ACG Metals (LON: ACG): 27,350% Surge or Strategic Reset? The 2026 Verdict

The meteoric rise of ACG Metals over the last 12 months—clocking in at an astronomical percentage gain—is a phenomenon largely driven by its transition from a Special Purpose Acquisition Company (SPAC) to a full-scale producer following the acquisition of the Gediktepe Mine in Turkey.

The stock is no longer a speculative shell; it is a cash-generating mining entity in the midst of a transformational shift from gold to copper.

Latest Key Reasons and Drivers as of 20 Jan 2026

Source: Kalkine Group

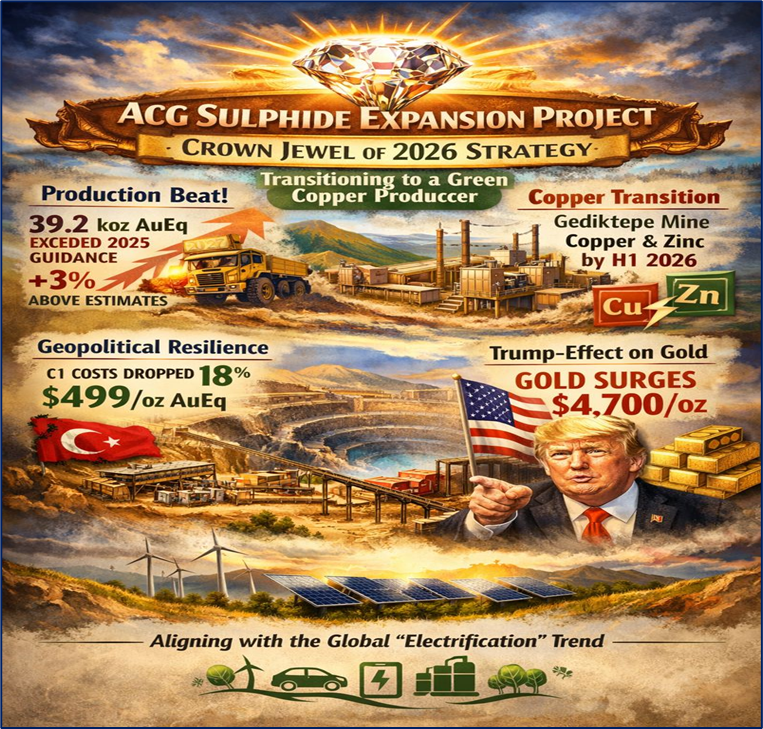

The primary catalyst for the current price action is the Sulphide Expansion Project, which is the "crown jewel" of the company’s 2026 strategy. Investors are pricing in the shift from being a precious metals player to a critical "green transition" copper producer.

- Production Beat: As of yesterday's update (Jan 19), ACG exceeded its 2025 production guidance, delivering 39.2 koz AuEq, which was 3% above the top-end estimates.

- Copper Transition: The Gediktepe mine is transitioning to copper/zinc production by the end of H1 2026. This move aligns the company with global "electrification" tailwinds.

- Geopolitical Resilience: Despite being based in Turkey, the mine has shown exceptional cost control, with C1 cash costs dropping 18% year-on-year to $499/oz AuEq.

- Trump-Effect on Gold: Renewed tariff threats from the U.S. administration have pushed gold prices above $4,700/oz, providing a massive cash-flow cushion while the copper plant is under construction.

Current Price & Technical Analysis (20 Jan 2026)

As of today, January 20, 2026, ACG is trading at approximately 1,400p, up nearly 4% in today's session following a strong operational update.

- Momentum: The stock has hit a new 52-week high of 1,400p today. Technologically, the stock is in a "blue sky" breakout phase, having cleared the previous resistance level of 1,350p.

- RSI and Moving Averages: The 14-day Relative Strength Index (RSI) is hovering near 75, suggesting the stock is entering overbought territory, which may lead to short-term consolidation. However, the stock remains comfortably above its 50-day and 200-day moving averages, signaling a robust primary uptrend.

- Volume: Trading volume has spiked significantly over the last 48 hours, confirming institutional accumulation following the production beat.

Latest Analyst Upgrades, Downgrades & Valuation

The "Smart Money" remains heavily biased toward the upside. On January 7, 2026, Canaccord Genuity named ACG Metals their "Top Mining Pick for 2026."

- Consensus Rating: "Buy" (based on major brokers including Berenberg and Canaccord).

- Price Targets: Analysts have a consensus target of 1,845p, with some aggressive targets reaching 1,950p. This implies an upside of roughly 35-40% from today’s price.

- Valuation: The stock currently trades at a P/E ratio of ~88x based on trailing earnings, but forward multiples are much lower as the copper production comes online in late 2026. It currently carries a Price/Book ratio of 4.3x.

Business Model and Financial Update

ACG Metals operates a "Roll-up and Consolidate" model. They acquire mid-tier copper and gold assets with strong ESG credentials and optimize them through technical expertise.

- Current Asset: 100% ownership of the Gediktepe Mine in Turkey.

- Net Debt: Reported at $65 million as of Dec 31, 2025, with a healthy cash balance of $144 million (including restricted sulphide project funds).

- Dividend Status: There is currently no dividend. The company is in a "Growth/Capex" phase, reinvesting every dollar into the Sulphide Expansion and Enriched Ore Treatment projects.

2026 Outlook and Risks

The guidance for 2026 is "Transformational." ACG expects to produce 20,000 to 22,000 tonnes of Copper Equivalent (CuEq) this year.

- Guidance: AISC (All-In Sustaining Costs) are projected at $2.40 to $2.60 per pound of CuEq.

- Risks: * Execution Risk: Any delay in the H1 2026 commissioning of the sulphide plant would be punished by the market.

- Commodity Volatility: While gold is high, a sudden drop in copper prices would hurt the 2027 revenue outlook.

- Single-Asset Risk: Until ACG makes its next acquisition, it remains highly sensitive to local Turkish regulations and the single-mine performance.

Conclusion

Is it still a buy? While the 27,350% surge represents the transition from a SPAC to a producer, the current valuation suggests that the "Copper Story" is only just beginning. For investors looking for exposure to the green energy transition through a high-margin, low-cost producer, ACG remains a high-conviction growth play, though technical indicators suggest waiting for a slight dip below 1,350p might offer a better entry.

Please wait processing your request...

Please wait processing your request...