Galantas Gold Corporation (LSE: GAL) capped off 2025 with a striking 11.8% surge on December 31, leaving retail investors and gold bugs wondering if this is a "Santa Rally" or a fundamental shift.

While the broader gold market remained buoyant near $4,300/oz, Galantas carved its own path through a series of aggressive corporate manoeuvres and a massive strategic pivot.

Key Drivers: Why the 12% Spike?

Source: Kalkine Group

The year-end rally wasn't just momentum; it was the culmination of three major catalysts that hit the wires in late December 2025:

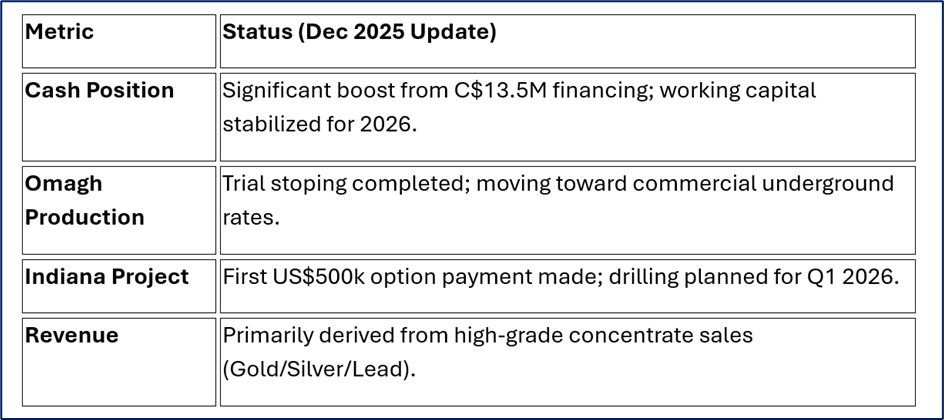

- The "Indiana" Breakthrough: Galantas successfully advanced the acquisition of RDL Mining Corp, granting them an option for the Indiana Gold-Copper Project in Chile. This transforms Galantas from a niche UK operator into a multi-jurisdictional player.

- Upsized Financing Success: On December 19, the company announced an upsized C$13.5 million financing deal. Closing these funds at the turn of the year provided the "dry powder" needed to execute their 2026 expansion.

- The "Ocean Partners" Synergy: The market responded favorably to the solidified Joint Venture with Ocean Partners UK, which de-risks the Omagh Project in Northern Ireland by providing technical and financial backing from a major global trader.

Latest Business Model: The 2026 "Hub-and-Spoke" Strategy

Galantas has evolved from a single-mine developer into a high-grade growth platform. Their latest model relies on three distinct pillars:

- Production Core (Omagh, Northern Ireland): Transitioning from open-pit to underground mining. The focus here is on high-grade "feed" processed via non-toxic froth flotation, keeping ESG scores high.

- The Chilean Growth Engine (Indiana Project): A high-grade gold-copper play in the Atacama region. The model here is "Early Cash Flow"—trucking ore to third-party mills while permitting their own 300 tpd (tonnes per day) plant.

- The Scottish Explorer (Gairloch): A long-term "VMS" (Volcanogenic Massive Sulphide) play in Scotland, serving as a secondary pipeline for resource growth.

Latest Updates: Financial & Operational (Q4 2025)

Source: Company Data

SWOT Analysis: A Reality Check

Source: Kalkine Group

Strengths

- Permitted Jurisdiction: Operating in stable, well-regulated regions (UK/Chile).

- High-Grade Assets: Omagh and Indiana both boast grades significantly higher than the industry average.

- Safe Processing: No cyanide or mercury used, making it a "green gold" favorite.

Weaknesses

- Capital Intensity: Underground mining requires constant CAPEX.

- Going Concern Risks: Like many juniors, they remain dependent on equity markets to fund large-scale developments.

Opportunities

- Resource Expansion: Recent drilling suggests the Omagh veins extend much deeper than initially mapped.

- Gold Price Tailwind: With gold projected to hit $4,400 in 2026, margins could expand exponentially.

Threats

- Permitting Delays: Northern Ireland’s planning process is notoriously slow.

- Geopolitical Shifts: While Chile is mining-friendly, changes in royalty laws can impact NPV (Net Present Value).

Critical Risks to Monitor

- Dilution: The recent C$13.5M financing, while necessary, increases the share count, potentially capping per-share gains.

- Operational Execution: Scaling two underground mines simultaneously (Omagh and Indiana) is a massive technical challenge for a junior team.

- Volatility: With a low market cap, GAL remains subject to "swing" volatility; a 12% gain can quickly be met by a 10% correction on low volume.

Conclusion

Galantas Gold is no longer just a "Northern Ireland story." By ending 2025 with a funded treasury and a foothold in Chile, the company has successfully repositioned itself as a diversified junior producer. The 12% jump reflects a market finally pricing in the "RDL acquisition" and the removal of near-term funding uncertainty.

Please wait processing your request...

Please wait processing your request...