Fresnillo shares surged 6.72% on 26 January, instantly snapping investor attention back to the FTSE 100’s largest precious-metals producer. The rally didn’t hinge on a single headline. Instead, it reflected a tight convergence of macro tailwinds, operational reassurance from the company’s latest disclosures, and renewed conviction around silver and gold as strategic assets.

With metals prices firming and execution risks easing, the market repriced near-term confidence in Fresnillo’s operating story.

What sparked the surge — the latest drivers investors latched onto

Source: Kalkine Group

- Precious-metals momentum

Gold and silver prices firmed as global real yields softened and volatility ticked higher across risk assets. Silver, Fresnillo’s core profit driver, outperformed gold on industrial-demand optimism tied to electrification and solar installations. - Operational delivery stabilising

Recent company updates signalled improving grade consistency at key mines and tighter cost discipline, easing fears that had lingered through earlier periods of operational disruption (Fresnillo operational update). - Mexico-specific risk premium compressing

No new adverse regulatory developments emerged, and the absence of policy shocks allowed investors to unwind part of the long-standing Mexico discount applied to mining equities. - Short-covering and positioning reset

Following months of cautious positioning in miners, improving sentiment toward metals triggered momentum flows and short covering, amplifying the one-day move.

Fresnillo’s business model — simple on the surface, operationally complex underneath

Fresnillo operates a vertically integrated precious-metals model focused primarily on silver, with gold as a significant co-product. The group controls the full mining value chain, from exploration and development through to production and refining, predominantly within Mexico.

- Asset concentration with scale advantages

Large, long-life assets such as Saucito, Fresnillo, Herradura, and Juanicipio underpin production visibility and economies of scale. - Silver-led revenue mix

Silver remains the dominant earnings driver, giving Fresnillo a natural leverage to any upside in the metal while exposing it to sharper downside during weak cycles. - In-house exploration pipeline

A strong exploration function supports reserve replacement, a key differentiator versus peers reliant on acquisitions. - Operational leverage

Fixed-cost intensity means even modest improvements in grades or recoveries can materially lift margins during supportive price environments.

Latest financial, operational and dividend signals from the company

- Production trends

Recent disclosures highlighted stable to improving output profiles, with Juanicipio continuing to ramp up toward steady-state performance and contributing higher-grade silver volumes (Fresnillo production update). - Cost management

Management reiterated focus on cost containment amid inflationary pressures, with unit costs expected to stabilise as energy and consumables pressures moderate (Fresnillo financial update). - Balance sheet resilience

The group maintained a conservative balance-sheet stance, prioritising liquidity and operational flexibility over aggressive capital returns (Fresnillo results statement). - Dividend framework

Dividend distributions remain linked to profitability and cash generation, preserving balance-sheet strength through commodity cycles rather than committing to a rigid payout (Fresnillo dividend policy update).

Why the market reaction mattered more than the headline number

This wasn’t just a price pop. The move reflected a broader shift in perception: Fresnillo transitioning from a “problem execution story” to a “cyclical leverage with improving control” narrative.

- Investors responded to reduced downside risk, not speculative upside alone

• Confidence grew around earnings sensitivity to silver prices rather than operational setbacks

• The stock re-entered momentum screens after lagging the wider mining sector

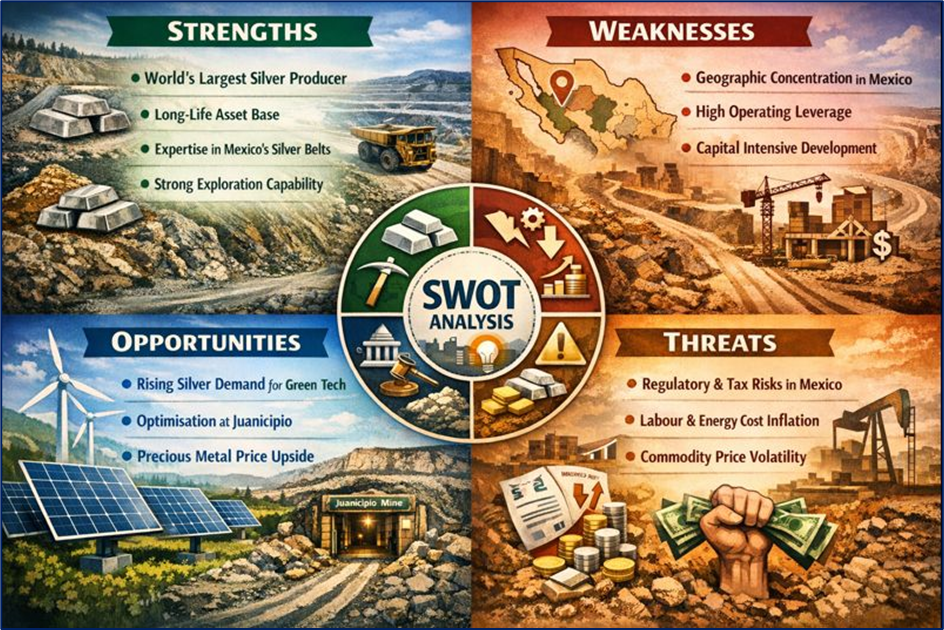

SWOT snapshot — Fresnillo at this stage of the cycle

Source: Kalkine Group

Strengths

• World’s largest primary silver producer with unmatched scale

• Long-life asset base with established infrastructure

• Deep geological knowledge of Mexico’s richest silver belts

• Strong exploration capability supporting reserve longevity

Weaknesses

• Heavy geographic concentration in Mexico

• High operating leverage magnifies cost and grade volatility

• Capital intensity during development phases

Opportunities

• Rising industrial silver demand from energy transition technologies

• Further optimisation at Juanicipio as the mine matures

• Margin expansion potential if precious-metals prices remain firm

Threats

• Regulatory or fiscal shifts in Mexico

• Labour and energy-cost inflation

• Commodity-price reversals driven by stronger real rates

Outlook — why sentiment has turned constructive without becoming euphoric

Near-term sentiment toward Fresnillo is being shaped by a cleaner operational backdrop and supportive metals pricing rather than blue-sky assumptions.

- Operational visibility improving as key assets move into steadier production phases

• Silver’s dual role — industrial metal and monetary hedge — broadens its demand base

• Cost pressures easing relative to the prior year’s peaks

That said, expectations remain grounded. The market is rewarding delivery and discipline, not forecasting a straight-line rally.

Key risks investors are still watching closely

- Metal-price volatility

Silver remains historically volatile, and sharp pullbacks can quickly compress margins. - Country concentration

Any deterioration in Mexico’s mining framework would disproportionately affect Fresnillo relative to diversified peers. - Operational execution

Complex underground mining leaves little margin for error if grades or recoveries disappoint. - Currency movements

Peso strength versus the US dollar can pressure local cost bases.

Compelling conclusion — why this move resonated

Fresnillo’s 6.72% jump on 26 January was less about excitement and more about relief — relief that operations are stabilising, relief that metals are back in favour, and relief that execution risk appears better contained than before. In a market searching for real assets with tangible cash-flow leverage, Fresnillo reminded investors why it remains a bellwether for silver exposure in the FTSE 100. The rally underscored a recalibration of confidence rather than a speculative frenzy — a subtle but meaningful distinction.

Please wait processing your request...

Please wait processing your request...