On January 15, 2026, the FTSE 250 Index is outperforming its blue-chip peers, surging 1.21% to trade near the 23,234 mark. This mid-cap rally is fueled by a "Goldilocks" combination of stronger-than-expected UK GDP data and a significant resurgence in the financial services sector.

1. Key Drivers & Market Sentiment

- GDP "Beat": The primary catalyst was the ONS report showing UK GDP grew 0.3% in November, tripling the consensus forecast of 0.1%. This suggests the UK economy is more resilient to high interest rates than previously feared.

- Services Rebound: A 0.3% rise in services and a 1.1% jump in production output provided the fundamental "engine" for mid-cap stocks, which are more sensitive to the domestic UK economy.

- M&A Heat: Mid-caps continue to be the target of "Smart Money" and private equity firms looking for value as the FTSE 100 sits at record highs above 10,000.

2. Sector Analysis: Gainers & Losers

Source: Kalkine Group

The Winners:

- Financial Services: Ashmore Group (+17%) skyrocketed after reporting massive net inflows and AUM growth to $52.5 billion, signaling a return of "Risk-On" sentiment in emerging markets.

- BioTech/Healthcare: Oxford Biomedica (+10%) and Oxford Nanopore saw heavy buying following positive sales guidance.

- Real Estate (REITs): Optimism over potential Bank of England rate cuts in mid-2026 lifted Safestore and Big Yellow Group.

The Losers:

- Recruitment: Hays PLC (-5%) tumbled after RBC Capital slashed its price target to 65p, citing a sluggish hiring environment in white-collar sectors.

- Housebuilders: Despite the GDP beat, Vistry Group faced volatility, dropping nearly 9% in early trade following lingering concerns over historical accounting adjustments, though it found support later in the day.

3. Analyst Upgrades, Downgrades & Bank Views

- Morgan Stanley: Issued a bullish note on European financials, specifically raising targets for retail-exposed banks as capital distribution plans for 2026-2027 look "highly attractive."

- Goldman Sachs: Flagged a "rotation to value" in the UK mid-cap space, highlighting that 63% of FTSE 350 recommendations are now "Buys" entering 2026.

- RBC Capital Markets: Downgraded Reckitt Benckiser to "Sector Perform" and cut Hays, signaling a selective approach to the UK market.

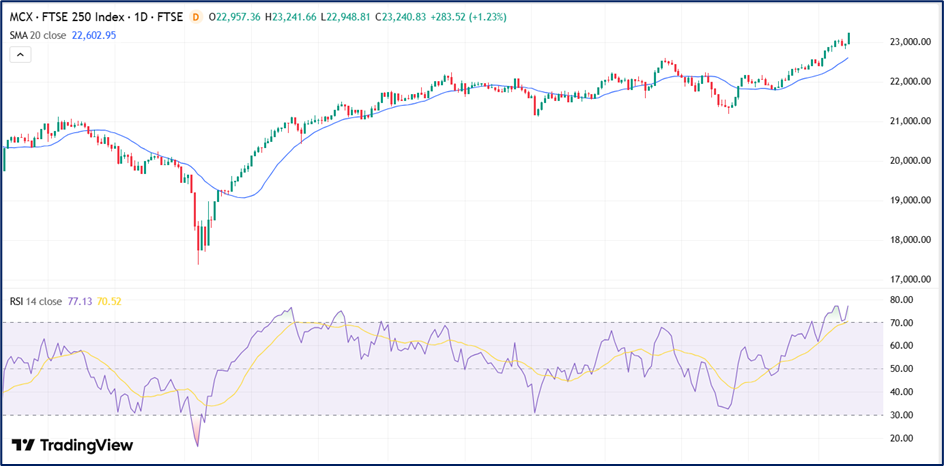

4. Technical Analysis Summary

Source: Trading View

The FTSE 250 is currently in a strong bullish breakout phase:

- Resistance: The index has cleared the psychological 23,000 barrier. The next major resistance sits at 23,450 (the 2024-2025 peak).

- Support: Immediate support is found at 22,800.

- RSI (Relative Strength Index): Currently at 77, suggesting there is still "room to run" before hitting extreme overbought territory.

- Moving Averages: The index is trading well above its 50-day and 200-day SMAs, confirming a medium-term uptrend.

The Retail Investor’s Take Forget the blue chips. While the FTSE 100 hovers at record highs, the real action is happening in the "Engine Room" of the UK economy. Today’s 1.21% jump in the FTSE 250 isn't just a fluke—it’s a fundamental repricing of British business.

With GDP data coming in three times higher than expected, the "Recession Fear" trade is officially dead. Hedge funds are ditching overvalued US tech and hunting for yield in London’s mid-market. Ashmore Group’s explosive 17% gain today is the "canary in the coal mine," signaling that the smart money is moving back into beaten-down asset managers and domestic winners.

Please wait processing your request...

Please wait processing your request...