_12_29_2025_06_37_56_429947.jpg)

On December 24, 2025, while most of the market was winding down for the festive break, Morgan Advanced Materials (LSE: MGAM) caught the eye of retail and institutional investors alike, closing up 1.41% at GBX 216.50.

For a stock that has navigated a turbulent 2025—marked by semiconductor destocking and a strategic "pivot" under new leadership—this Christmas Eve nudge signals more than just low-volume holiday trading. It reflects a growing market consensus that the company's "simplification" story is finally taking root.

The Christmas Rally: Key Drivers & Latest Updates

The 1.4% uptick on the final trading day before Christmas can be attributed to several converging factors:

Source: Kalkine Group

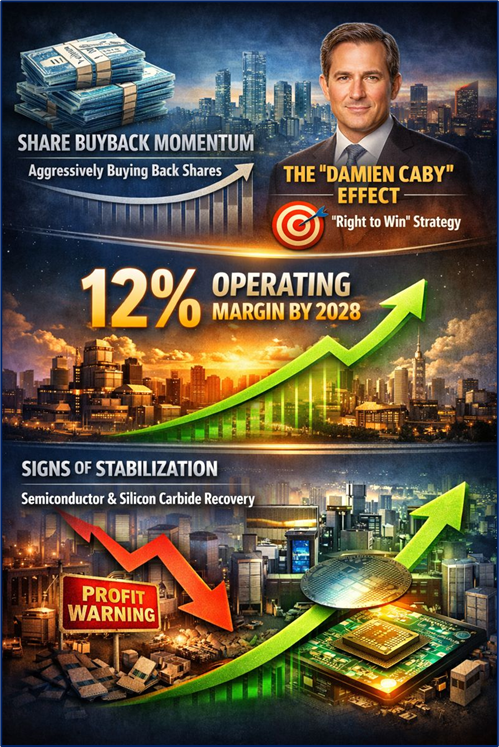

- Share Buyback Momentum: Recent RNS filings (Regulatory News Service) on December 23 and 24 confirmed that the company is actively executing its transaction in own shares. By aggressively buying back its own stock, Morgan is providing a "floor" for the share price and signaling confidence in its undervalued status.

- The "Damien Caby" Effect: Since taking the helm, CEO Damien Caby has transitioned the company from a "growth-at-all-costs" mindset to a "Right to Win" strategy. Investors are warming to the pragmatic December 4th strategy update, which prioritized 12% operating margins by 2028.

- Signs of Stabilization: Following a profit warning in October (where margins were revised down to ~10% for 2025), recent data suggests that the "de-stocking" in the semiconductor and silicon carbide markets—which hammered the stock earlier this year—is finally bottoming out.

The 2025 Business Model: Not Your Grandfather’s Industrial

Morgan has shed its image as a traditional brick-and-mortar manufacturer. The latest business model is built on Agility and Customer Intimacy, categorized into three distinct pillars:

- Thermal Products: High-temperature insulation for energy-intensive industries.

- Performance Carbon: Critical components for rail, aerospace, and clean energy.

- Technical Ceramics: The "high-tech" engine room, providing precision parts for medical equipment and semiconductor manufacturing.

The Pivot: The company is moving away from being a "generalist" provider. It is now focusing on Strategic Mandates—divesting lower-margin businesses (like the recent sale of the Molten Metal Systems business) and doubling down on sectors where they have a technical monopoly.

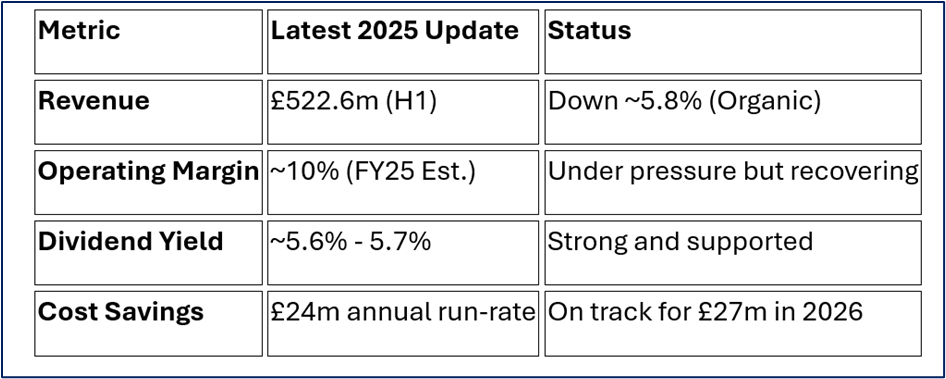

Latest Financial & Operational Health Check

Morgan’s 2025 has been a year of "pruning for growth."

Source: Company Data

Operational Highlights: * Semiconductor Capacity: The massive investment in silicon carbide capacity is now "substantially complete." This means the heavy capital expenditure (CapEx) phase is ending, paving the way for better Free Cash Flow in 2026.

- Simplification Program: The company is on track to hit its goal of returning to a 12.5% margin in the near term by closing underperforming sites and streamlining its global supply chain.

SWOT Analysis

Source: Kalkine Group

Strengths

- Technical Moats: 160 years of material science expertise makes their products difficult to replicate.

- Global Footprint: Manufacturing in 18 countries provides a natural hedge against localized economic downturns.

- Dividend Reliability: A 5%+ yield is highly attractive in a FTSE 250 context, supported by a strong balance sheet.

Weaknesses

- Legacy Systems: Ongoing costs associated with upgrading IT infrastructure and recovering from past cyber-security incidents.

- Margin Volatility: Exposure to cyclical markets (metals, industrial) makes earnings "lumpy."

Opportunities

- The Energy Transition: Growing demand for thermal management in EVs and green hydrogen.

- Aerospace & Defense: A secular bull market in defense spending is boosting their Technical Ceramics division.

- Portfolio Pruning: Further divestments of "non-core" assets could unlock significant cash for M&A or higher dividends.

Threats

- Geopolitical Friction: Trade tensions with China (a key market) remain a persistent risk.

- Slow Semi Recovery: If the semiconductor rebound stalls in 2026, the newly built capacity could sit idle, dragging on ROIC (Return on Invested Capital).

Critical Risks to Watch

Despite the optimistic end to the year, investors should keep a close eye on:

- FX Headwinds: As a global exporter, a strengthening GBP can eat into reported profits.

- Input Costs: While inflation is cooling, the price of specialized minerals and energy remains volatile.

- Execution Risk: The CEO’s "2028 Strategy" is ambitious. Any delay in the £27m savings target will likely be punished by the market.

Conclusion

Morgan Advanced Materials is currently a "show-me" story. The 1.4% rise on December 24 suggests that the market is starting to believe the turnaround narrative. With the heavy lifting of capital investment behind them and a clear path to 12% margins, the stock is positioning itself as a resilient, high-yield play for 2026. However, its success hinges entirely on the recovery of the semiconductor cycle and the management's ability to trim the corporate fat without losing its technical edge.

Please wait processing your request...

Please wait processing your request...