While most traders were popping champagne, Litigation Capital Management (LSE: LIT) was popping off on the charts. On December 31, 2025, the AIM-listed alternative asset manager closed up roughly 9.5%, sparking intense retail interest. After a year defined by "unprecedented adversity" and a brutal 52-week slide, this year-end rally suggests the tide may finally be turning.

This deep dive breaks down the drivers behind the surge, the radical shift in their business model, and whether this is a "dead cat bounce" or a strategic rebirth.

The December 31 Surge: Key Drivers

Source: Kalkine Group

The 9.5% jump wasn't just random volatility; it was fueled by a convergence of late-quarter strategic moves:

- The "Covenant Lifeline": On December 30, 2024, LCM secured a crucial extension to its debt covenant waiver. For a company that saw its net debt balloon to A$40.1m earlier in the year, this breathing room from lenders was the "green flag" the market needed to stop the bleeding.

- Strategic Review Momentum: Management has been "constructively engaging" with third parties for a potential sale or merger. On the final day of the year, speculation reached a fever pitch that a transaction—representing a "viable alternative to the status quo"—might be imminent in early 2026.

- Short Covering & Year-End Rebalancing: After falling over 30% in December alone, LIT was heavily oversold. Institutional rebalancing and retail "bottom fishing" combined to drive a sharp upward correction on thin holiday volume.

Latest Business Model: From "Gambler" to "Manager"

LCM is aggressively shedding its old skin. Historically, the company acted like a principal investor, putting its own balance sheet at risk. The 2025 Pivot has shifted them toward an Asset Management Model:

- Third-Party Fund Management: Instead of using its own cash, LCM now manages massive pools of external capital (Fund I, II, and the newly launched Fund III).

- Performance Fee Engine: By shifting to a "Capital Light" model, LCM earns management fees and 20%+ performance "carries" on wins, without the catastrophic downside risk of losing its own principal.

- The "Run-Off" Option: As part of the ongoing strategic review, the board is considering a "run-off" model—essentially stopping new investments and returning all realized cash from the existing A$400m+ award pipeline to shareholders.

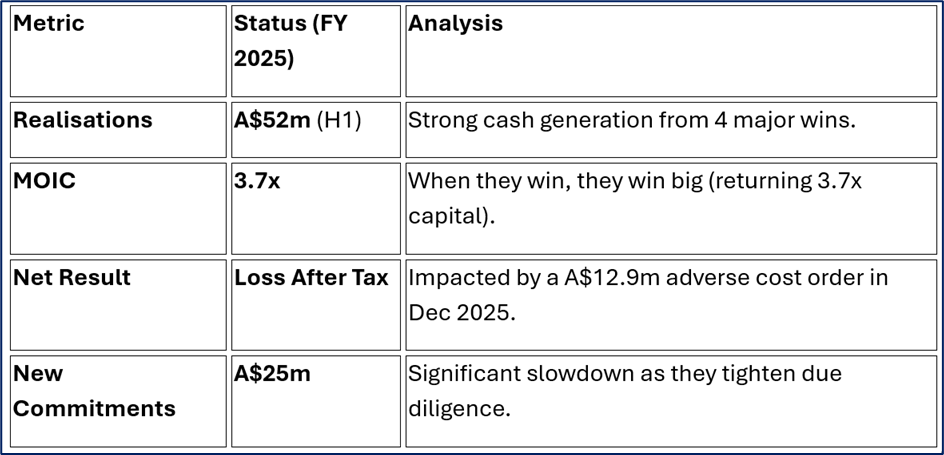

Financial & Operational Health Check

The numbers for 2025 have been a rollercoaster of "nuclear" wins and "painful" losses.

Source: Company Data

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Massive Award Pipeline: Over US$400m in potential awards currently in enforcement phases (e.g., Indiana Resources, Green-X Metals).

- Uncorrelated Returns: Litigation outcomes don't care about inflation or interest rates.

- High MOIC: A 13-year track record of 2.4x Multiple on Invested Capital (MOIC).

Weaknesses

- Binary Risk: A single "lost" class action (like the Queensland Electricity case) can wipe out millions in a single judgment.

- Liquidity Mismatch: Cases take 3–5 years to resolve, but debt interests are due monthly.

- Concentration: Too much capital tied up in "legacy" balance sheet positions.

Opportunities

- AI Integration: LCM is now using AI/ML to predict case outcomes and vet evidence, potentially lowering the "loss ratio."

- Secondary Markets: Selling "slices" of existing cases to other funds to de-risk and realize cash early.

- Consolidation: The strategic review could lead to a buyout by a larger private equity firm or a global competitor like Burford.

Threats

- Regulatory Crackdown: New US/UK rules requiring funders to disclose their "secret" agreements in court.

- Adverse Cost Orders: Courts forcing funders to pay the defendant's legal fees if the case is lost.

- "Nuclear Verdict" Fatigue: Judges increasingly pushing back against massive settlement demands.

Key Risks to Watch

Investors should not ignore the "Red Flags" that led to the 2025 price collapse. The company faces debt covenant pressure; if the strategic review fails to produce a buyer or a capital injection, the "run-off" model could become a forced liquidation. Additionally, litigation is unpredictable—even "slam dunk" cases can be lost on technicalities, as seen in the recent Quintis shareholder action.

Conclusion

The 9.5% rally on December 31, 2025, marks a "relief rally" for a stock that has been battered by bad news. With a new US$75m credit facility, a shift toward a fund-management model, and a massive pipeline of high-value international arbitrations, the intrinsic value of the portfolio may be significantly higher than the current market cap. However, until the Strategic Review concludes, LIT remains a high-stakes play on the "justice" system.

Please wait processing your request...

Please wait processing your request...