As of January 20, 2026, WPP PLC (LSE: WPP) presents one of the most polarizing "Value vs. Trap" debates in the FTSE universe. Trading near a multi-year trough of 315p after a brutal 58% slide over the past year, the global advertising titan now dangles a massive 10.1% dividend yield—a figure so high it typically signals a market that has already priced in a significant dividend cut.

With new CEO Cindy Rose characterizing recent performance as "unacceptable" and leading a McKinsey-backed radical reset to combat AI disruption and client in-housing, WPP is no longer a blue-chip stabilizer but a high-stakes turnaround play.

For income seekers, the yield is "juicy" but dangerous, covered by cash flow but technically insolvent on an earnings basis (114% payout ratio). Smart money remains defensive, as the stock’s recent exit from the FTSE 100 underscores a collapse in institutional confidence that only a proven reversal in organic growth can fix.

Latest Key Reasons & Today’s Drivers (Jan 20, 2026)

Source: Kalkine Group

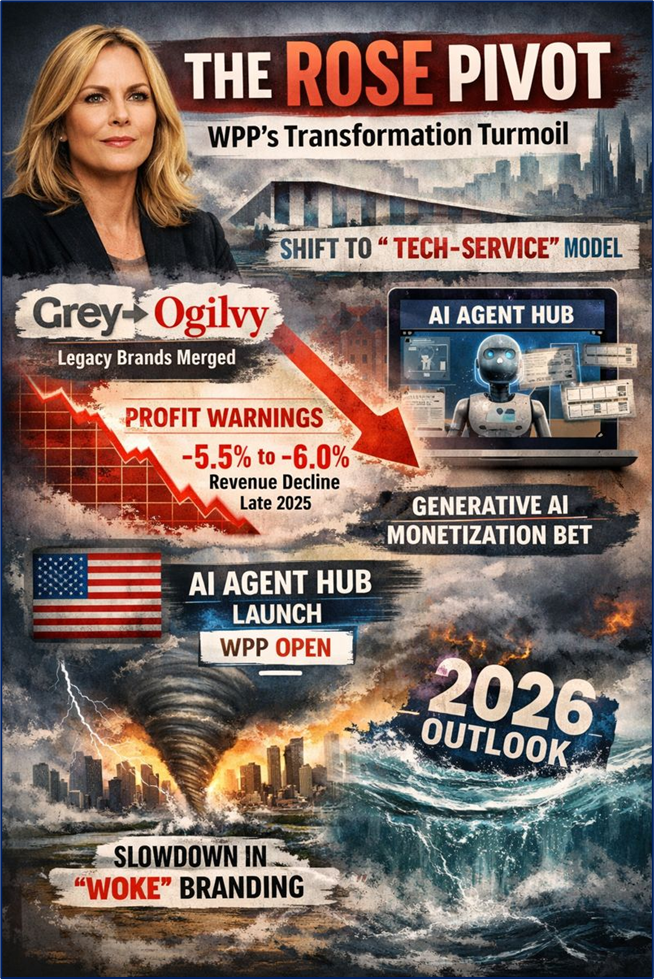

The primary driver of the current price action is the "Rose Pivot." CEO Cindy Rose has officially shifted WPP from a traditional agency holding group to a "Tech-Service" model, merging legacy brands like Grey into Ogilvy to streamline a bloated cost base.

Current sentiment is weighed down by two profit warnings in late 2025, which saw like-for-like revenue guidance slashed to a contraction of -5.5% to -6.0%.

Operationally, today’s market is reacting to the "AI Agent Hub" launch on WPP Open, which is WPP’s attempt to prove it can monetize Generative AI rather than be replaced by it.

Macro factors including US tariffs and a general slowdown in "woke" branding budgets (impacting CPG clients) have created a perfect storm for the 2026 outlook.

Current Price Technical Analysis (Jan 20, 2026)

Source: Trading View

WPP is currently locked in a sustained bearish channel, trading at 315.60p, which is barely 18% above its 52-week low of 266p.

The stock is currently trading below its 200-day Moving Average (422p) and is struggling to hold above its 50-day MA (314p), suggesting that the long-term trend remains firmly down. The Relative Strength Index (RSI) is hovering near 40,

Major resistance is sitting at the 350p - 363p zone, while a break below the 266p support level would likely trigger a fresh wave of institutional selling.

Latest Analyst Upgrades & Downgrades

The consensus remains "Hold/Neutral" as analysts wait for evidence of stabilization in the 2026 guidance.

Citi recently reaffirmed a "Neutral" rating (Jan 14, 2026) with a target of 365p, citing a lack of near-term catalysts despite the low valuation.

Morgan Stanley maintains a "Hold" with a 350p target, warning that equities sales and trading professionals see continued weakness in media spend for H1 2026.

Deutsche Bank remains one of the few "Buy" outliers with a target of 510p, betting on a massive re-rating if the AI integration successfully lowers production costs.

Business Model & Operational Update (As of Today)

WPP has moved away from the "service bureau" model. It now operates as an integrated platform where half of all new pitches involve cross-disciplinary teams (Creative, Media, Data, AI).

The workforce has been reduced by over 7,000 employees in the last 12 months, shifting the balance from "traditional creatives" to software engineers and data scientists.

A major focus is WPP Media (formerly GroupM), which is being repositioned as an AI-enabled media buying powerhouse to compete with digital-native firms.

Strategic wins in early 2026 include Mastercard and Reckitt, though these are offset by the massive loss of the Mars global media account in mid-2025.

Latest Current Dividend Analysis

The dividend yield is currently 10.11%, which is more than double the FTSE 100 average.

The Payout Ratio stands at 113.87%, meaning WPP is paying out more in dividends than it is earning in statutory profits—this is the definition of an unsustainable dividend.

However, the company’s Free Cash Flow of £716 million provides a temporary "liquidity bridge" to maintain payments through 2026.

Smart money expects a dividend rebasing (cut) in late 2026 if revenue does not return to growth, as the firm needs to preserve capital for its AI "mission."

Latest Valuation as of Today

WPP is objectively undervalued on a Price-to-Book basis, trading at 0.84x P/B, meaning you are buying the assets for less than their accounting value.

The Forward P/E ratio is a complex 9.1x, appearing cheap compared to historical averages but reflecting the "decline premium" the market is currently applying.

Compared to peers like Publicis, WPP is trading at a 40% discount, reflecting its slower transition to digital and higher debt-to-equity leverage (215%).

Outlook, Guidance & Risks

Outlook: 2026 is officially a "Reset Year." Management has deferred pay reviews to May 2026 to preserve cash.

Guidance: Anticipated revenue growth for 2026 remains flat at best (0% to +1%), with the real recovery pushed to 2027.

Major Risks: The primary risk is AI Disintermediation—if clients find they can generate high-quality ads for 1% of the cost using in-house tools, WPP’s scale becomes a liability rather than an asset. Additionally, high debt levels in a "higher-for-longer" interest rate environment remain a drag on earnings.

Conclusion

WPP is a classic value play for the brave. It is fundamentally undervalued and offers a "juicy" yield, but the yield carries a high risk of being cut to fund the necessary technological pivot. It is currently a "Show Me" story; until the new CEO can prove that AI is a tool for WPP's growth rather than its replacement, the stock will likely remain a laggard.

Please wait processing your request...

Please wait processing your request...