Executive Summary: The Record Run Stalls

After a euphoric start to 2026 that saw the FTSE 100 smash through the historic 10,000 barrier, reality bit back on Wednesday. The UK’s premier index closed down 74.52 points (0.74%) at 10,048.21, retreating from Tuesday's record highs.

While the broader trend remains bullish, a "perfect storm" of plummeting oil prices—triggered by fresh directives from the White House—and profit-taking in the mining sector forced the index into the red. However, it wasn't a sea of red; the domestic-focused FTSE 250 actually rose 0.4%, and defensives provided a safe harbor for nervous capital.

The 3 Primary Drivers: Why the Drop?

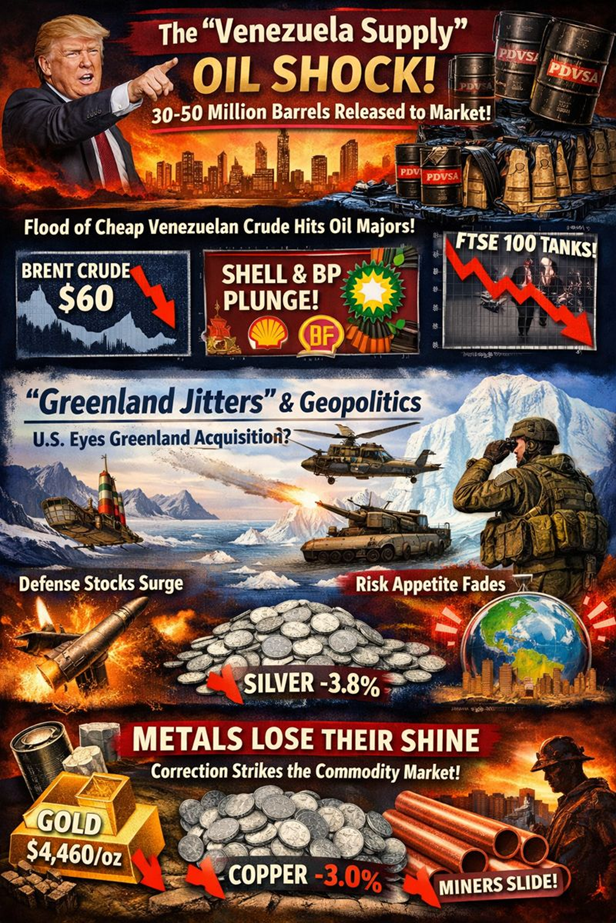

1. The "Venezuela Supply" Oil Shock

The single biggest weight on the index was the energy sector. Brent Crude tumbled toward $60/barrel after US President Donald Trump announced a surprise deal to release 30-50 million barrels of Venezuelan oil onto the open market.

- The Catalyst: Trump stated the proceeds would be controlled to "benefit the people," effectively flooding a market already worried about oversupply.

- The Impact: Oil majors Shell and BP, which account for a massive chunk of the FTSE 100's weighting, were hammered as traders priced in lower margins for Q1 2026.

2. "Greenland Jitters" & Geopolitics

Uncertainty spiked following "murmurings" from Washington regarding the potential acquisition of Greenland. With the administration not ruling out military options to secure the territory for national security, risk appetite for global cyclical stocks faded. This geopolitical noise pushed investors toward Defense stocks and away from riskier assets.

3. Metals Lose Their Shine

After a blistering run, precious and industrial metals saw a sharp correction.

- Gold dipped below $4,460/oz, and Silver shed nearly 3.8%.

- Copper retreated 3.0%, dragging down the heavyweight mining sector. Investors locked in profits, fearing that the "reflation trade" might be cooling off amidst the new supply-side oil dynamics.

Source: Kalkine Group

Winners & Losers: The Stock Movers

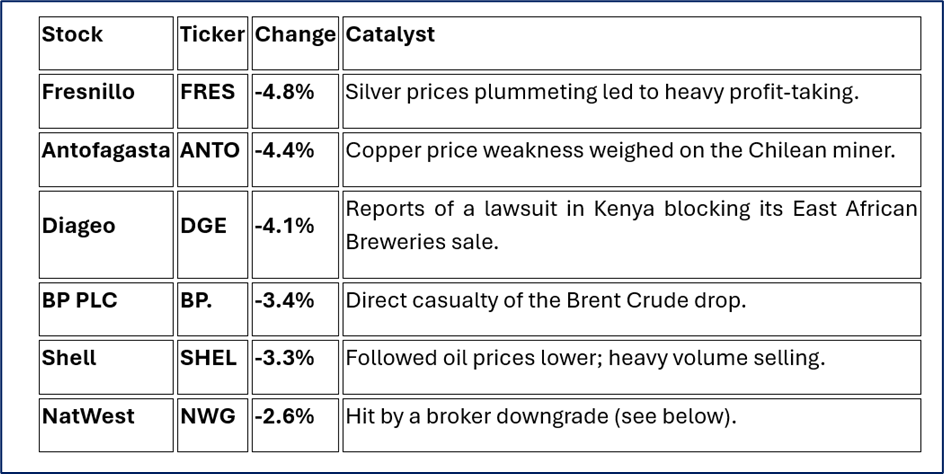

The Losers: Commodities & Banks

The "sell" button was hit hardest in the resource sectors and financials.

Source: Kalkine Group

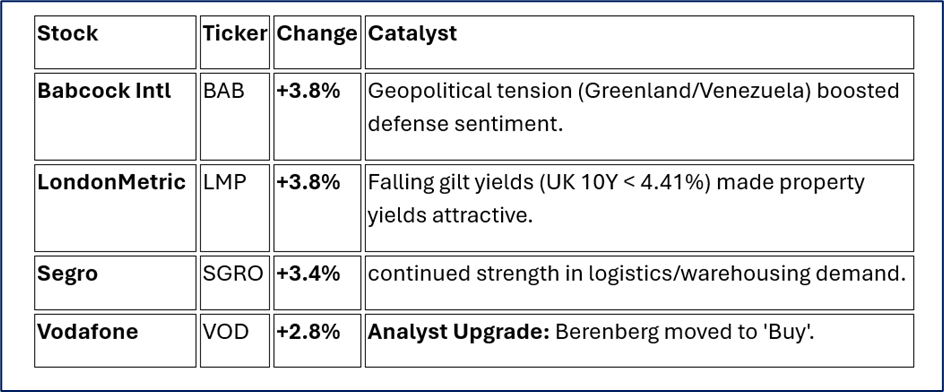

The Gainers: Defense, Property & Tech

Capital didn't leave the market; it rotated. Investors sought safety in defense and yield in property.

Source: Kalkine Group

Analyst Intel: Upgrades & Downgrades

Institutional adjustments played a key role in individual stock moves on Jan 7.

- Vodafone (BUY): Berenberg upgraded the telecom giant from Hold to Buy, citing improved free cash flow visibility. This pushed VOD to the top of the leaderboard early in the session.

- Relx (OUTPERFORM): JPMorgan issued a bullish note, describing the company's "AI glass" as overflowing, suggesting the recent pullback was a prime buying opportunity.

- NatWest (NEUTRAL): Barclays downgraded the bank to Equalweight, causing it to underperform its peers.

- Hikma Pharmaceuticals (SELL): Barclays cut Hikma to Underweight, sending the stock down nearly 2%.

Technical Analysis: The View from the Charts

- Current Level: 10,048.21

- Trend: Bullish, but consolidating.

- RSI (Relative Strength Index): The index has exited "Overbought" territory (>70), cooling off to more neutral levels. This is healthy for a sustained rally.

Key Levels to Watch:

- Support 1 (Immediate): 10,000 – The psychological "floor." Bulls must defend this to keep the '2026 Breakout' narrative alive.

- Support 2 (Critical): 9,920 – The November high. A break below here signals a deeper correction toward the trendline at 9,800.

- Resistance: 10,160 – The intra-day record high. A close above this level is needed to resume the uptrend toward 10,200/10,300.

Technical Verdict: The primary uptrend is intact. The dip to 10,048 represents a retest of the breakout zone. As long as 9,920 holds, technicals favor "buying the dip."

Source: Trading View

Global Context: The Macro View

The FTSE didn't fall in a vacuum. The global stage on Jan 7 was dominated by:

- US Bond Yields: The US 10-Year Treasury yield narrowed to 4.15%, and UK Gilts fell to 4.41%. Lower yields are generally supportive of equities (especially housing/property), cushioning the FTSE's fall.

- US Data Mixed: A strong ISM Services PMI was offset by a surprise drop in job vacancies (JOLTS), leaving markets guessing ahead of Friday’s crucial Non-Farm Payrolls.

- Eurozone Inflation: Confirmed at 2.0% for December, cementing expectations that the ECB will hold rates steady, providing stability across the channel.

What This Means For Your Portfolio

The "Trump Trade" is evolving. It is no longer just about deregulation; it is now about active intervention in commodity markets (e.g., Venezuela oil).

- If you hold Energy: Expect volatility. The floor for oil has likely lowered to the $55-$60 range.

- If you hold Defense: Geopolitical noise is your friend.

- If you hold Property: The drop in bond yields is a green light for REITS and housebuilders.

Please wait processing your request...

Please wait processing your request...