As of January 23, 2026, Rolls-Royce Holdings PLC (LSE: RR) remains a focal point of the FTSE 100, extending a multi-year transformation that has fundamentally redefined its market status. No longer viewed as a struggling legacy engineer, the company has successfully pivoted into a high-margin "growth monster," fueled by a resurgence in global long-haul travel and a strategic aggressive push into the burgeoning data centre and defense sectors.

With the share price testing historic highs near the 1,245p-1,300p range, the narrative has shifted from one of survival to one of relentless operational execution and cash generation, positioning the firm as a premier industrial powerhouse for the late 2020s.

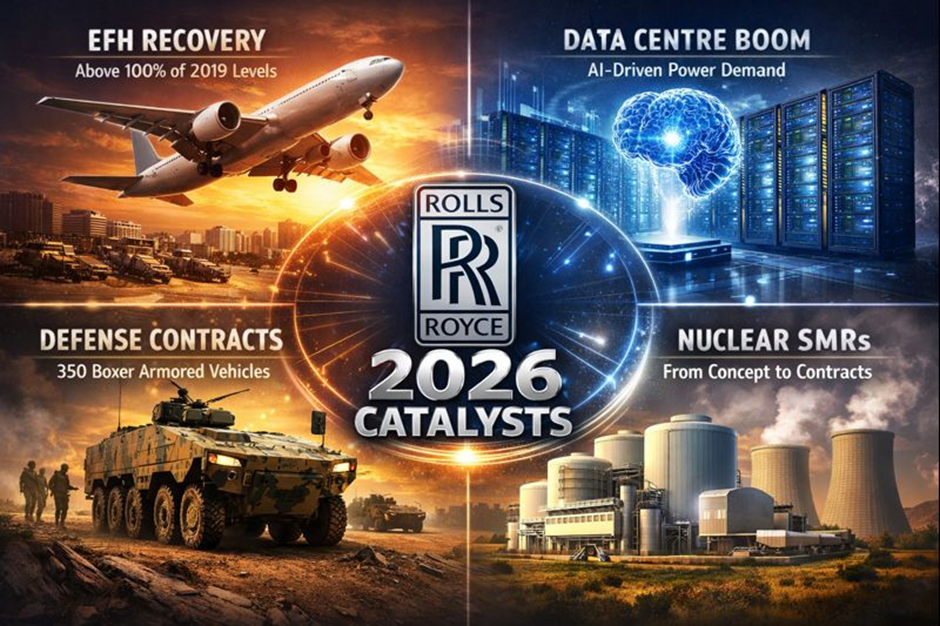

Latest Drivers of the Surge

Source: Kalkine Group

The current momentum in Rolls-Royce shares is underpinned by several critical 2026 catalysts:

- Engine Flying Hour (EFH) Recovery: Large engine flying hours have surpassed 100% of 2019 levels, directly boosting high-margin Long-Term Service Agreement (LTSA) revenues.

- Data Centre Boom: The Power Systems division is experiencing unprecedented demand for mtu backup power solutions, driven by the global AI infrastructure build-out.

- Defense Contracts: Significant new orders, including a January 21, 2026, announcement for 350 mtu engines for Boxer armored vehicles, highlight the company's vital role in European rearmament.

- Nuclear Milestones: The selection of Rolls-Royce as the preferred supplier for Small Modular Reactors (SMRs) in multiple jurisdictions has shifted the nuclear segment from "concept" to "contract pipeline."

Current Business Model

Rolls-Royce operates a high-moat, vertically integrated model across three primary pillars:

- Civil Aerospace: Focused on widebody engines (Trent family). The model relies on "Power by the Hour" contracts, where profit is derived from maintenance and parts over a 20+ year lifecycle rather than just the initial sale.

- Defense: A Tier-1 supplier for transport, combat, and naval propulsion. It serves as the sole provider of nuclear power plants for the UK’s submarine fleet.

- Power Systems: Specializes in high-speed reciprocating engines for power generation and marine applications. It is increasingly shifting toward "non-governmental" clients like global hyperscale data centers.

Latest Financial & Operational Updates

According to recent company disclosures and the 2026 guidance trajectory:

- Profitability: Management has set a target operating profit of £3.1bn to £3.2bn for the current cycle (Company Guidance, Jan 2026).

- Cash Flow: Free cash flow is projected to reach £3.0bn to £3.1bn, allowing for the continued reduction of legacy debt (Company Source).

- Dividends & Buybacks: Following the reinstatement of dividends in 2025, the company recently announced an interim share buyback program in late December 2025 to return surplus capital to shareholders (RNS/Company Filing).

- Operations: Ground was broken on January 8, 2026, for a world-leading aero-engine maintenance facility in collaboration with Turkish Technic, expanding global MRO capacity (Company Press Release).

Latest SWOT Analysis

Source: Kalkine Group

Strengths

- Dominant Market Position: Exclusive engine supplier for the Airbus A350 and A330neo.

- Financial Health: Transition from net debt to a net cash position of approximately £1.1bn.

- Operational Efficiency: Successful "4 Pillar" strategy has expanded operating margins to nearly 20%.

Weaknesses

- Segment Concentration: Heavy reliance on widebody long-haul travel, leaving it vulnerable to specific aviation shocks.

- Supply Chain Fragility: Persistent constraints in the aerospace supply chain continue to impact delivery lead times.

Opportunities

- SMR Commercialization: A projected $295bn global market for small modular reactors by 2043.

- UltraFan Technology: Potential to capture the next-generation narrow-body market with 25% better fuel efficiency.

- AI Infrastructure: Massive growth potential in providing mission-critical power for global data centers.

Threats

- Geopolitical Protectionism: Rising tariffs (e.g., US-EU trade tensions) could impact cross-border component costs.

- Environmental Regulation: Pressure to accelerate the transition to Sustainable Aviation Fuel (SAF) and hydrogen may increase R&D burdens.

Outlook and Risks

The outlook for Rolls-Royce in 2026 is robust but demands flawless execution. The company is aiming to double annual revenue in the five years leading to 2030. However, the "thinning air" at record valuations means there is little room for error. Key risks include a potential slowdown in China’s travel market, unexpected durability issues with the Trent engine fleet, and the slow pace of government approvals for nuclear projects.

Conclusion

Rolls-Royce has successfully shed its image as an industrial laggard to become a high-performance cash generator. By aligning its core engineering expertise with the global demand for AI infrastructure, defense security, and carbon-neutral energy, the firm has built a diversified growth engine. While the valuation now reflects much of this "good news," the structural moats provided by its long-term service agreements and technical leadership ensure that Rolls-Royce remains the quintessential barometer for British engineering excellence on the global stage.

Please wait processing your request...

Please wait processing your request...