The FTSE 100 opened 2026 with a clear signal: the "old-school publisher" tag is officially dead. Pearson PLC (LSE: PSON) shares climbed approximately 2% on Monday, January 5, 2026, as the market digested a series of strategic wins and the realization that its "AI-First" business model is no longer just a roadmap—it’s a revenue engine.

The "Day 1" Catalyst: Key Drivers for the Jan 5 Spike

Source: Kalkine Group

While the broader market saw a "New Year, New Portfolio" rotation, Pearson’s specific 2% jump was fueled by three tactical drivers:

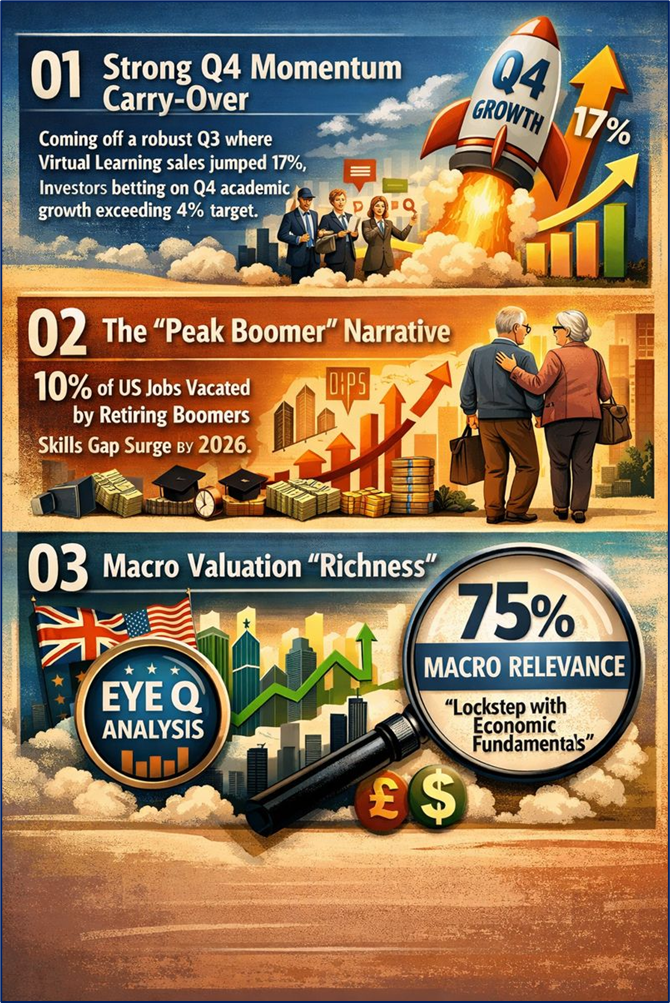

- Strong Q4 Momentum Carry-Over: Coming off a robust Q3 where Virtual Learning sales jumped 17%, institutional investors are betting that the Q4 academic cycle (typically Pearson’s strongest) has met or exceeded the 4% underlying sales growth target.

- The "Peak Boomer" Narrative: New demographic reports for 2026 highlight a massive skills gap as 10% of US jobs are vacated by retiring Boomers. Pearson’s Enterprise Learning & Skills division is the primary beneficiary of this corporate upskilling rush.

- Macro Valuation "Richness": Analysis from eyeQ suggests that while Pearson's price is trending higher, its "macro relevance" score remains high (75%), indicating the stock is moving in lockstep with improving UK and US economic fundamentals.

Latest Business Model: From Paper to "Agentic" Platforms

Pearson has successfully transitioned from a cyclical textbook provider to a Digital-First, Lifelong Learning Ecosystem. Its 2026 model rests on five pillars:

- Assessment & Qualifications (45% of Sales): The "Moat." High-stakes testing (Pearson VUE) and school qualifications that provide steady, recurring cash flow.

- Virtual Learning (14% of Sales): Full-service online schools (Connections Academy). It recently hit 41 schools across 31 US states.

- English Language Learning (12% of Sales): Powered by the Pearson Test of English (PTE), which is now a global standard for visa and university applications.

- Higher Education (22% of Sales): No longer just eBooks. The focus is now on "Inclusive Access" (subscription models) and AI Study Prep tools.

- Enterprise Learning & Skills (8% of Sales): The "Growth Engine." Partnerships with giants like Salesforce, Deloitte, and Cognizant to certify the global workforce.

2026 SWOT Analysis: The Analytical Lens

Source: Kalkine Group

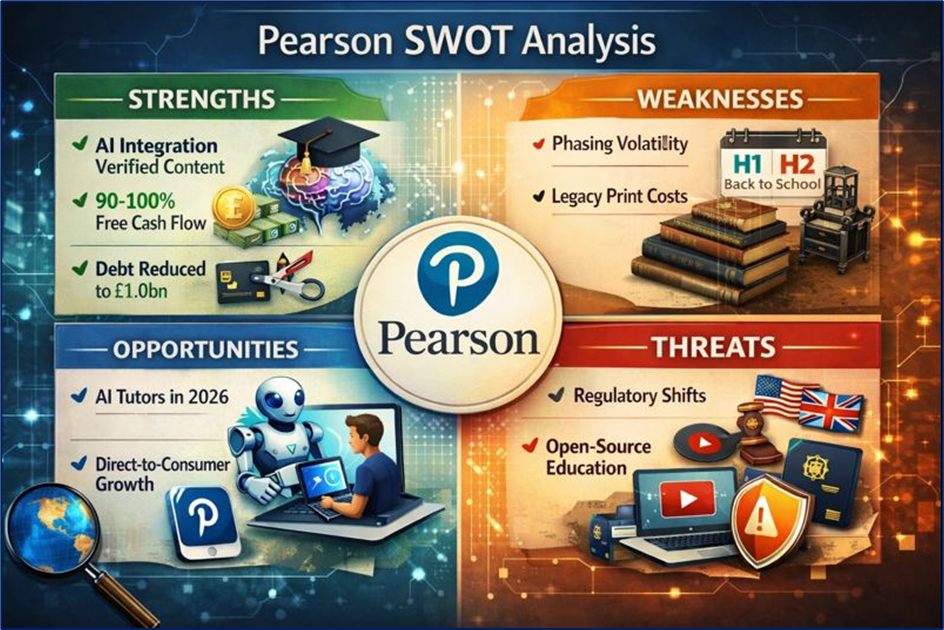

Strengths

- AI Integration: Unlike many, Pearson owns its content. Feeding proprietary, verified data into AI tools (like the GCSE Exam Practice Assistant) prevents the "hallucination" risks of open-source AI.

- Cash Conversion: A "Golden Ratio" of 90-100% free cash flow conversion, allowing for consistent dividends and the ongoing £350m share buyback.

- Debt Reduction: Net debt has been whittled down to £1.0bn (as of H2 2025), providing a massive cushion for M&A.

Weaknesses

- Phasing Volatility: Results are heavily weighted toward H2 (back-to-school), which can lead to share price "lulls" in the spring.

- Legacy Drag: Small pockets of traditional print media still exist, requiring high maintenance costs despite declining demand.

Opportunities

- Agentic AI: 2026 is the year of "AI Agents." Pearson is launching systems that act as 24/7 personal tutors for students and productivity partners for employees.

- Direct-to-Consumer (D2C): Moving away from just institutional sales to selling directly to individual "lifelong learners" via the Pearson+ app.

Threats

- Regulatory Shifts: Changes in US/UK immigration policy can instantly impact PTE (English Test) volumes.

- Open-Source Education: Free AI tools and YouTube-based learning remain a low-cost threat to the Higher Education segment.

Financial & Operational Update: The Numbers That Matter

As of the latest January 2026 outlook:

- Profitability: Targeted 40 basis point annual margin expansion is on track, driven by "operating leverage"—growing sales without increasing fixed costs.

- Dividends: The interim dividend was hiked 5% recently, signaling management’s confidence in the 2026 cash pipeline.

- Efficiency: AI tools for teachers have halved the time needed to create custom student assessments, significantly increasing the "stickiness" of Pearson’s platforms in schools.

The Risk Register

Investing in a "transitional" giant isn't without hurdles:

- Cybersecurity: As a data-rich company, any breach of student or professional certification data would be catastrophic for the brand.

- AI Disruption: While Pearson is leading, a "Leapfrog" technology from a Silicon Valley startup could potentially commoditize educational content.

- Interest Rates: Higher rates increase the cost of student loans, which can indirectly dampen Higher Education enrollment.

Conclusion

Pearson’s 2% climb on January 5, 2026, reflects a company that has successfully navigated the "Valley of Death" between print and digital. With a lean balance sheet, a dominant position in high-stakes testing, and a clear path to monetizing AI, the market is finally treating Pearson as a Tech-Ed powerhouse rather than a legacy publisher.

Please wait processing your request...

Please wait processing your request...