The London Open: A Delicate Balancing Act

The FTSE 100 is treading water this Friday, January 23, 2026, as a "data deluge" of domestic economic reports clashes with a complex geopolitical backdrop. Currently trading at 10,139.30, down a marginal -0.11%, the index reflects a market caught between two worlds: surprisingly resilient UK consumer data and the cooling effects of a strengthening Pound.

While the morning brought news of an unexpected rebound in retail sales, the initial relief has been tempered by a cautious technical setup and profit-taking after the index’s recent push toward all-time highs. Investors are essentially in a "wait-and-see" mode, weighing the prospect of domestic growth against the global headwinds of shifting trade policies and high-stakes diplomatic meetings in the UAE.

Current Key Drivers: Retail Resurgence vs. Currency Pressure

Source: Kalkine Group

- Retail Sales Surprise: The Office for National Statistics (ONS) reported a 0.4% rise in December retail volumes, smashing analyst expectations of a flat reading. This has provided a floor for consumer-facing stocks.

- PMI Momentum: Flash Purchasing Managers' Index (PMI) data showed the UK private sector growing at its fastest pace in nearly two years (53.9), signaling robust economic health but also stoking fears of "sticky" inflation.

- The "Greenland" Relief: Global sentiment remains buoyed after President Trump withdrew tariff threats against European nations over the Greenland dispute, though the FTSE’s gains are limited by a stronger Sterling, which makes exported earnings less valuable.

- Geopolitical Watch: All eyes are on the UAE, where US, Russian, and Ukrainian officials are meeting. The potential for a "nearly ready" peace deal is keeping volatility high in energy and defense sectors.

The Winners & Losers: Sectors and Stocks

Sectors in the Green

- Financial Services: Driven by strong inflows and record Assets Under Management (AUM) reports from firms like Record PLC.

- Energy: Buoyed by stabilized oil prices and optimism surrounding potential de-escalations in Eastern Europe.

- Technology & Software: Benefiting from the "AI-spend" cycle identified in the latest IMF global outlook.

Sectors in the Red

- Consumer Goods & Luxury: Weighed down by disappointing outlooks from heavyweights like Burberry.

- Aerospace & Defense: Seeing a "sell the news" reaction following CEO transition announcements at major players.

- Mining: Facing pressure as commodity prices fluctuate amid a stronger US Dollar.

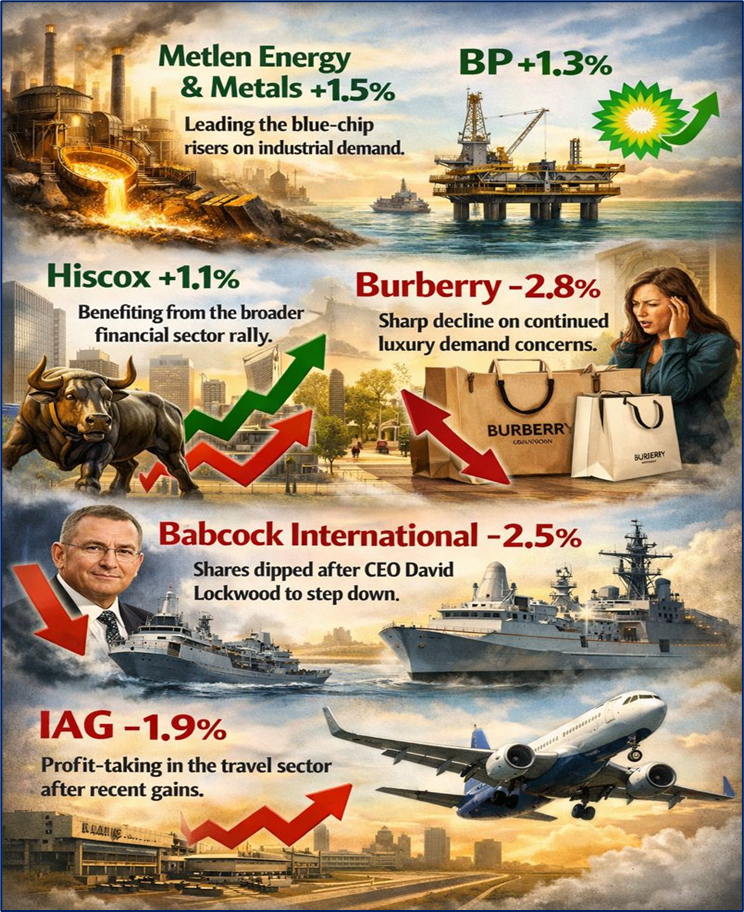

Top Stock Movers

Source: Kalkine Group

Technical Analysis Summary: The 10,100 Support Zone

Source: Trading View

From a technical perspective, today’s action confirms that the FTSE 100 is in a consolidation phase. The index is currently hugging its 20-day Moving Average, with immediate support found at the psychological 10,100 level.

The Relative Strength Index (RSI) is hovering near 64, suggesting the market is neither overbought nor oversold, leaving room for a move in either direction. However, the failure to hold the morning high of 10,184.14 suggests a lack of immediate "bullish conviction." If the index closes below 10,120, technical traders may eye the 10,050 mark as the next major floor.

The Bottom Line

The FTSE 100’s mild retreat today isn't a sign of a crashing market, but rather a healthy pause. The UK economy is showing surprising teeth—exemplified by the retail sales bounce—but the "Goldilocks" scenario of growth without inflation remains elusive. For retail investors, the focus remains on sector-specific stories rather than broad index movements. As the "data deluge" settles, the path to 10,200 remains open, provided the geopolitical landscape doesn't throw a fresh curveball.

Please wait processing your request...

Please wait processing your request...