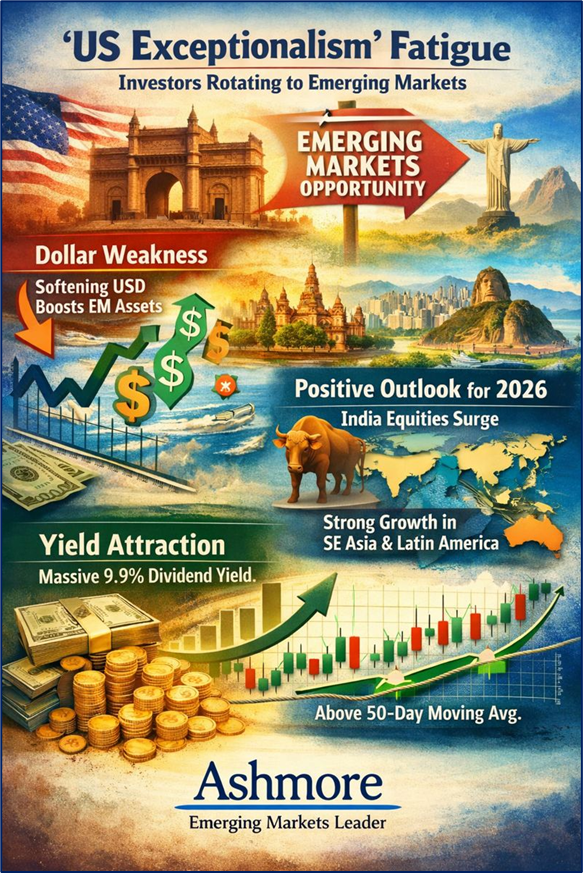

- The "US Exceptionalism" Fatigue: As we head into 2026, global investors are increasingly rotating out of "overcrowded" and high-valuation US tech stocks. Ashmore is the primary "beta play" for those moving capital into Emerging Markets.

- Dollar Weakness: A softening US Dollar in late Q4 2025 has provided a tailwind for EM local currency bonds and equities—Ashmore’s bread and butter.

- Positive Outlook for 2026: Ashmore’s recent research highlights a "Goldilocks" scenario for 2026, specifically citing a major turnaround for Indian equities and robust GDP growth in regions like Southeast Asia and Latin America.

- Yield Attraction: With a massive dividend yield of ~9.9%, income seekers are bidding up the stock as it stabilizes above its 50-day moving average.

Latest Business Model & Operational Updates

Ashmore has evolved its "Specialist EM" model to survive a period of high interest rates and geopolitical volatility.

The Evolved Business Model

Ashmore now operates on a three-phase growth strategy:

- Phase 1: Establish benchmark-driven EM themes (External/Local Debt).

- Phase 2: Diversify into Equities and Investment Grade (IG) strategies.

- Phase 3: Scale via Local Platforms (In-country offices managing local money for local clients).

Operational Highlights (FY 2025 Results)

- Assets under Management (AuM): Stood at $48.7 billion as of September 30, 2025.

- Performance: A staggering 81% of AuM is outperforming benchmarks over a 5-year period, proving the value of their active management.

- Network Expansion: In 2025, Ashmore successfully opened new offices in Qatar and Mexico, deepening its footprint in the Middle East and Latin America.

- Inflow Shifts: While institutional debt saw some outflows earlier in the year, Equities and Alternatives saw net inflows, signaling a diversification of the revenue base.

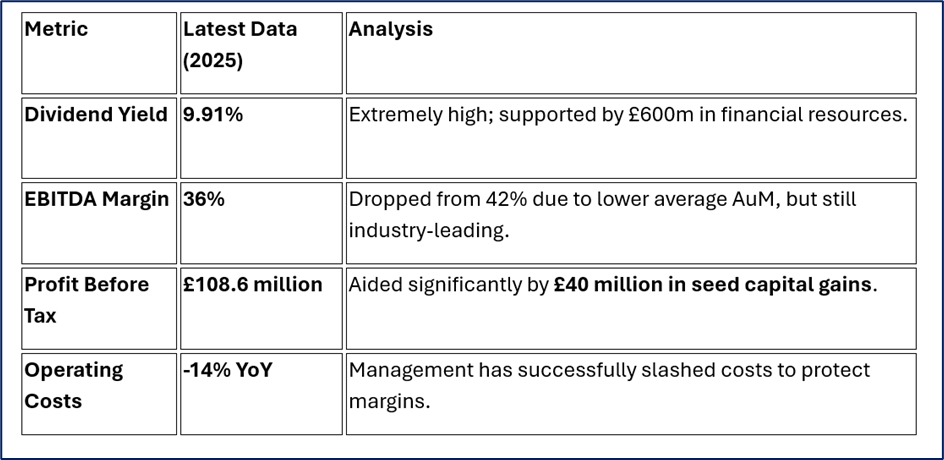

Financial Health Check

Source: Company Data

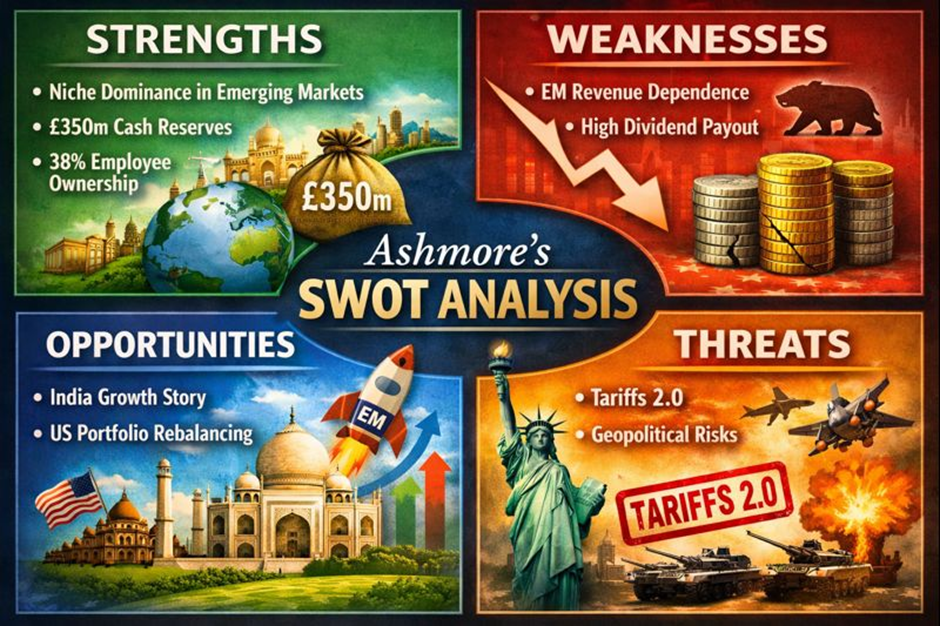

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Niche Dominance: Unrivaled brand equity in Emerging Markets.

- Liquid Balance Sheet: Over £350 million in cash allows them to seed new funds even during downturns.

- Employee Alignment: ~38% of the company is owned by employees, ensuring long-term focus.

Weaknesses

- Revenue Concentration: Still heavily reliant on EM sentiment; when EM is "out," Ashmore suffers.

- High Payout Ratio: Paying out more than earnings in dividends puts pressure on the balance sheet if AuM doesn't grow in 2026.

Opportunities

- The India Growth Story: Ashmore is heavily betting on India’s manufacturing-led GDP growth.

- US Portfolio Rebalancing: Even a 1% shift from US equities to EM could double Ashmore's AuM.

Threats

- Tariffs 2.0: Potential US trade protectionism (Trump-era policies) could hit export-heavy EMs like Vietnam and Mexico.

- Geopolitical Flares: Escalations in the Middle East or Eastern Europe remain a constant risk for EM risk appetite.

Key Risks to Watch

Investors should remain cautious of the "Dividend Trap" risk. While the 9.9% yield is enticing, the high payout ratio means any significant drop in performance fees or further AuM erosion could lead to a dividend cut in late 2026. Additionally, the Forward P/E remains elevated, suggesting the market is already pricing in a significant recovery.

Conclusion

The 2% rise on December 24 reflects a market that is starting to believe the "EM Underperformance" cycle is ending. Ashmore has trimmed its costs, expanded its local office footprint, and maintained a massive yield. If 2026 becomes the year of the "Great Rotation" from the US to Emerging Markets, Ashmore is perfectly positioned at the front of the line.

Please wait processing your request...

Please wait processing your request...