Experian (LSE: EXPN) kicked off the first full trading week of 2026 with a notable 3% jump on January 5th. While the broader FTSE 100 saw moderate movement, Experian’s outperformance signals a renewed retail and institutional appetite for "data-as-infrastructure."

This surge isn't just a market fluke; it is the culmination of a strategic pivot toward AI-integrated financial services and a robust upward revision in growth guidance.

Why Experian is Surging: Key Drivers on Jan 5, 2026

Source: Kalkine Group

The 3% uptick is driven by a "perfect storm" of positive sentiment and fundamental upgrades:

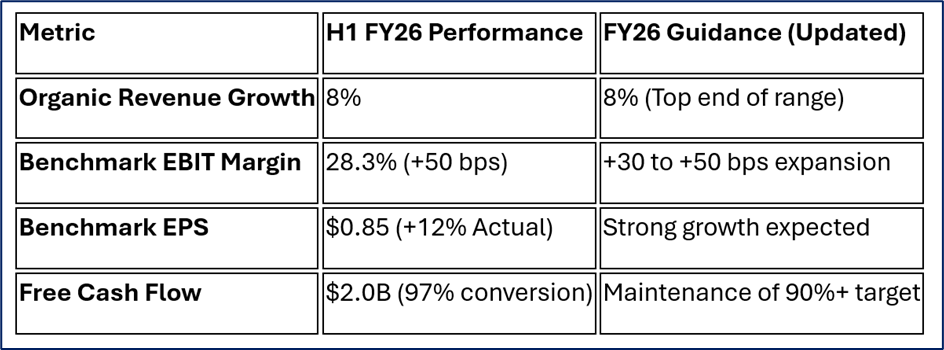

- Guidance Upgrades: In its most recent updates leading into 2026, Experian raised its FY26 organic revenue growth expectations to the top end of its range (8%), with total revenue growth projected at 11%.

- The "AI Winner" Tag: JPMorgan recently reinstated coverage with an "Overweight" rating, specifically labeling Experian an "AI winner." The market is now pricing in the efficiency gains from Experian’s AI-driven automation, which is already expanding margins by 30–50 basis points.

- Dividend Magnet: With the ex-dividend date fast approaching (January 8, 2026) for a 21.25 US cent interim payment (a 10% increase), "dividend capture" buying has likely provided a short-term floor for the price.

- Resilient Verticals: While the UK mortgage market remains sensitive, Experian’s diversification into Healthcare and Automotive data has shielded it from the volatility of traditional credit cycles.

The 2026 Business Model: From Credit Bureau to AI Powerhouse

Experian has successfully transitioned from a passive credit reporting agency into a proactive Data & Technology Platform.

- The "Ascend" Ecosystem

The core of the latest business model is the Experian Ascend platform. It allows financial institutions to build, test, and deploy credit models in days rather than months. By integrating proprietary data with real-time analytics, Experian has become an indispensable "toll booth" for the global lending economy.

- Direct-to-Consumer (D2C) Monetization

With over 208 million free members, Experian is no longer just selling data to banks. It is a fintech giant in its own right, offering "Experian Boost," identity theft protection, and personalized marketplace lending. In 2026, this segment is a major organic growth driver, growing at 9% YoY.

- Vertical Expansion: Healthcare & Fraud

The 2026 model heavily emphasizes Experian Health. As US healthcare regulations (like the OBBBA) increase billing complexity, Experian’s AI tools for claim denials and patient eligibility have become high-margin "must-haves" for hospitals.

Latest Financial & Operational Pulse

Source: Company Data

Operational Highlights:

- ClearSale Integration: The acquisition of ClearSale (completed April 2025) has supercharged Experian’s fraud prevention capabilities in Latin America.

- Latin America Momentum: Brazil remains a powerhouse, with double-digit growth as credit penetration in the region matures.

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Unrivaled Data Moat: Possession of credit histories for over 1 billion people and businesses globally.

- High Switching Costs: Banks and hospitals cannot easily swap out the data infrastructure integrated into their lending and billing workflows.

- Strong Cash Flow: A 90%+ cash conversion rate allows for consistent R&D and dividend growth.

Weaknesses

- Premium Valuation: Trading at a P/E of ~30x, the stock is priced for perfection, leaving little room for earnings misses.

- Regional Imbalance: While Latin America and North America are booming, the UK and Ireland regions show slower growth (1%) due to local macro-pressures.

Opportunities

- Generative AI: Using GenAI to provide "financial coaching" to consumers, further increasing retention in the D2C app.

- Open Banking: As global regulations move toward open data, Experian is positioned to aggregate and verify non-traditional data (utilities, rent).

Threats

- Cybersecurity Risks: As a prime target for state-sponsored and AI-driven cyberattacks, any data breach would be catastrophic for brand equity.

- Regulatory Scrutiny: Increased "Buy Now, Pay Later" (BNPL) regulations and data privacy laws (GDPR/CCPA) could increase compliance costs.

The Risk Landscape: What Could Go Wrong?

Despite the 3% rally, investors remain watchful of two primary risks:

- The "AI Arms Race": While AI helps Experian, it also helps fraudsters. Experian’s own 2026 Data Breach Forecast warns that AI-driven synthetic identities could become indistinguishable from real people, necessitating constant, expensive R&D.

- Interest Rate Volatility: If central banks hold rates higher for longer in 2026, mortgage volumes (a key B2B driver) could remain suppressed, capping the upside for the North American segment.

Conclusion

Experian’s 3% jump on January 5, 2026, reflects a market that is finally rewarding the company’s transition from a "legacy bureau" to a "high-growth tech platform." With revenue hitting the top end of guidance and AI-driven margins expanding, the company has successfully decoupled its performance from the broader sluggishness of some European markets.

For the retail observer, the story isn't just about credit scores—it’s about who owns the "digital truth" in an AI-driven economy.

Please wait processing your request...

Please wait processing your request...