Genedrive PLC (LSE: GDR) closed out 2025 with a festive flourish, seeing its share price climb approximately 9.3% on December 31, 2025. For a company that spent much of the year navigating turbulent financing waters, this year-end rally caught the attention of retail investors and biotech analysts alike.

Below is a deep dive into the drivers, the business model pivot, and the operational updates fueling this momentum as we head into 2026.

Key Reasons for the Dec 31st Surge

Source: Kalkine Group

The New Year's Eve spike was not a random fluctuation; it was the culmination of three specific tailwinds:

- AGM Optimism: The company held its Annual General Meeting (AGM) at 10:00 AM on December 31. Early sentiment from the meeting suggested shareholder alignment on the "Next Chapter" strategy, particularly following the earlier rejection of a highly dilutive equity raise in October.

- The "Nugent" Safety Net: Investor confidence has been buoyed by the finalized £1 million loan facility from major shareholder David Nugent. This provided the "bridge" financing needed to survive into early 2026 without immediate, aggressive dilution.

- NHS Momentum: Late December news regarding the Scotland NHS “test of change” pilot programme and the publication of the NHS Implementation Guide for CYP2C19 testing signaled that Genedrive is moving from "pilot" phase to "standard of care" in the UK.

Latest Business Model: From R&D to Commercial Scale

Genedrive has officially transitioned from a research-heavy biotech firm to a commercial-stage pharmacogenetics leader. Its business model now focuses on three pillars:

- The Razor/Razorblade Strategy: Selling the Genedrive® System (the hardware) at a competitive entry point, while generating high-margin recurring revenue through single-use, ambient-temperature stable test cartridges.

- Direct NHS Integration: Rather than just selling to private labs, Genedrive is embedding its tests directly into emergency care pathways (e.g., ambulances and neonatal wards) where speed is the primary value proposition.

- International Distribution: Using MoUs and partnerships in regions like Saudi Arabia and the European Union (following CE-IVDR certification) to scale without the overhead of a global direct sales force.

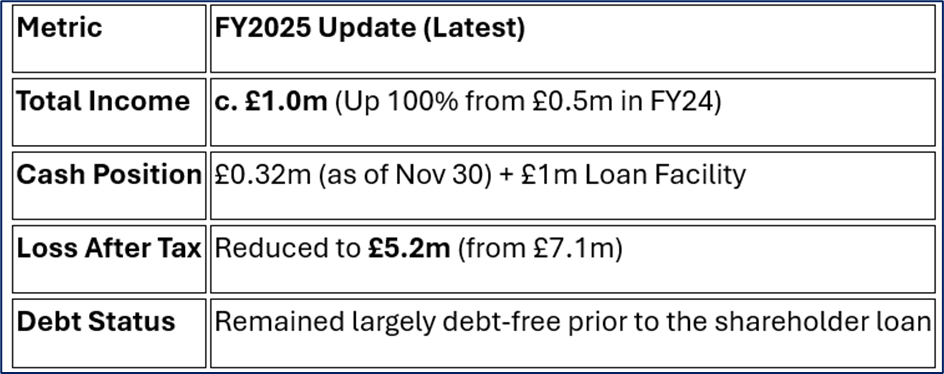

2025 Financial & Operational Highlights

Source: Company Data

Operational Wins:

- CYP2C19 ID Kit: Now featured in official NHS implementation guides for stroke patients.

- MT-RNR1 ID Kit: The "world’s first" bedside test to prevent antibiotic-induced hearing loss is now seeing national rollout in Scotland.

- Manufacturing: Successfully onshored and internalised assay manufacturing in Manchester to dual-source supply and protect margins.

SWOT Analysis (Strategic Outlook 2026)

Source: Kalkine Group

Strengths

- First-Mover Advantage: World’s first point-of-care test for neonatal hearing loss (MT-RNR1).

- Speed: Results in 26–70 minutes, whereas lab-based tests take days.

- Regulatory Status: CE-IVDR certified and FDA Breakthrough Device designation.

Weaknesses

- Cash Burn: Average monthly burn of £0.35m vs. low cash reserves.

- Historical Dilution: Frequent equity raises have historically pressured the share price.

- Revenue Scale: While doubling, £1m in annual income is still small relative to operating costs.

Opportunities

- US Market Entry: FDA 510(k) submission for CYP2C19 is anticipated in early 2026.

- "Innovator Passport": New UK healthcare reforms could allow faster adoption across all NHS trusts.

- M&A Target: As a leader in a niche but vital tech space, GDR is a potential acquisition target for larger diagnostic giants.

Threats

- Financing Risk: If the £1m loan isn't enough to reach profitability, further dilutive funding may be required.

- Regulatory Delays: Any pushback from the FDA regarding the US rollout would be a significant blow.

- Competition: Larger players could eventually develop similar "near-patient" PCR technologies.

Key Risks to Watch

- The "Runway" Issue: As of December 2025, the company is still in a race against time to turn its growing "clinical interest" into "cash flow."

- High Volatility: With a market cap hovering around £10m–£12m, small buy orders can cause massive percentage swings, making it a high-risk play for retail investors.

Conclusion

The 9.3% gain on December 31, 2025, reflects a market that is starting to price in the "derisking" of Genedrive’s immediate survival. With the £1m loan secured and NHS implementation guides now active, the story for 2026 is no longer "Will they survive?" but "How fast can they scale?"

The upcoming FDA submission in early 2026 and the Half-Year Earnings Release in March 2026 will be the next major catalysts for the stock.

Please wait processing your request...

Please wait processing your request...