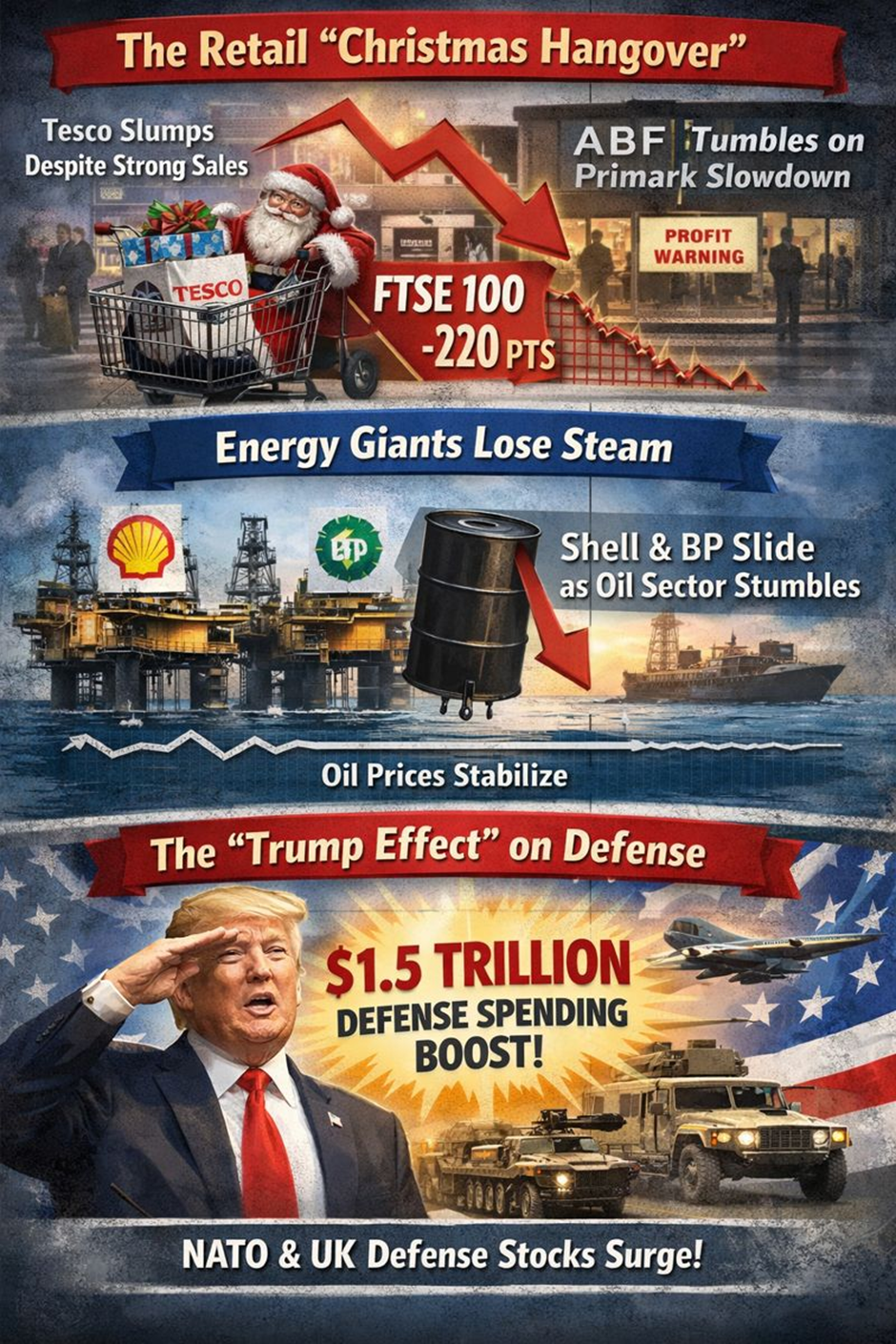

London’s blue-chip index retreated 0.22% on Thursday as a "perfect storm" of retail profit warnings and energy sector weakness neutralized a massive rally in defense stocks triggered by fresh spending vows from Washington.

Market Snapshot: The Numbers That Matter

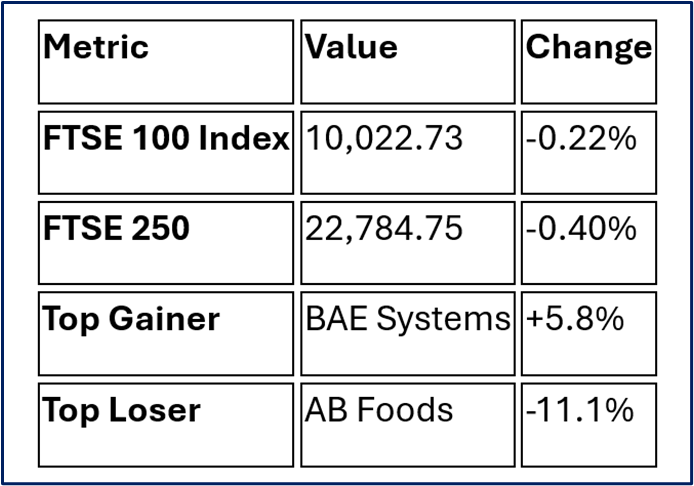

The FTSE 100 last traded at 10,022.73, shedding roughly 25 points. After recently breaching the historic 10,000 psychological barrier, the index found itself caught between two opposing forces: a surging defense sector fueled by geopolitical shifts and a retail sector reeling from a disappointing festive period.

Source: Market Data

The Drivers: Why the FTSE Faltered

The primary drag on the index came from the Retail and Energy sectors, which collectively overshadowed a rare "Goldilocks" moment for UK defense contractors.

1. The Retail "Christmas Hangover"

Investors were spooked by a series of trading updates that suggested the UK consumer is tightening their belt. Despite Tesco reporting strong Christmas sales, its shares fell as the market "sold the news," focusing instead on the cautious outlook for 2026. However, the real damage was done by Associated British Foods (ABF), which saw its worst day in years after warning of a slowdown at Primark.

2. Energy Giants Lose Steam

Heavyweights Shell and BP acted as a persistent anchor on the index. Shell’s shares dropped nearly 2.6% following a production update that flagged potential losses in its chemicals division and a tightening of its LNG output range. With oil prices stabilizing but showing no signs of a breakout, the energy sector's massive weighting in the FTSE 100 made it impossible for the index to stay green.

3. The "Trump Effect" on Defense

The silver lining was provided by President Donald Trump, who announced plans to hike the US defense budget to $1.5 trillion. This sent shockwaves through London-listed defense firms, which are seen as primary beneficiaries of increased NATO and US military spending.

Source: Kalkine Group

Sector Analysis: Winners & Losers

The Gainers: Defense & Mining

- Aerospace & Defense (+4.5%): The clear winner. BAE Systems and Rolls-Royce reached fresh highs as investors rotated into "security" assets.

- Mining: Despite a slight dip in midday trading, certain miners held onto gains as global supply concerns persisted, though the sector was volatile due to cooling demand from China.

The Losers: Retail & Utilities

- Retail (-6.2%): The worst-performing sector. High-street names were hammered by the Primark profit warning.

- Energy (-2.1%): Dragged down by Shell's operational update and a bearish outlook for global oil surpluses in early 2026.

Individual Stock Performance

Top 5 Gainers

- BAE Systems (+5.8%): Riding the wave of the proposed $1.5tn US defense budget.

- Coca-Cola HBC (+4.2%): Defensive beverage stocks saw a flight to safety.

- Endeavour Mining (+3.4%): Benefited from a slight uptick in gold's mid-day appeal.

- Marks & Spencer (+2.6%): A rare retail outlier, continuing its post-Christmas momentum.

- Babcock International (+2.1%): Gained on the back of the broader defense sector rally.

Top 5 Losers

- AB Foods (-12.9%): Primark owner crashed on weak festive sales and US food demand.

- Greggs (-7.7%): Warned of flat profits for the upcoming year.

- Tesco (-6.1%): Profit-taking followed "top of the range" earnings guidance.

- Mondi (-3.5%): Packaging giant hit by concerns over slowing industrial demand.

- Shell (-2.6%): Dragged by chemical division losses and production downgrades.

Analyst Corner: Upgrades & Downgrades

The brokerage community has been busy recalibrating for a "higher-for-longer" geopolitical risk environment.

- Rentokil Initial: Upgraded to Overweight by Morgan Stanley, citing attractive valuations after recent sell-offs.

- JD Sports: Downgraded by Bank of America; analysts expressed concern over a "material stepdown" in sportswear growth for 2026.

- Diageo: Upgraded to Outperform by RBC Capital Markets, with a price target of 2,000p, as cash flow remains resilient.

- Ocado: Placed on "Positive Catalyst Watch" by JPMorgan.

Technical Analysis Summary: The 10,000 "Line in the Sand"

Technically, the FTSE 100 is at a crossroads. After hitting record highs earlier in the week, the index is showing signs of being overbought on the RSI (Relative Strength Index).

- Support Levels: Immediate support is seen at 9,973, with a more significant "floor" at 9,880.

- Resistance Levels: The bulls need to reclaim and hold 10,050 to open the door for a run toward 10,150.

- Outlook: While the medium-term trend remains bullish (as long as it stays above the November low of 9,423), a short-term consolidation or "cooling off" period is expected as the market digests recent gains.

Investor Tip: Watch the GBP/USD pair. Sterling is trading near a 3-month high ($1.344); any further strength in the Pound could continue to pressure the FTSE's multinational earners by devaluing their overseas profits.

Source: Trading View

Please wait processing your request...

Please wait processing your request...