The final trading session of 2025 delivered a major win for Europa Oil & Gas (Holdings) PLC (LSE: EOG). While the broader oil market faced a volatile year-end, Europa's shares surged approximately 17% on December 31, 2025, following a sequence of high-impact operational updates.

The 17% Catalyst: Why the Stock Jumped

Source: Kalkine Group

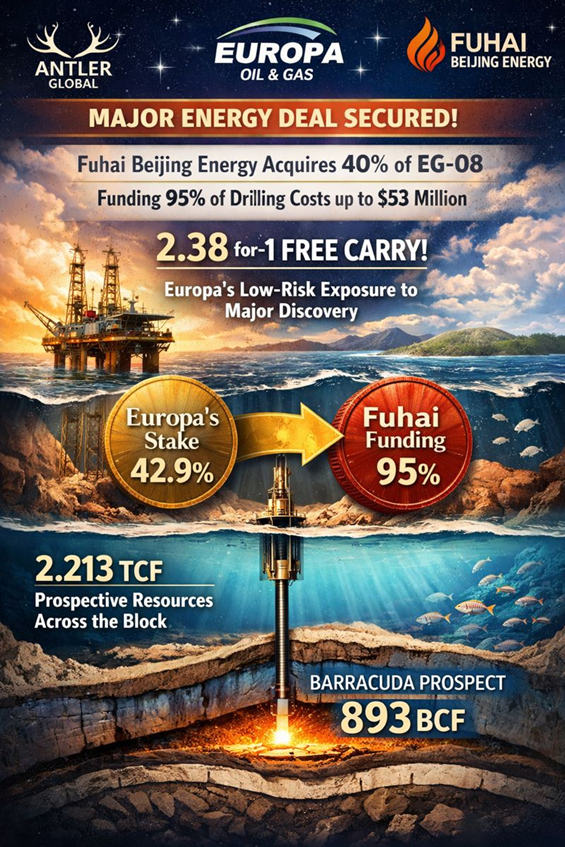

The primary driver behind the double-digit surge was the formal signing of a binding Farm-out Agreement (FOA) for the EG-08 license in Equatorial Guinea, announced just 24 hours prior.

- The Deal: Europa’s partner, Antler Global, secured a deal with Fuhai Beijing Energy. Fuhai will acquire a 40% interest in EG-08 by funding 95% of the costs for the upcoming Barracuda exploration well, up to a $53 million cap.

- The "Free Carry": For Europa (which holds a 42.9% stake in Antler), this represents a massive "de-risking." The company is essentially getting a 2.38-for-1 carry, meaning they gain exposure to a massive potential discovery with minimal capital expenditure.

- The Resource Potential: Updated geophysical analysis identifies 2.213 trillion cubic feet (TCF) of prospective resources across the block, with the primary Barracuda prospect estimated at 893 billion cubic feet (BCF).

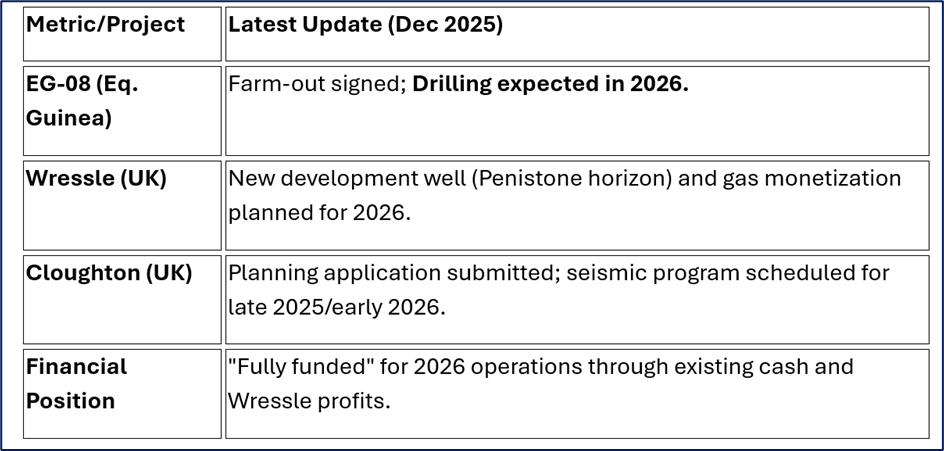

Business Model & Strategy (2026 Update)

Europa has pivoted toward a "Balanced Portfolio" model designed to survive energy transition pressures while capturing high-upside exploration wins.

- Core Production (The Cash Cow): Revenue is underpinned by UK onshore assets, specifically the Wressle field. Wressle continues to produce at the top end of forecasts, providing the "rent" money for the company.

- Appraisal & Gas-Weighting: The company is shifting heavily toward gas, viewed as a "transition fuel." Key projects include the Cloughton appraisal (UK) and Inishkea West (Ireland).

- Low-Cost Exploration: By using the "Farm-out" model (bringing in partners to pay for drilling), Europa maintains a high-reward profile in West Africa without betting the entire company's balance sheet on a single "dry hole."

Financial & Operational Snapshot

Source: Company Data

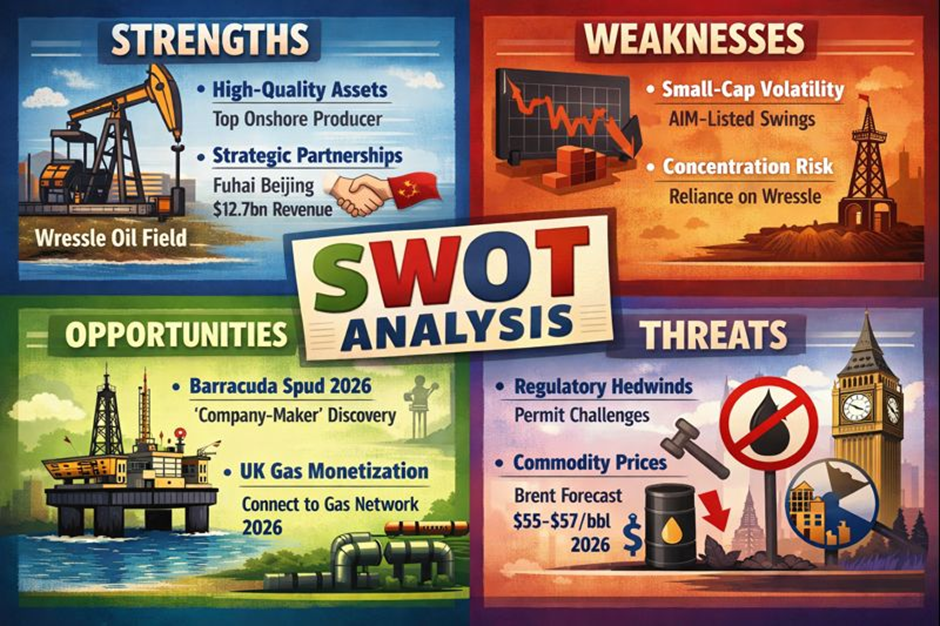

SWOT Analysis

Source: Kalkine Group

Strengths

- High-Quality Assets: Wressle is one of the most productive onshore fields in the UK.

- Strategic Partnerships: The deal with Fuhai Beijing brings in a partner with deep pockets ($12.7bn 2024 revenue).

- Insider Alignment: Insiders own ~14% of the company, showing skin in the game.

Weaknesses

- Small-Cap Volatility: As an AIM-listed stock, liquidity can be thin, leading to sharp price swings.

- Concentration Risk: Heavy reliance on Wressle for immediate cash flow.

Opportunities

- Barracuda Spud (2026): A discovery at the 893 BCF Barracuda prospect would be a "company-maker."

- UK Gas Monetization: Connecting Wressle to the local gas network could materially increase revenues in 2026.

Threats

- Regulatory Headwinds: The UK government’s stance on new oil/gas permits remains a constant friction point.

- Commodity Prices: Brent crude is forecast to average $55–$57/bbl in 2026 due to global oversupply, which may squeeze margins.

Key Risks to Watch

While the 17% jump is a vote of confidence, investors should monitor:

- Approval Risk: The Equatorial Guinea deal still requires final Ministry (MMHD) and Chinese ODI approvals.

- Drilling Delays: Offshore exploration is notorious for technical delays and cost overruns.

- Global Glut: A projected 2 million barrel-per-day surplus in 2026 could keep a "ceiling" on energy stock valuations regardless of operational success.

Conclusion

The year-end rally in Europa Oil & Gas reflects a fundamental shift from "hope" to "funded execution." By securing a heavyweight partner for the Barracuda well, Europa has transformed 2026 into a "pivotal" year where the drill bit—rather than the balance sheet—will decide its valuation.

Please wait processing your request...

Please wait processing your request...