London’s blue-chip index defies global volatility, hitting $10,191.76 as financial heavyweights and Asian-exposed giants propel the FTSE to record-breaking territory.

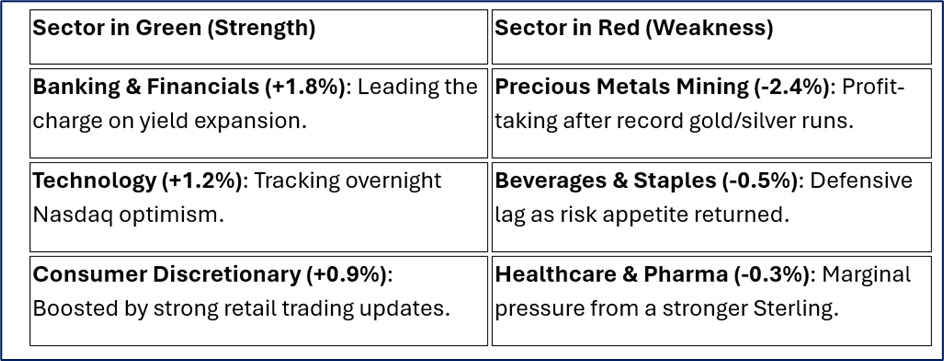

The FTSE 100 showcased remarkable resilience on Tuesday, January 27, 2026, gaining 0.42% to settle at 10,191.76. While European peers like the DAX and CAC 40 flirted with the red, London’s benchmark was buoyed by a "perfect storm" of sector rotation. Investors shifted aggressively into Financials and Banking, anticipating a "higher-for-longer" yield environment confirmed by sticky UK inflation data.

Simultaneously, a wave of optimism regarding Chinese stimulus measures provided a significant tailwind for the index's Asia-focused constituents, effectively cushioning the blow from a temporary cooling in the red-hot precious metals sector.

Market Snapshot: The Green vs. The Red

On January 27, 2026, the market split was defined by a rotation out of "safe-haven" commodities and into "growth-yield" financials.

Source: Market Data

Top Gainers: Why They Soared

Source: Kalkine Group

The day belonged to the lenders and the China-proxies.

- HSBC (HSBA): Up 2.1%. The dual-listed giant benefited from a "double-dip" of positive sentiment—stronger-than-expected Asian growth forecasts and positioning ahead of its February earnings.

- NatWest Group (NWG): Up 1.9%. Investors are piling into domestic banks as the Bank of England signals that rate cuts remain "off the table" due to persistent service-sector inflation.

- Prudential (PRU): Up 1.7%. As a primary proxy for Asian insurance growth, Prudential rose on the back of easing geopolitical tensions in the Pacific and renewed demand for HK/China exposure.

- St. James's Place (STJ): Up 1.5%. Wealth management saw a boost as the FTSE 100’s breach of the 10,000 mark improved institutional AUM (Assets Under Management) outlooks.

- Auto Trader (AUTO): Up 1.4%. Benefited from a tech-sector halo effect and upbeat data regarding UK used-car price stability.

Top Losers: The Drivers of the Dip

The "risk-on" mood elsewhere meant the defensive and commodity plays felt the squeeze.

- Fresnillo (FRES): Down 2.5%. Despite gold hovering near $5,100/oz, Fresnillo saw sharp profit-taking ahead of its January 28 production report, as traders locked in gains from a 170% annual rally.

- Antofagasta (ANTO): Down 2.4%. A cooling in copper prices and a pause in the "merger-mania" speculation surrounding Rio Tinto and Glencore weighed on the stock.

- ConvaTec (CTEC): Down 1.2%. The medical device maker suffered as investors rotated capital into more aggressive growth sectors.

- Diageo (DGE): Down 0.9%. The spirits giant remains under pressure from softening "premiumization" trends in the US and a lack of fresh catalysts.

- Experian (EXPN): Down 0.7%. Faced head-to-head competition for capital against the high-yielding retail banks.

Technical Analysis Summary: The 10,200 Threshold

Source: Trading View

Technically, the FTSE 100 is in a confirmed bullish breakout phase. After smashing the psychological 10,000 barrier earlier this month, the index is now using 10,150 as a new floor (support).

- Resistance: The immediate target for bulls is the mid-January peak of 10,256. A clean break above this could open the door to the 10,350 Fibonacci extension level.

- Support: Significant support sits at 10,140, followed by the "Line in the Sand" at 10,000.

- Momentum: The Relative Strength Index (RSI) is hovering around 67, signaling the index is "warm" but not yet in the extreme "overbought" territory ($>70$), suggesting there is still room for further upside.

Conclusion: The New Era of Five-Figure Trading

Today’s session confirms that the FTSE 100’s journey into five-figure territory is not a fluke but a fundamental repricing. With the "Old Economy" sectors like banking and energy now acting as growth engines rather than anchors, London has reclaimed its status as a premier destination for global capital. While mining volatility remains a wild card, the sheer momentum in the financial sector suggests that 10,200 is merely a pitstop on a much longer climb.

Please wait processing your request...

Please wait processing your request...