The FTSE has a new star of the day. On December 23, 2025, shares of XAAR PLC (LSE: XAR) surged by approximately 6.7%, closing at roughly GBX 105.50. For a small-cap stock that has navigated a choppy 2025, this pre-Christmas rally isn't just festive cheer—it’s a signal of shifting investor sentiment toward Xaar’s "High Viscosity" future.

Here is the deep dive into why XAAR is moving, the mechanics of its new business model, and whether this momentum can carry into 2026.

The Dec 23 Surge: Key Drivers

The 6% jump was fueled by a "perfect storm" of fundamental validation and technical recovery:

Source: Kalkine Group

- Jewellery Wax Dominance: Recent data confirmed that Xaar's partnership with Flashforge (the Waxjet 530) has captured significant market share ahead of schedule. Revenue in this niche grew from £0.6m to £3.3m in H1 2025—a massive 450% increase.

- Short-Covering & Low Liquidity: As a small-cap with a £81m market cap, Xaar can move quickly on thin holiday volumes. With the stock recently trading below its 200-day moving average (123p), contrarian buyers stepped in, sensing an "oversold" opportunity.

- Berenberg's Bullish Echo: The market is finally pricing in the "Buy" initiation from Berenberg (target price 160p), which highlighted Xaar as a prime turnaround play.

- Operational Stability: After a "mixed" 2024, the H2 2025 order book in the EPS (Engineered Print Systems) division began to show signs of rebuilding, easing fears of further profit warnings.

Latest Business Model: Beyond Just Printheads

Xaar has evolved from a simple component manufacturer into a vertically integrated inkjet solutions group. Its 2025 model rests on four pillars:

- The "Ultra High Viscosity" Moat: Unlike competitors (Epson, Ricoh) that jet thin liquids, Xaar jets fluids up to 100 centipoise (cP). This allows it to print functional fluids like 3D resins, glues, and heavy paints.

- Direct-to-Market Systems: Through its EPS and Megnajet subsidiaries, Xaar doesn't just sell the "engine" (the printhead); it sells the entire "car" (the printing system and fluid management).

- Segment Diversification:

- Core: Ceramics and Glass (stabilizing).

- Growth: Packaging, Textiles, and Labels.

- Moonshots: EV Battery coating and 2.5D/3D printing.

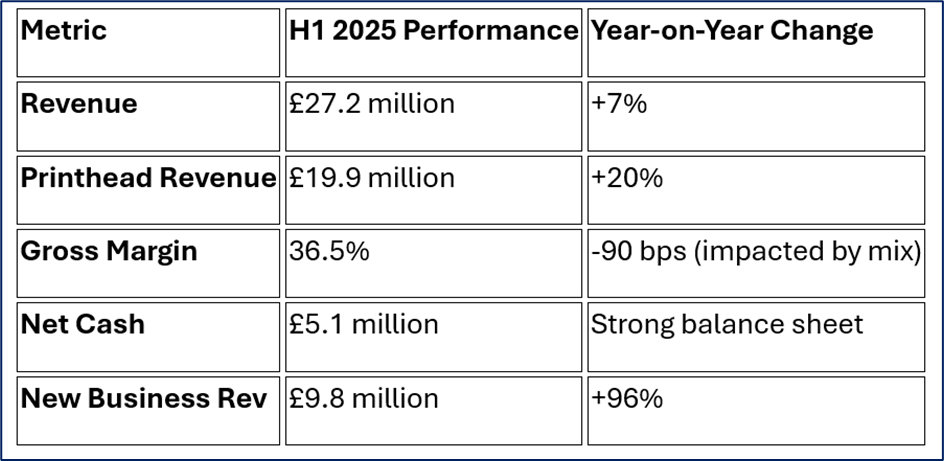

2025 Financial & Operational Snapshot

Source: Company Data

Operational Highlights:

- EV Battery Breakthrough: Xaar’s technology is now being used for insulation coating on 800V EV platforms, replacing traditional film with more efficient inkjet spray.

- Sustainability Push: Switched 100% of UK operations to green gas, reducing Scope 1 emissions by 60%.

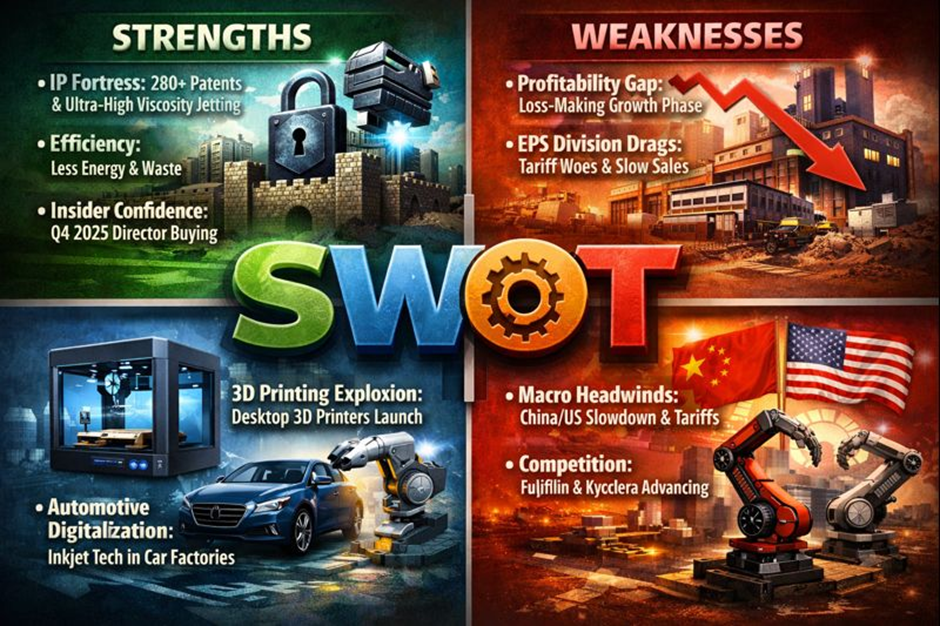

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- IP Fortress: 280+ patents and a monopoly on ultra-high viscosity jetting.

- Efficiency: Digital printing uses less energy and creates less waste than traditional analog methods.

- Insider Confidence: Notable director/PDMR buying reported throughout Q4 2025.

Weaknesses

- Profitability Gap: The company remains in a "loss-making growth phase" as it scales.

- EPS Division Drags: US-based EPS has struggled with tariff uncertainty and a slow sales cycle.

Opportunities

- 3D Printing Explosion: The launch of desktop 3D printers using Xaar tech could democratize high-end manufacturing.

- Automotive Digitalization: Replacing masks and sprays with inkjet in car factories represents a multi-billion pound TAM.

Threats

- Macro Headwinds: Tariffs and industrial slowdowns in China/US could delay OEM product launches.

- Competition: Giants like Fujifilm and Kyocera are aggressively moving into industrial segments.

Key Risks to Watch

- Tariff Exposure: Significant operations in the US and China make Xaar sensitive to trade war rhetoric.

- Adoption Rate: If the transition from "Analog to Digital" in the automotive sector stalls, Xaar’s medium-term targets will be missed.

- Cash Burn: While net cash is £5.1m, continued R&D investment (c.7% of revenue) requires the company to hit profitability by 2027 to avoid further Dilution.

Conclusion

Xaar’s 6% rise on December 23 is more than a "dead cat bounce." It reflects a growing realization that the company’s pivot toward high-margin, high-viscosity applications like jewellery wax and EV coatings is working. While the group is still fighting for bottom-line profitability, the top-line growth in "New Business" (+96%) suggests the technology is finally finding its market fit.

Source: Trading View, 23 December 2025

Please wait processing your request...

Please wait processing your request...