The Mega-Deal: Breaking Down Today's Surge

FirstGroup plc (LSE: FGP) is trading significantly higher today, up approximately 6%, following a major announcement that has reignited investor confidence.

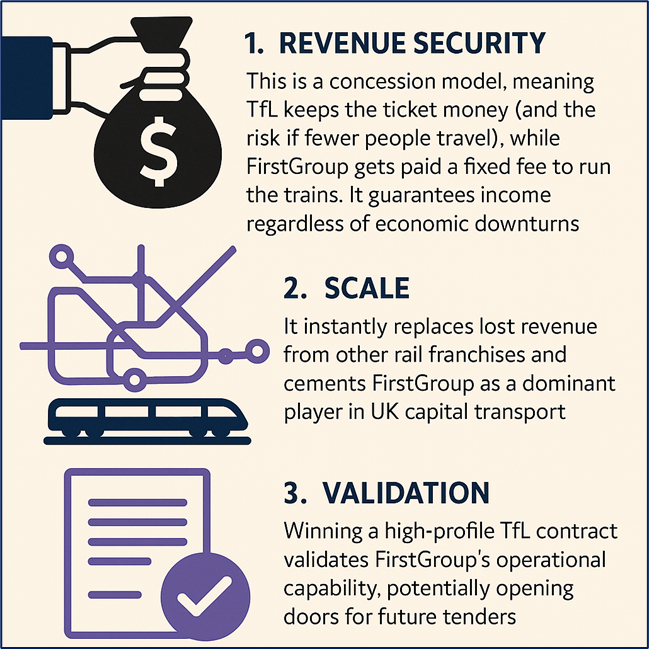

The Catalyst: On Wednesday, December 10, 2025, FirstGroup announced it has won the massive £3 billion contract to operate the London Overground network.

- The Client: Transport for London (TfL).

- The Value: ~£3 billion over 8 years (plus a 2-year extension option).

- The Start Date: May 2026.

- The Scope: Taking over from Arriva to run one of London’s busiest networks (4 million passengers/week).

Why The Market Loves This Deal

This isn't just "another contract." It is a strategic game-changer for three reasons:

Source: Kalkine Group

The Business Model: How FirstGroup Makes Money

FirstGroup is a public transport giant operating in two main divisions. The key to understanding the stock is seeing how they are de-risking their income.

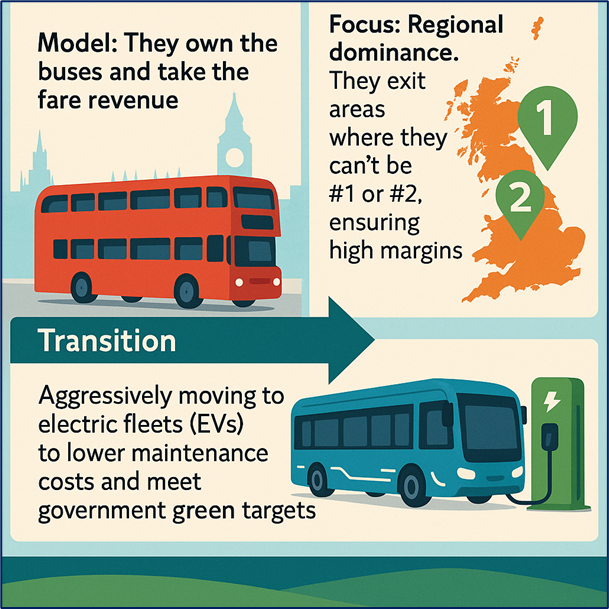

- First Bus (The Cash Cow)

- Scale: One of the UK’s largest bus operators, serving 25% of the population.

- Model: They own the buses and take the fare revenue.

- Focus: Regional dominance. They exit areas where they can't be #1 or #2, ensuring high margins.

- Transition: Aggressively moving to electric fleets (EVs) to lower maintenance costs and meet government green targets.

Source: Kalkine Group

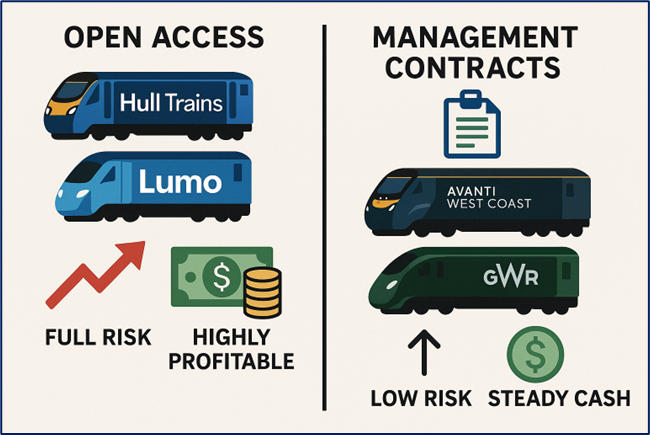

- First Rail (The Growth Engine)

- Open Access: They run "Hull Trains" and "Lumo" (London-Edinburgh). Here, they take full risk but keep all profits. These are highly profitable.

- Management Contracts: They run lines like Avanti West Coast and Great Western Railway (GWR) for the government. They get a fixed management fee. The new London Overground deal fits here—low risk, steady cash.

Source: Kalkine Group

Latest Business Updates (Dec 2025)

Beyond today's £3bn win, here is the snapshot of their recent health:

- H1 Earnings (Nov 2025): Reported a robust profit increase, driven by acquisitions and "Open Access" rail performance.

- Bus Volumes: A slight dip in regional bus passenger numbers was flagged in November (down ~4%), which had previously depressed the stock. Today’s news reverses that sentiment.

- Share Buybacks: The company recently completed a £50m share buyback, proving they are committed to returning cash to shareholders.

- Dividends: The interim dividend was hiked by ~30% recently, signaling management confidence in cash flow.

The Risks: What Could Go Wrong?

Despite the green arrows, FirstGroup operates in a tough sector.

- Political Risk (Nationalization): The UK Labour government has ambitions to bring rail into public ownership. While "concessions" like the Overground are safer, the broader rail portfolio faces policy uncertainty.

- Industrial Action: Strikes have plagued UK rail for years. While the Overground deal mitigates revenue risk, strikes still damage the brand and incur performance penalties.

- Cost Inflation: High energy prices and wage increases for drivers put pressure on margins, particularly in the Bus division where they can't always pass costs to passengers.

Strategy: The "De-Risking" Playbook

FirstGroup’s strategy is clear: Minimize Risk, Maximize Cash Flow.

- Pivot to Fixed-Fee Rail: By chasing contracts like the London Overground, they avoid the danger of "passenger collapse" (like during COVID). They want steady, boring, reliable fees.

- Electrification: Investing heavily in electric buses to reduce long-term operating costs and secure government subsidies.

- Shareholder Returns: Using excess cash to buy back shares and pay dividends, keeping the stock attractive to income investors.

Outlook: Is This the Turning Point?

- Short Term: The Overground win removes a major overhang ("Can they replace lost rail contracts?"). Expect positive momentum.

- Long Term: If they can stabilize Bus passenger volumes and successfully launch the Overground service in 2026, the stock is positioned as a high-yield, low-volatility infrastructure play.

Conclusion

FirstGroup is up 6% today because it proved it can win massive, secure government contracts. By locking in £3 billion of revenue for the next decade, it has significantly reduced its risk profile. For investors, FGP is transforming from a volatile travel stock into a steady infrastructure utility—but the shadow of nationalization and labor strikes remains the primary caution.

Source: Trading View, 10 December 2025, 11:50 AM GMT

Please wait processing your request...

Please wait processing your request...