Key Takeaways

- The Catalyst: A fresh £70 million share buyback program announced today is the primary fuel.

- The Aggressor: New reports surface today that Frasers is circling SilkFred for a potential takeover.

- The Strategy: The "Elevation" strategy is working - margins are up despite retail headwinds.

- The Vibe: Cash-rich, hungry for deals, and aggressively fixing its own undervalued share price.

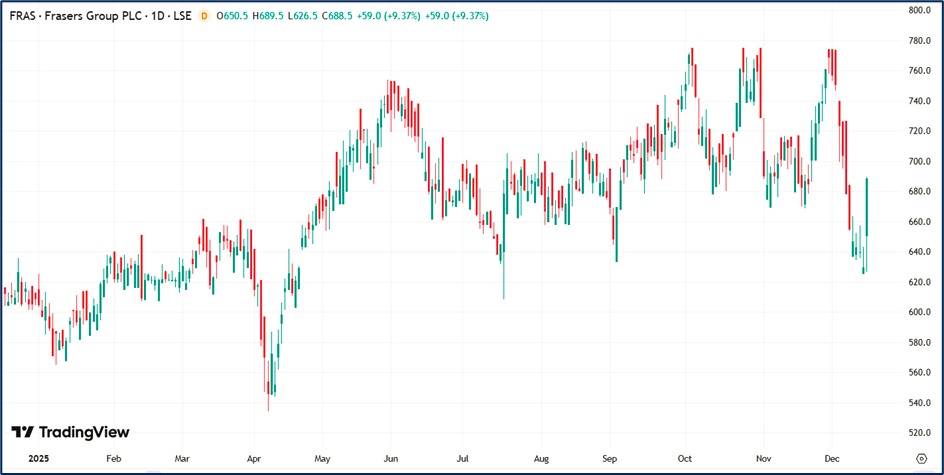

- Why the 9% Jump? (The Drivers)

The market hates uncertainty but loves cash returns. Frasers Group delivered a double whammy of confidence today:

- The £70m Buyback (Immediate Trigger): Frasers announced a share buyback program of up to £70 million, running until April 2026.

- Why it matters: It signals management believes the stock is severely undervalued. By reducing the share count, they boost Earnings Per Share (EPS) for remaining holders. It's a massive vote of confidence from the inside.

- The "Deal Hunter" Premium (SilkFred Rumors): Reports broke today that Frasers is eyeing a bid for the fashion marketplace SilkFred.

- The Pattern: This fits perfectly with their strategy of snapping up distressed or strategic assets (like they did with Mulberry, Boohoo stakes, and Swindon Designer Outlet last week). The market loves the "Frasers Machine" acquiring revenue streams on the cheap.

- Solid Fundamentals (The Backdrop): Investors are still digesting the H1 results (released recently) which showed a 160bps margin improvement. While revenue is tricky in this economy, Frasers is becoming more profitable per sale.

- The "Frasers Machine": Business Model Decoded

Frasers isn't just "Sports Direct" anymore. It is a diversified retail conglomerate acting like a Private Equity firm.

- The "Elevation" Strategy: Moving away from the "pile it high, sell it cheap" image.

- Flannels: The luxury engine.

- New Gen Sports Direct: Sleek stores carrying premium Nike/Adidas lines that competitors can't get.

- The Ecosystem (The "Flywheel"):

- Brands: Owns the IP (Everlast, Slazenger, Jack Wills) = 100% margin capture.

- Retail: Owns the shelf space (House of Fraser, Sports Direct, GAME).

- Credit: Frasers Plus (their Buy Now, Pay Later service) locks customers into the ecosystem and gathers massive data.

- Strategic Stakes: They hold "influence" stakes in competitors (AO World, ASOS, Boohoo, Currys). This gives them a seat at the table or a hedge against the sector.

- Latest Business Updates (Dec 2025 Context)

- Swindon Acquired: Just bought the Swindon Designer Outlet to expand physical footprint.

- Boardroom Power: CEO Michael Murray (Mike Ashley’s son-in-law) has successfully pivoted the brand image while retaining Ashley’s ruthless deal-making DNA.

- Treasury Stash: The balance sheet remains robust enough to fund both this £70m buyback and potential acquisitions like SilkFred simultaneously.

- Risks to Watch

Even with a 9% pop, it's not all clear skies:

- UK Consumer Squeeze: Discretionary spending is still under pressure from high interest rates and energy costs. Frasers is cyclical.

- Governance Perception: While improving, the "Mike Ashley factor" still spooks some institutional investors who fear unpredictable capital allocation.

- Integration Indigestion: Buying SilkFred, Mulberry, and outlets is great, but integrating distinct tech stacks and cultures is messy and costly.

Conclusion: The "Retail King" Flexes

Frasers Group is currently the "apex predator" of the UK high street. The 9% surge today is a direct response to a management team that puts its money where its mouth is (buybacks) while refusing to slow down its expansion (acquisitions). They are effectively saying: "If the market won't value us correctly, we will buy ourselves."

Source: Trading View, 15 December 2025, 11:20 AM GMT

Please wait processing your request...

Please wait processing your request...