JD Sports Fashion (LSE: JD) kicked off the first full trading session of 2026 with a resilient +1.5% nudge upward. While the broader retail sector remains under a magnifying glass, the "King of Trainers" is proving that even in a "volatile" economy, its global footprint is a force to be reckoned with.

Below is a deep-dive analysis of why the stock moved, the latest business model shift, and whether the operational engine is firing on all cylinders.

The Jan 2 Momentum: What’s Driving the Price?

Source: Kalkine Group

The 1.5% uptick on January 2nd wasn't a fluke; it was a combination of valuation hunting and strategic optimism:

- Undervaluation Signal: After a tough 2025 where the stock was frequently labeled "undervalued" (trading at a forward P/E as low as 7-8x), institutional investors are starting 2026 by picking up "beaten-down" quality.

- The "Nike Pivot": Market sentiment is shifting as key partner Nike eases its "Direct-to-Consumer" (DTC) obsession, returning more focus to wholesale partners like JD. Since Nike accounts for roughly 45% of JD’s revenue, this is a massive tailwind.

- Holiday Residuals: Early whispers of "resilient" holiday spending—particularly in the US and Europe—provided a safety net for the stock price as traders returned from the break.

Latest Operational & Financial Updates

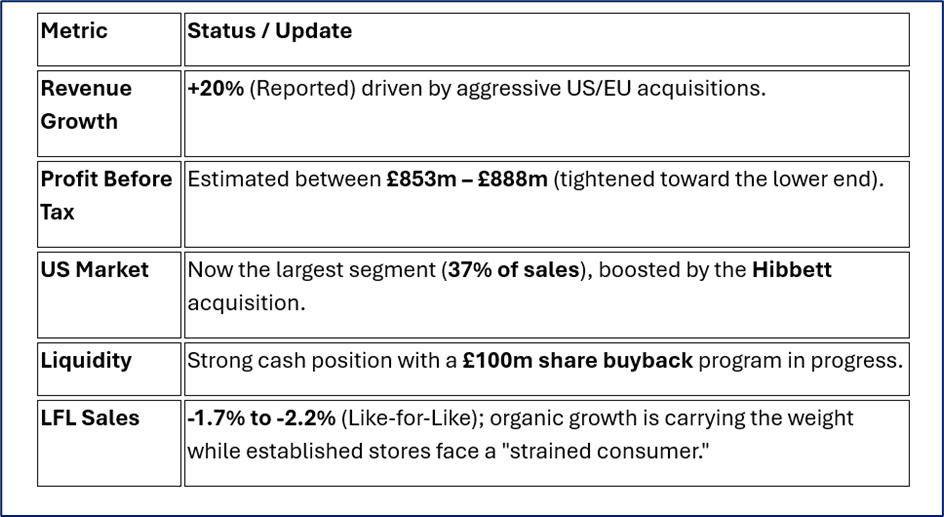

JD Sports is no longer just a UK high-street shop; it is a global powerhouse with 4,800+ stores. Here is the state of play for Fiscal Year 2026 (FY26):

Source: Company Data

The 2026 Business Model: "JD Brand First"

The "Schultz Era" (under CEO Régis Schultz) has moved the company into a new phase: Operational Discipline.

- JD Brand First: Converting regional acquisitions (like Finish Line in the US) into the global "JD" fascia to build a unified powerhouse brand.

- Complementary Concepts: Keeping brands like Hibbett (US) and Courir (Europe) to reach different demographics that the core JD brand might miss.

- Beyond Physical Retail: A massive push into the "JD STATUS" loyalty program (now 9m+ members) to collect first-party data and drive repeat digital sales.

- Supply Chain Optimization: New automated distribution centers in the US and EU are finally "ramping up" to lower the cost per unit shipped.

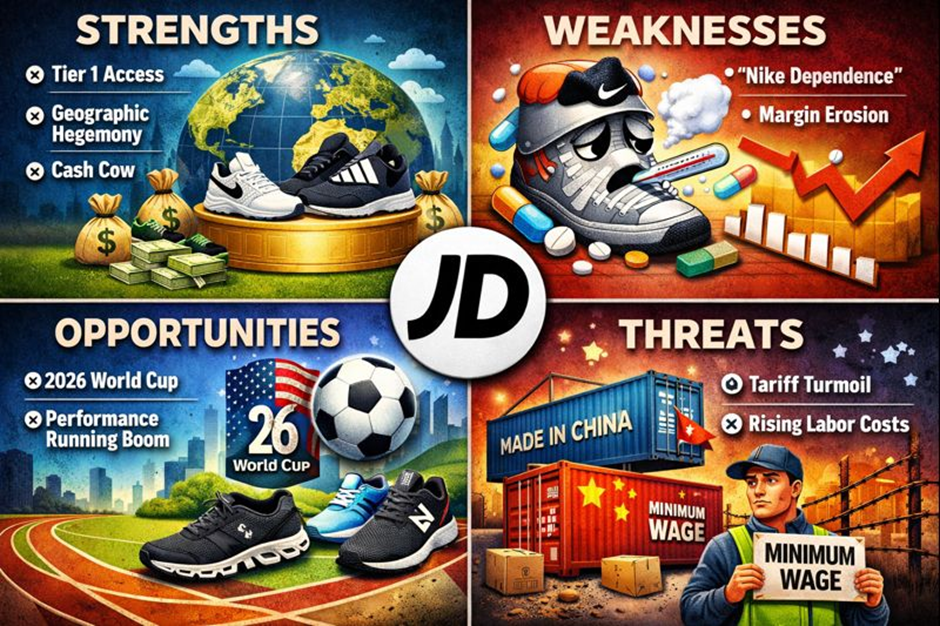

SWOT Analysis (The Strategic Reality)

Source: Kalkine Group

Strengths

- Tier 1 Access: Unlike smaller rivals, JD gets "first dibs" on exclusive releases from Nike and Adidas.

- Geographic Hegemony: Significant scale in North America, Europe, and Asia-Pacific reduces UK-specific economic risk.

- Cash Cow: Consistently generates high free cash flow, allowing for dividends and buybacks even in "down" years.

Weaknesses

- The "Nike Dependence": If Nike sneezes, JD catches a cold. 45% revenue concentration is a double-edged sword.

- Margin Erosion: Increased promotional activity to clear stock in a "promotional market" has shaved ~60bps off gross margins.

Opportunities

- 2026 World Cup: The upcoming tournament in North America is a "catalyst event" for jersey and footwear sales.

- Running Segment: JD is pivoting away from "Retro Basketball" (which is cooling) into the high-growth "Performance Running" sector (On, Hoka, New Balance).

Threats

- Tariff Turmoil: Potential US tariffs on Chinese-made footwear remain a "known unknown."

- Labor Costs: Minimum wage increases in the UK and US are putting pressure on the "cost to serve" in-store.

The Risk Radar

Investors are keeping a close eye on "Sticky Inflation." While JD's core "Gen Z" demographic is usually resilient, the data shows they are finally starting to feel the pinch. If Like-for-Like (LFL) sales don't turn positive by Q2 2026, the stock may struggle to break out of its current range.

Conclusion

JD Sports enters 2026 as a leaner, more global version of its former self. The 1.5% gain on Jan 2 reflects a market that is cautiously optimistic about the company's ability to manage costs and leverage its "Brand Partner" relationships. While the "Golden Age" of double-digit LFL growth has paused, the sheer scale of the JD empire makes it a formidable FTSE 100 titan.

Please wait processing your request...

Please wait processing your request...