FTSE-100 Listed Endeavour Mining (LSE: EDV), the largest gold producer in West Africa, caught the eye of retail and institutional investors alike on Friday, December 19, climbing approximately 3.1%. While no single "breaking news" press release was issued on that specific morning, a convergence of macroeconomic tailwinds and solid corporate fundamentals ignited the rally.

Here is the analytical breakdown of the move, the business model, and the risks you need to know.

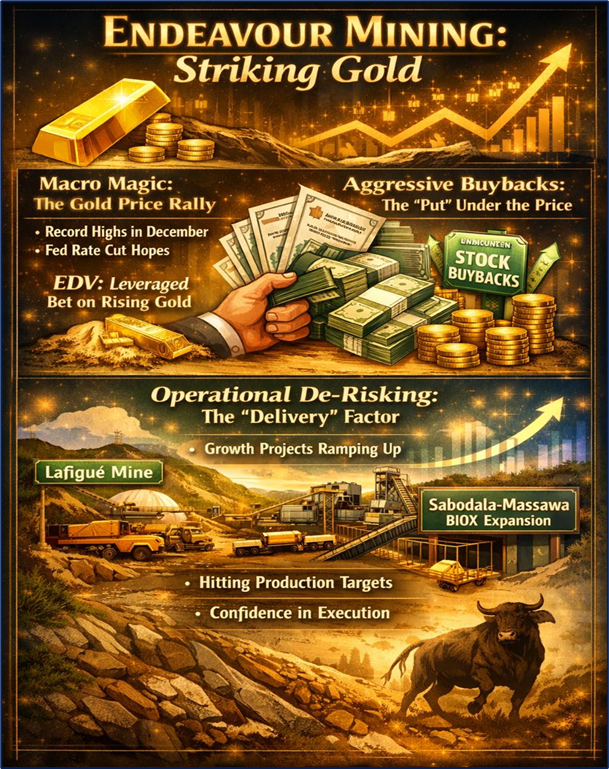

The 3 Drivers: Why the Stock Popped

Source: Kalkine Group

- Macro Magic: The Gold Price Rally

- The Catalyst: On Dec 19, gold prices pushed toward record highs, driven by softer-than-expected US inflation data. This strengthened the case for Federal Reserve rate cuts.

- The Impact: As a pure-play gold miner, EDV is a leveraged bet on the metal. When gold rises, EDV’s margins expand disproportionately, making it an immediate beneficiary of "yellow metal" momentum.

- Aggressive Share Buybacks (The "Put" Under the Price)

- The Action: Endeavour has been actively purchasing its own shares (Transactions announced mid-December).

- The Signal: Constant buying pressure from the company itself reduces the float (supply of shares) and signals management’s confidence that the stock is undervalued. This creates a "floor" that emboldens buyers.

- Operational De-Risking (The "Delivery" Factor)

- The Context: Following strong Q3 results, the market is pricing in the successful ramp-up of two major growth projects: the Lafigué mine and the Sabodala-Massawa BIOX® expansion.

- The Sentiment: Investors are moving from "wait and see" to "reward execution," confident that Endeavour will hit the top half of its annual production guidance.

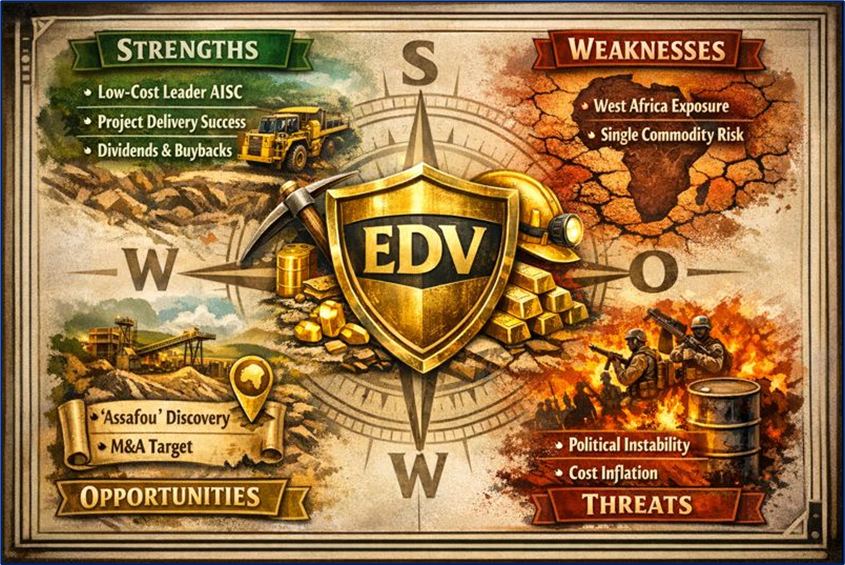

SWOT Analysis: The Strategic Snapshot

Source: Kalkine Group

Strengths (Internal Power)

- Low-Cost Leader: Industry-leading All-In Sustaining Costs (AISC) protect margins even if gold dips.

- Project Delivery: A rare track record of building mines on time and on budget (e.g., Lafigué).

- Shareholder Returns: A robust policy of dividends and buybacks that rewards patience.

Weaknesses (Internal Gaps)

- Geographic Concentration: 100% exposure to West Africa creates a lack of jurisdictional diversification compared to global peers.

- Single Commodity: Pure reliance on gold means no buffer from other metals like copper (though this is a "strength" during a gold bull run).

Opportunities (External Growth)

- The "Assafou" Giant: The Tanda-Iguela discovery in Côte d’Ivoire is potentially a Tier-1 asset that could be a massive future growth engine.

- M&A Target: As a mid-cap producer with premium assets, EDV remains an attractive takeover target for larger global majors.

Threats (External Risks)

- Regional Instability: Political volatility in Burkina Faso and Mali remains the primary discount factor applied to the stock.

- Cost Inflation: Rising fuel and consumable costs can erode the "low cost" advantage if not managed tightly.

Latest Business Updates & Model

The Business Model: "Discover, Build, Operate" Endeavour operates purely in West Africa (Senegal, Côte d’Ivoire, Burkina Faso). Their strategy is simple but hard to execute:

- Focus on High Quality: They only want assets with long mine lives (>10 years) and low costs.

- Active Management: They are not passive; they actively explore to replace reserves (finding gold costs them <$25/oz, which is exceptionally low).

- Capital Allocation: Cash flow is split between reinvesting in growth (new mines) and paying shareholders.

Recent Operational Highlights (Late 2024)

- Production: On track to produce between 1.13 – 1.26 million ounces for the full year.

- New Mines:

- Lafigué (Côte d’Ivoire): Achieved commercial production; now contributing cash flow.

- Sabodala-Massawa (Senegal): Expansion is complete, processing high-grade ore.

- Debt Reduction: Net debt leverage is healthy (well below 1.0x EBITDA), providing a fortress balance sheet.

Key Risks to Watch

- The "Sahel" Discount: Any news of coups or political unrest in the Sahel region usually triggers an knee-jerk sell-off in EDV, regardless of whether their mines are physically affected.

- Gold Price Reversal: If the Fed signals "higher for longer" rates, gold could correct, dragging EDV down with it.

Conclusion

Endeavour Mining's ~3.1% rise on December 19 was a classic case of a high-quality asset catching a macro tailwind. The company is operationally sound, hitting its targets, and buying back its own stock, all while gold prices surge. For investors, the thesis relies on being comfortable with West African geopolitical risk in exchange for superior operational returns and dividend yields.

Verdict: The stock is currently trading on "execution confidence" + "gold price strength."

Source: Trading View, 19 December 2025

Please wait processing your request...

Please wait processing your request...